The Fed Tries to Thread the Stagflation Needle

By doing exactly what they were planning to do before, at least for now.

The new Administration is in the process of implementing significant policy changes in four distinct areas: trade, immigration, fiscal policy, and regulation. It is the net effect of these policy changes that will matter for the economy and for the path of monetary policy. While there have been recent developments in some of these areas, especially trade policy, uncertainty around the changes and their effects on the economic outlook is high.

—Jerome Powell, March 19 2025 press conference

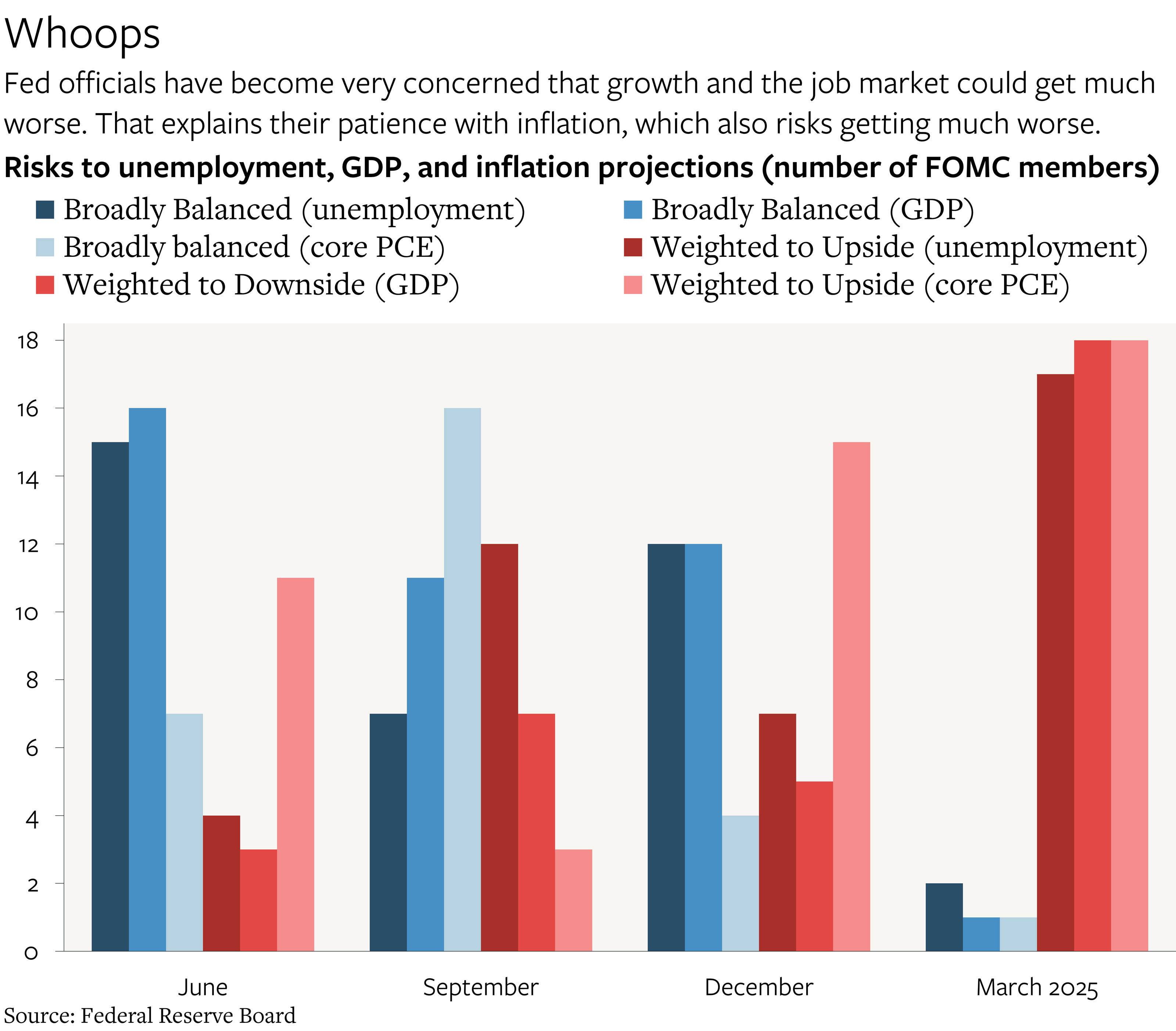

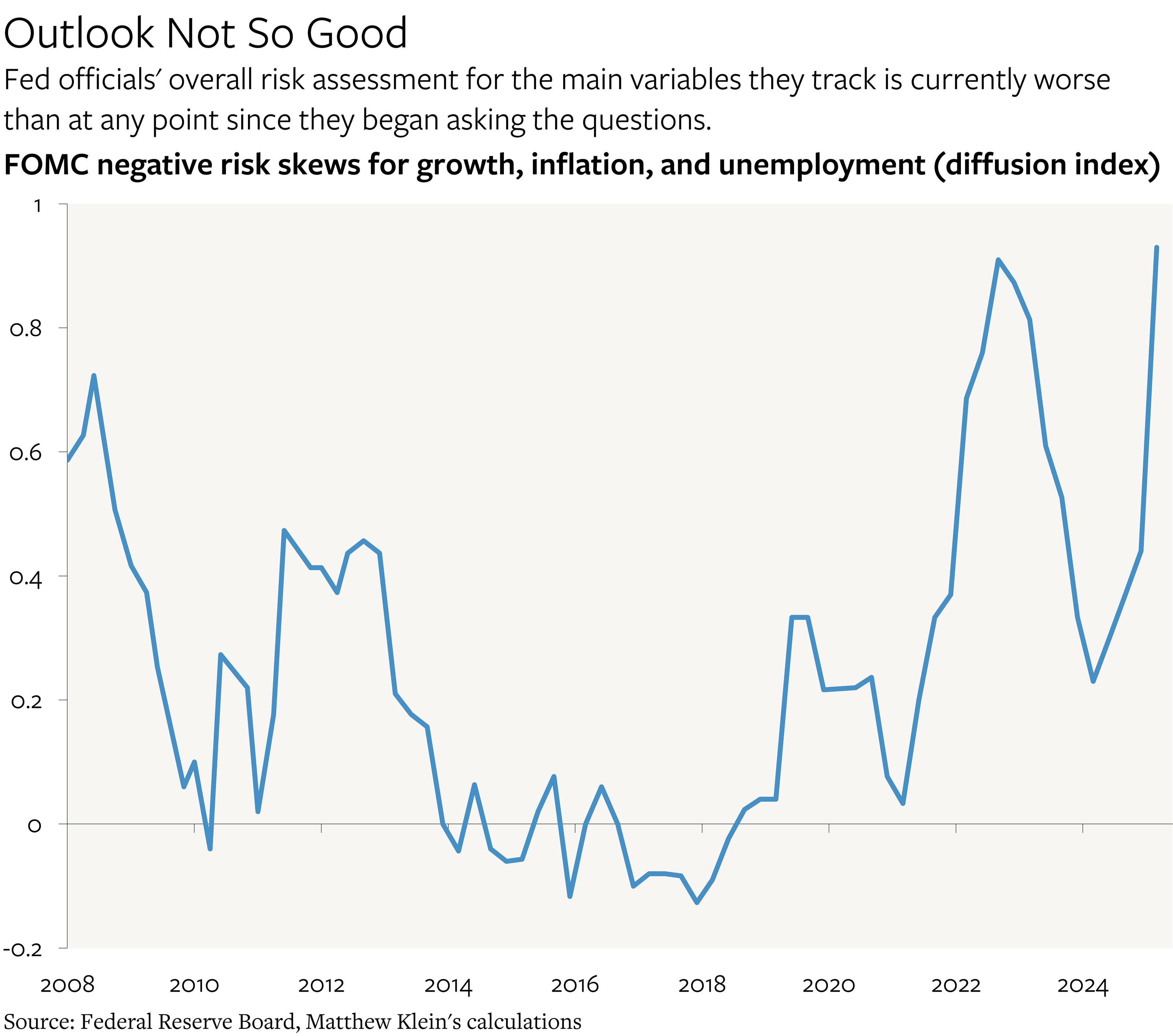

Federal Reserve officials always have a hard job, but the new administration has made it far more challenging. According to officials’ latest Summary of Economic Projections (SEP), forecast uncertainty has spiked for growth, for inflation, and for joblessness. Moreover, this uncertainty has an unpleasant skew, reflecting worse balance of risks for all three variables.

In fact, the average balance of risks across the three variables has never been judged to be worse than it is now. (Or at least not since Fed officials were asked about these issues every quarter starting at the end of 2007.) Moreover, this spike in fear is not attributable to any external shock, such as a global pandemic or Russia’s attack on Ukraine, or even a nonviolent surprise such as the global financial crisis. Instead, it is entirely attributable to policy choices from the new administration.

There are obvious reasons to worry about inflation stemming from higher input costs and hoarding, and there are also good reasons to worry about the growth and employment outlook as consumers and businesses retrench in the face of extreme policy arbitrariness. As Powell said, the question for the Fed is how to weight these risks.

So far, monetary officials seem to have concluded that the net impact on the variable they care most about—unemployment—is zero. That is why, despite everything else, the median official’s projected path of short-term interest rates “under appropriate monetary policy” has not changed since the last set of projections were published in December. The question is whether this balance will hold, and if not, which way officials will break.