Less Tax Evasion, a Profit Boom, and a Persistent Interest Puzzle: Highlights of the 2023 Comprehensive NIPA Revisions (Part 1)

The quinquennial update of the U.S. National Income and Product Accounts has lots of new information. But many questions about the state of the economy remain.

In the U.S. national accounts, economic activity is represented by two separate, yet equally important aggregates: the expenditure-based estimate (GDP), which is the sum of personal consumption, business investment, the trade balance, and government spending; and the income-based estimate (GDI), which is the sum of wages and benefits, interest, profits, rents, and taxes.

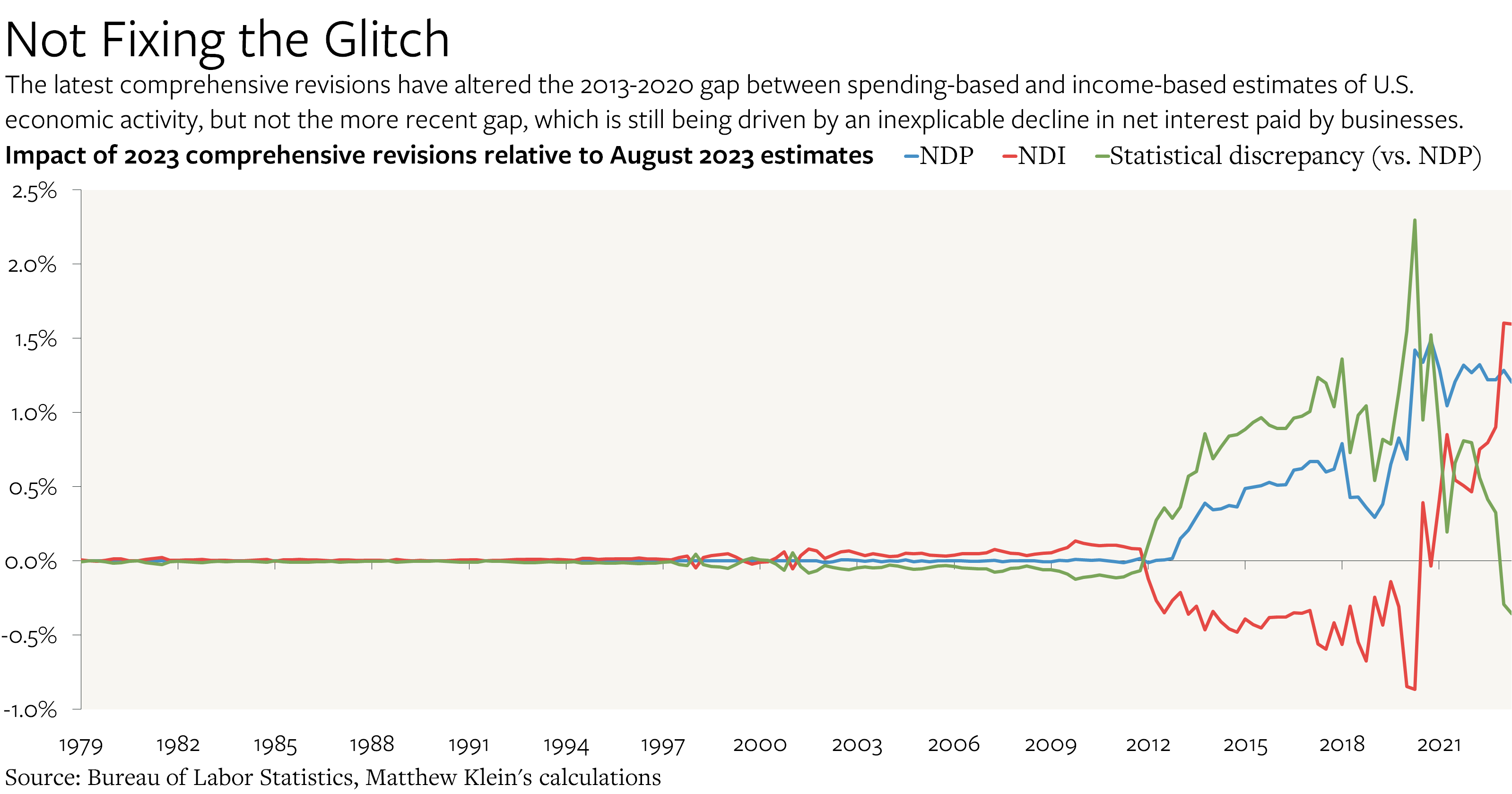

While the two aggregates should be the same, there is often a “statistical discrepancy” between them. Changes in this gap can sometimes lead to contradictory answers to seemingly simple questions such as “is the economy shrinking or growing?”

Since 2021, there have been large swings in the discrepancy between GDP and GDI. At one point, it seemed as if GDP was radically understating the strength of business investment. (It turned out that GDI was overstating workers’ wages and grossly underestimating dividend payouts.) More recently, GDI has been falling sharply vs. GDP mostly because American businesses’ net interest payments have allegedly dropped by 31% since the most recent peak in 2022Q2. Real domestic income excluding interest payments is more or less in line with real domestic production (net of depreciation).

Every five years, the Bureau of Economic Analysis (BEA) publishes comprehensive revisions informed by the highest-quality—and lowest-frequency—sources, such as the Economic Census, the IRS’s Statistics of Income, and the Annual Survey of Manufactures. One consequence is that both measures of economic output were revised up nearly 2% as of 2023Q2. But the gap between the income-based and expenditure-based estimates remains large, even if the 2013-2020 discrepancy now looks somewhat smaller.

What follows is a breakdown of what happened with both the income-based and expenditure-based estimates. The detailed monthly data on personal income, spending, saving, and prices will be the subject of a subsequent note.

The main highlights:

The BEA’s new approach to the treatment of “regulated investment companies” shifted the composition of national income. Financial corporations are now recorded as having paid much less interest, while financial and nonfinancial corporations are both earning higher profits. Those effects mostly canceled each other out until 2020.

Corporate profits have grown much more than previously thought during the pandemic, with corresponding effects on estimates of corporate tax receipts and dividend payments.

New estimates of tax evasion for the years 2014-2016, which is the latest available period, depressed historical estimates of small business and partnership income in the years before the pandemic.

Estimates of spending on imputed rent “paid” by owner-occupiers have been revised up (along with personal rental “income”) even as estimates of spending on actual rent by tenants was revised down.

There is an unusual disconnect between revisions to personal income tax receipts, social insurance tax receipts, and wage income.

Investment spending has been revised up across many categories, most notably nonresidential structures and multifamily housing. But an apparent investment boomlet in one particular category that I had previously been excited about was revised away.

And finally, the bizarre plunge in net interest payments by businesses refuses to go away.