Markets Are Still Sanguine About the Oil Outlook

Prior oil shocks in 1973 and 1979 involved far larger price increases than what we have seen so far. Yet this shock involves a hit to volumes that is unprecedented outside of the pandemic.

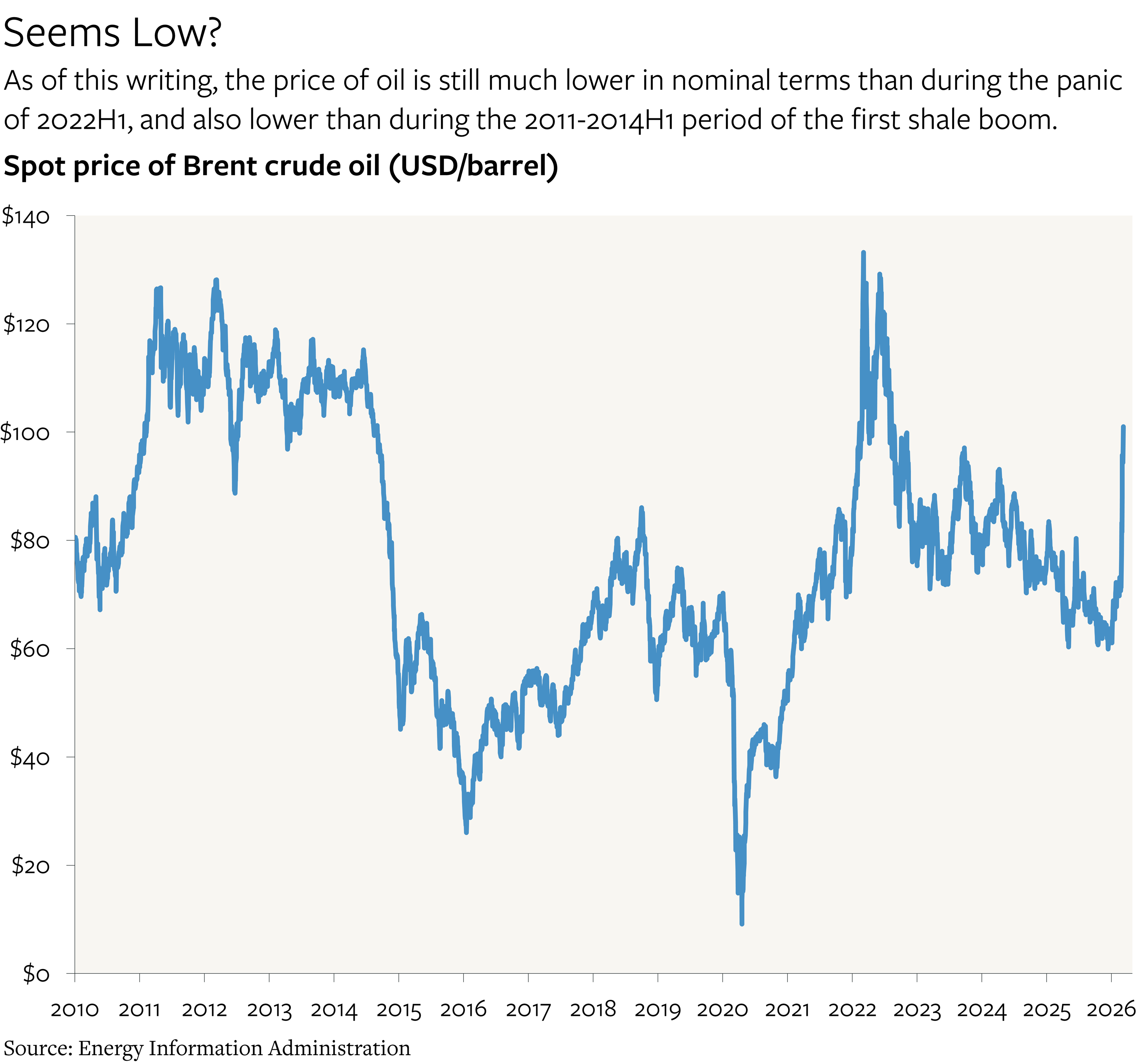

The striking thing about oil prices, given what is going on in the world, is how low they are.

Crude oil exported from Iran, Iraq, Kuwait, Saudi Arabia, Qatar, and the United Arab Emirates (UAE) was equivalent to about 20% of global supply before the recent war with Iran, or more than 40% of all crude oil exports. Much of this supply is now unavailable,1 with traffic through the Strait of Hormuz still stuck around zero as ships avoid Iranian drones, missiles, and mines.

Yet as of this writing, front-month Brent crude futures are trading at just $103/barrel. That is still lower, in nominal terms, than in the first few months of Russia’s 2022 invasion of Ukraine ($110-$130). It is also lower than the stable average of about $110 that persisted from early-2011 through mid-2014.

