If You Thought the Inflation Outlook Was Bad Before...

Quantifying its size is impossible given how little we know about when and how this will end, but the direction of the impact is obvious. The big question is whether long-term beliefs will shift.

I have no insights into how the war with Iran will unfold—in common with the people in charge, apparently—nor am I an expert in commodity markets. But it does not take much expertise to see that any sustained reduction in exports from the Gulf will be painful.

According to the latest Statistical Review of World Energy, about 20% of all liquefied natural gas (LNG) exports in 2024 came from Qatar, mostly going to East Asia. About a third of all crude oil exported in 2024 came from Iraq, Kuwait, Saudi Arabia,1 and the United Arab Emirates (UAE). Similarly, about 18% of global exports of refined petroleum products also came from those four countries.

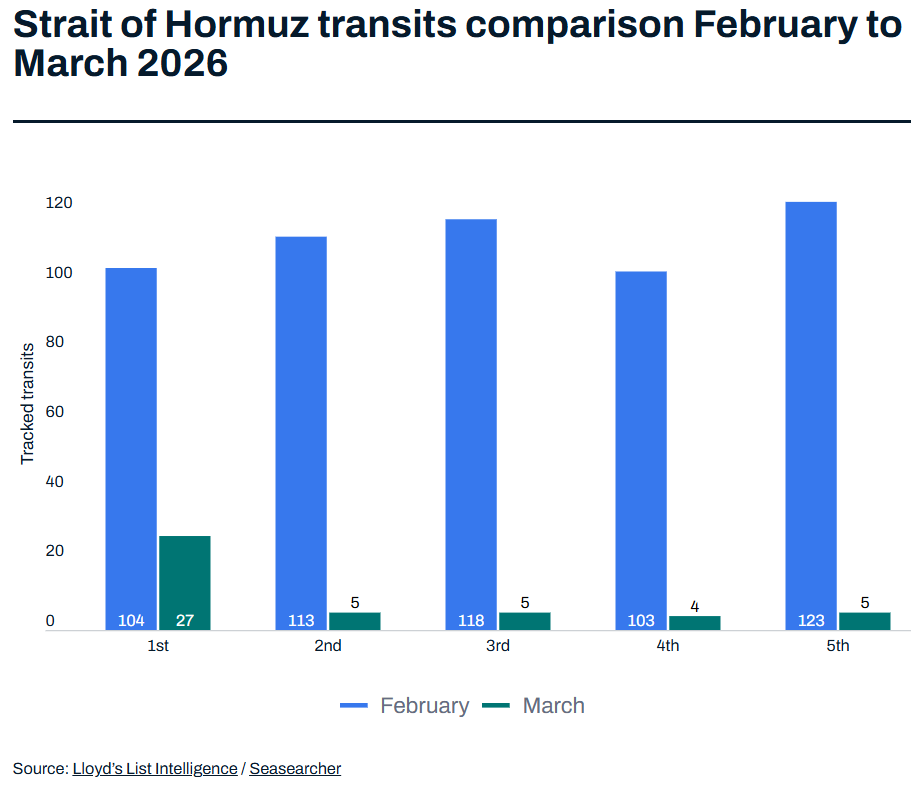

As of this writing, those exports have more or less stopped. From Lloyd’s List:

Without the ability to export, storage facilities for crude are filling rapidly, and some producers have already responded by slashing output. The problem is not just that the Strait of Hormuz is unsafe for tanker traffic, but that much of the infrastructure for extracting, storing, refining, and exporting fossil fuels from the Gulf is currently under attack from Iranian drones and missiles. The longer the fighting lasts, the harder it will be to restore production and exports to pre-war levels.

So far, spot crude oil prices are up about 50% since the start of the year, and up around 25% as of this writing since the start of the conflict. That relative calm may reflect ample inventories in the major consuming societies plus, possibly, a temporary reduction of Chinese stockpiling. (Or it might just be a mistake.) Gas and refined products are harder to store, however, which explains why international prices for LNG, jet fuel, and diesel have roughly doubled over the past week. (China discouraging exports of refined products has not helped, although the net effect depends on what they are doing with their reserves of crude oil.)

The supply crunch is already flowing through to the price of fertilizer, which is made from natural gas, which could in turn affect the northern hemisphere’s spring planting cycle and, eventually, food prices. The impact may not stop there. In addition to being used directly for heat and energy, crude oil and natural gas are both inputs for manufacturing chemicals and plastics, which in turn are used as inputs for everything from pharmaceuticals to semiconductors.

Stocks and bonds suggest that traders outside of the energy markets are relatively sanguine about all of this, at least so far. And they could well be right. Betting against human creativity and adaptability—which is, essentially, what any sustained long position in commodities represents—is usually a bad way to make money.

Still, we can be reasonably be confident that, in the short term at least, there will be a price to pay via some combination of worse real growth and faster inflation. The only argument is about the magnitude of the impact, not the direction.

That would make this the third negative supply shock to hit the global economy in the recent past, following the pandemic, which began almost exactly six years ago, and then Russia’s war of aggression on Ukraine, which started almost exactly four years ago. The loss of Russian commodity exports and the near-total closure of the Black Sea constituted a massive shock to the prices of everything from wheat to semiconductors, which hit particularly hard in the first half of 2022. (The Chinese goverment inadvertantly lessened the impact thanks to its extreme “Covid Zero” policy.) For Americans, the war with Iran is arguably the fifth supply shock over the past six years, if we include the policy uncertainty that has been unleashed since last January, particularly around tariffs, as well as the massive changes in net immigration flows.

At some point it becomes reasonable to ask whether these even count as “shocks” anymore, given their frequency. Individually, they are all more or less random unpleasant surprises. Collectively, however, they are responsible for repeated spikes in prices. The risk is that people people respond by changing what they think is “normal”. That is how inflation accelerates on a sustained basis. As Goldfinger put it, “Once is happenstance. Twice is coincidence. Three times is enemy action.”

Lael Brainard, who was an influential Federal Reserve official from 2014-2023, was explicit about the implications back in 2022:

A protracted series of supply shocks associated with an extended period of high inflation—as with the pandemic and the war—risks pushing the inflation expectations of households and businesses above levels consistent with the central bank’s long-run inflation objective. It is vital for monetary policy to keep inflation expectations anchored, because inflation expectations shape the behavior of households, businesses, and workers and enter directly into the inflation process. In the presence of a protracted series of supply shocks and high inflation, it is important for monetary policy to take a risk-management posture to avoid the risk of inflation expectations drifting above target.

Austan Goolsbee, the President of the Federal Reserve Bank of Chicago, told me something similar when I interviewed him in 2024:

The direct impact of higher oil prices, there’s nothing you can do about that. You’re going to get inflation from it. But you try to prevent wage-price spiraling, you try to prevent it from getting folded into expectations where you can’t get rid of it…One thing we learned was the supply chain is so many stages now that when chips were not there, then the computers that use those chips had their prices go up, and then when the computers’ price went up, then the autos that use those little computers, their price went up. Then the FedEx driver who’s using the car—it had a “if you give a mouse a cookie” element to it. We should think about that when we’re thinking about monetary policy reaction to supply shocks.

The problem for policymakers in the U.S. is that inflation had been persistently faster than their alleged 2% yearly goal before 2025, with no sign of improvement over the past 12 months. If anything, the situation was only getting worse before the Iran war.

The rest of this note has two parts. First, some additional perspective on the disruption to gas and oil exports, in part informed by the recent experience with Russia’s war on Ukraine. Second, a detailed update on the latest U.S. numbers for inflation and the job market, which give us a sense of what the economy was looking like before the current conflict began.