Russia's Iran War Windfall in Perspective

As long as financial sanctions and export controls remain in place, the aggressor's gains from higher oil and gas prices will be limited.

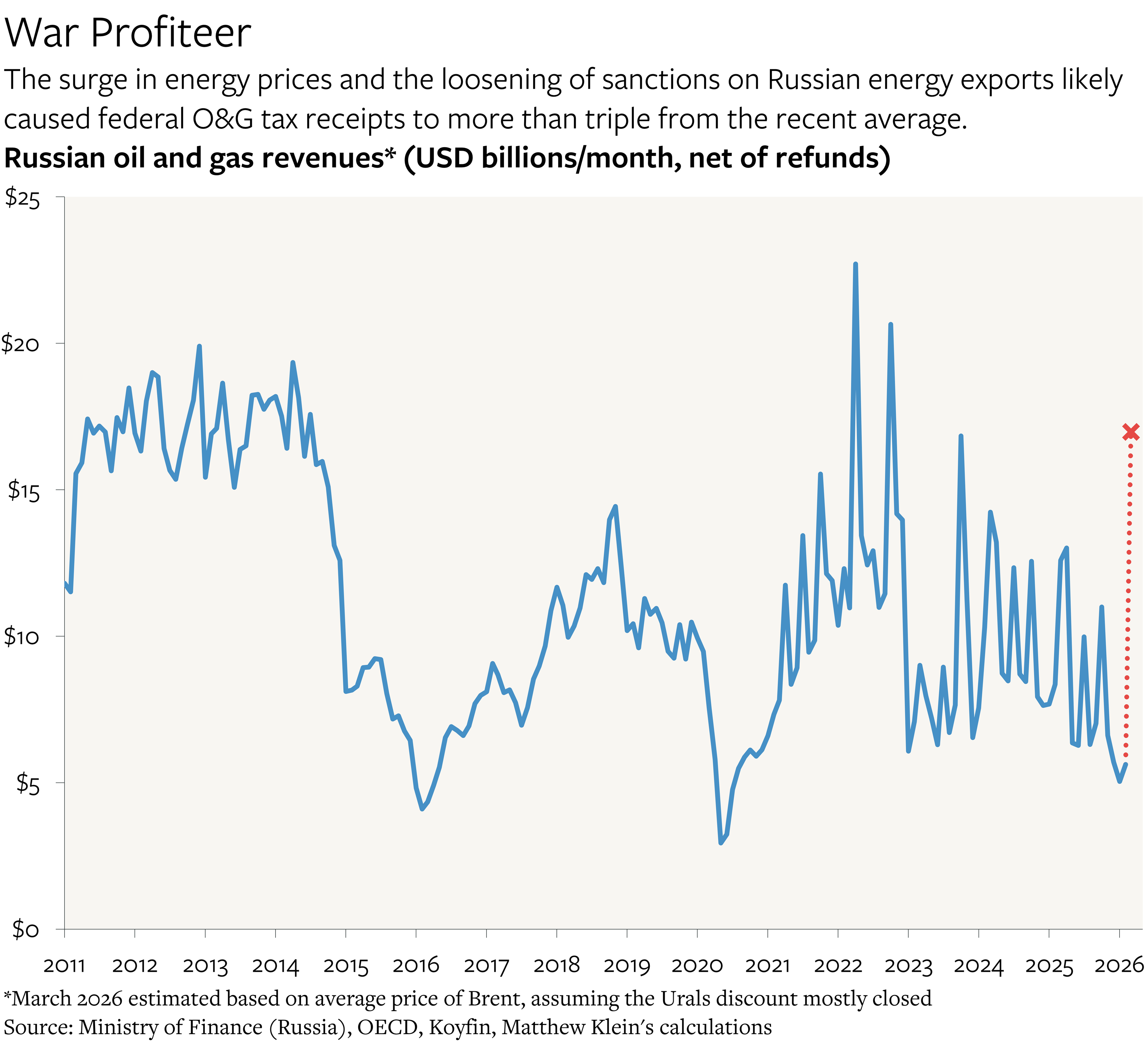

At current prices, the Russian government’s energy-related tax revenues are probably running about 3x the monthly average from December 2025-February 2026. If those prices hold for the rest of the year, total oil and gas tax receipts would be worth about $180 billion in 2026, up from $101 billion in 2025.

If Russian export prices rise further from here—which seems likely given the world’s growing desperation for oil, gas, and refined products that are not affected by the Iranian government’s growing realization that it controls all traffic through the Strait of Hormuz—then the Russian government could find itself with a windfall worth hundreds of billions of dollars. (Unless of course its own export volumes are constrained by Ukrainian attacks.) Russia is also poised to benefit from its position as a major exporter of fertilizers now that Middle Eastern exports are no longer available.

The bad news is that consumers of essential commodities are being forced to make do with less, with the constrained supply rationed according to the willingness (or the ability) to pay increasingly high prices. As is always the case, the global poor will be hit hardest.

The good news is that, as long as the allies hold the line on non-energy sanctions and export controls, the disruption in Hormuz will do little to improve Russia’s position in its war of aggression against Ukraine. For better or worse, Russian energy exports have never been that important to the war effort. Russian officials have been steadily reducing the importance of oil and gas taxes in financing day-to-day spending ever since the 2014 price crash, and their current plan is to assume that energy prices will not only revert to pre-Iran levels, but fall further. The windfall, such as it is, should allow the Russians to rebuild their National Wealth Fund (NWF), which has been partially drained in recent years, but it will not alter the Russian economy’s material constraints, particularly the ongoing shortages of men and manufactured goods.

Russia Is Not a “Gas Station Masquerading as a Country”

Looking at how the Russian economy and financial system responded to large changes in energy prices in the recent past is helpful for thinking through the current situation. The reaction to the 2014-2016 energy price crash has meaningfully changed the Russian government’s sensitivity to oil prices.