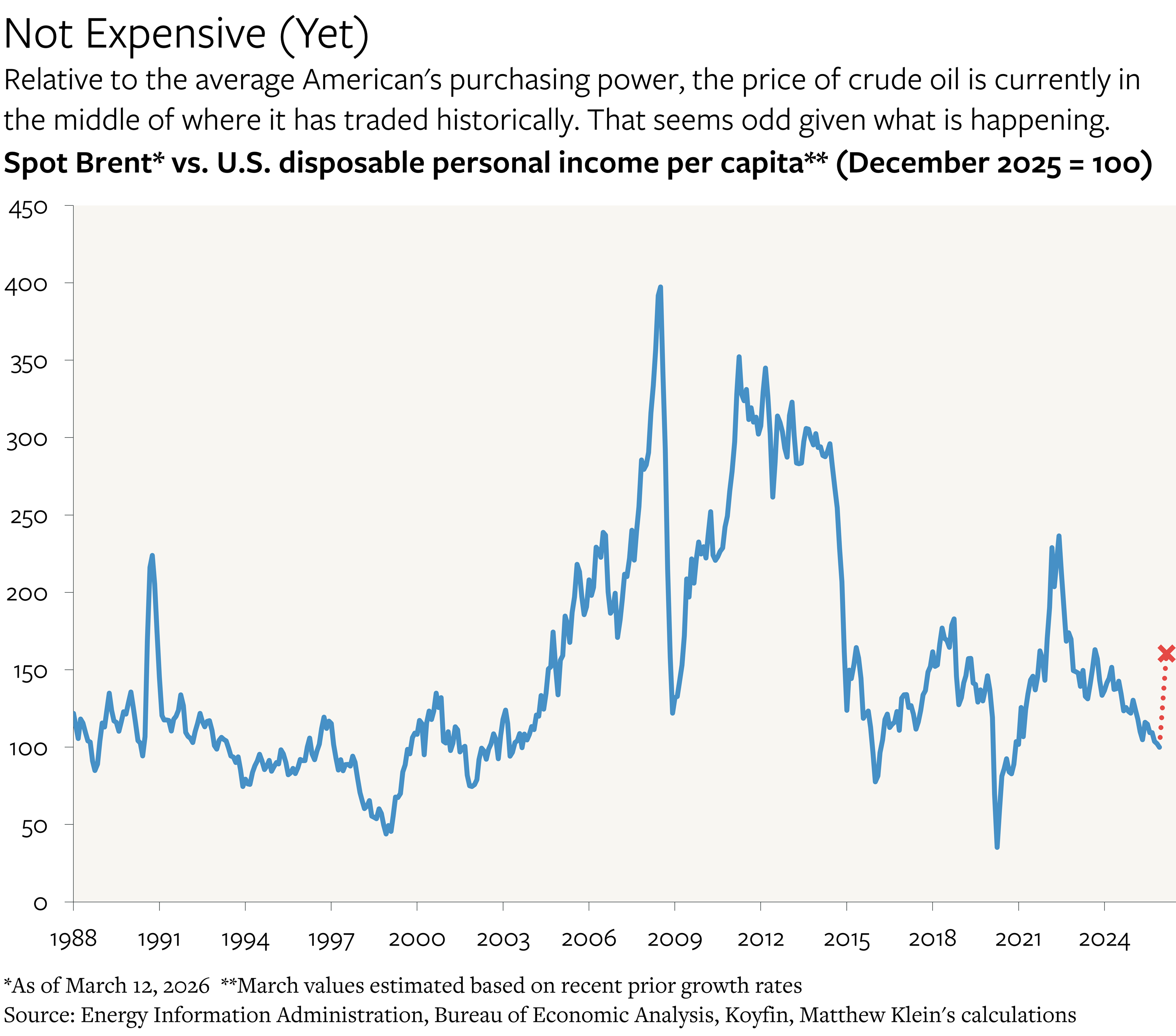

Even more striking is how low the current price looks when adjusted for inflation and productivity growth. Dividing the monthly spot price of Brent crude oil by nominal U.S. disposable income per capita2 shows that today’s “real” price is right in line with the average since January 1988—and far below any previous period when the price of oil was considered too high.

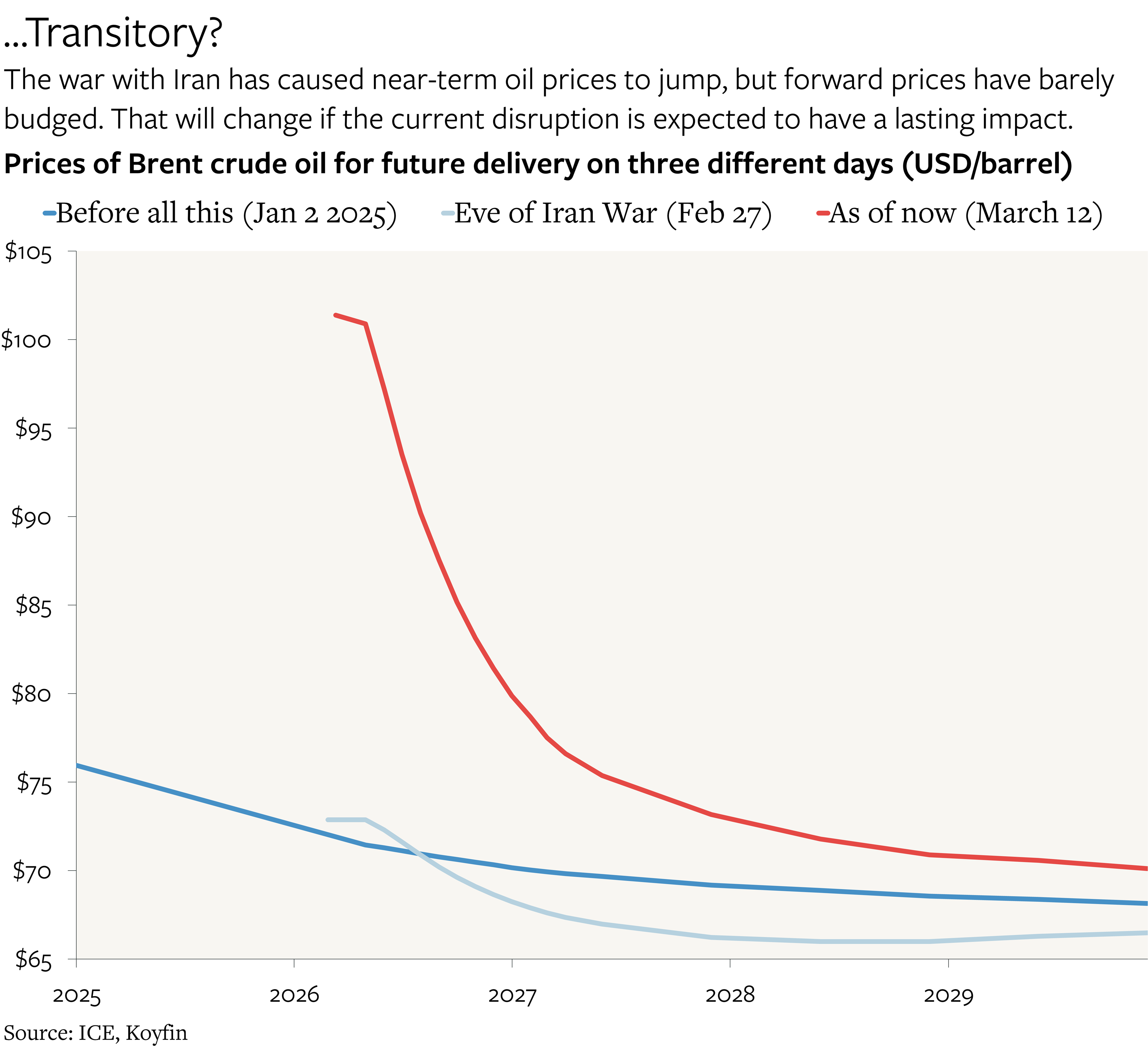

Moreover, anyone willing to wait for physical delivery can lock in prices substantially lower than the current spot price. Equivalently, anyone who has physical crude oil available to distribute today can get paid a massive premium to clear out their storage space in exchange for the promise to refill later.

The August 2026 Brent futures contract was just under $90/barrel on the evening of March 12, the January 2027 contract was trading at just under $80/barrel, and the December 2027 contract was just $73/barrel. Those willing to wait until December 2028 could secure oil for the price of just $70/barrel. All of those futures contracts were barely higher than the $66/barrel price that prevailed across the curve on February 27 (the eve of the war with Iran). In fact, the prices of Brent contracts for March 2027 onwards were barely higher than where they were in the beginning of 2025.

The implication is that the current price spike is attributable to temporary disruptions that will soon fade, rather than permanent reductions in the world’s oil supply.

But even if a quick return to normalcy were the single likeliest outcome, which is far from obvious—I will defer to the military experts and oil gurus—there are many other possibilities, all of which would be worse for oil consumers. We simply do not know what is needed to restore pre-war shipping volumes through the Strait of Hormuz at pre-war insurance rates. As Defense Secretary Pete Hegseth unhelpfully explained, “The only thing prohibiting transit in the straits right now is Iran shooting at shipping. It is open for transit should Iran not do that.”

Given this uncertainty, comparing the current crisis with previous notable oil disruptions, both in terms of price and volume impact, is helpful for getting some perspective. There are three big takeaways:

The current threat to supply is unprecedented

Prior changes in prices required to reduce demand and/or increase supply were far larger than what we have seen so far, and the adjustment periods also took longer, even though the changes in volumes were also far smaller than what is currently happening

The U.S. is still extremely sensitive to disruptions of crude oil imports despite being a net exporter of petroleum+products, at least when it comes to inflation

1973, 1979, and the 2000s

Over the past century there were three distinct episodes when oil prices more than doubled from “normal” levels and then stayed high.