The Atlanta Fed's Nowcast Is Broken (For Now)

Imports of gold bars turn out to be surprisingly important. Plus: some thoughts on the February jobs numbers.

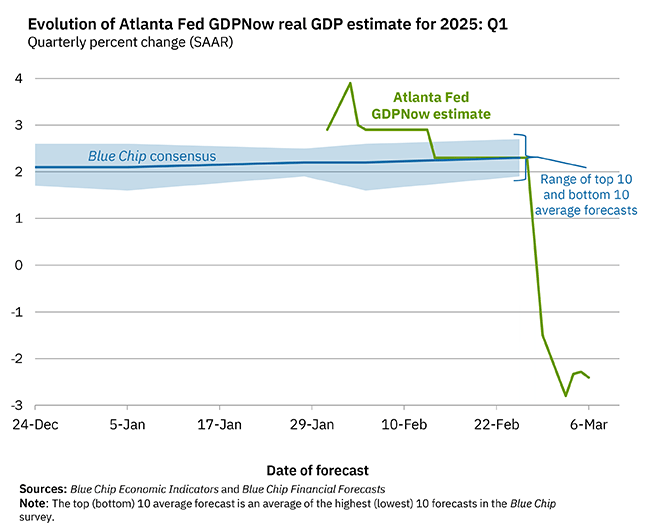

The Federal Reserve Bank of Atlanta provides many valuable services to the public, one of which is its GDPNow estimate of current-quarter growth based on the latest available data. The current picture is dire:

Most of the bad news came on February 28, with the publication of the Census Bureau’s “Advanced Economic Indicators Report”. That showed that U.S. imports of goods surged by 12% on a seasonally-adjusted basis from December 2024 to January 2025 thanks to a 33% spike in imports of “industrial supplies”. (The early cut of the data does not provide more detail.) Exports of goods only rose by 2%, so the trade deficit was judged to have blown out by 26% in a single month.

The Atlanta Fed’s model responded by projecting that the growth in the trade deficit for January-March 2025 would subtract a staggering 3.7 percentage points (annualized) from the overall growth rate of real GDP in 2025Q1.1 The Atlanta Fed’s estimate of the impact did not change when the detailed trade data were published on March 6.

While a lot could happen between now and the end of March, I would be extremely surprised if the current GDPNow projection for 2025Q1 turns out to be accurate by the time the official growth numbers are published at the end of April.

Even if real output in January-March 2025 turns out to be substantially lower than in October-December 2024 on a seasonally-adjusted basis—which would be mathematically difficult absent a catastrophe hitting the U.S. within the next three weeks—it would more likely be because of weak consumer spending and business investment rather than what is currently implied by the Atlanta Fed’s model.

To understand why, it is important to dig into why exactly imports are counted against GDP, as well as the detailed trade data behind the recent import surge.

Trade Deficits and GDP Accounting

GDP stands for Gross Domestic Product, and each of those words is imporant for understanding how the aggregate number is put together. The goal is to track production of new goods and services within a given jurisdiction.2 One way to do this is to measure the value generated by each industry sector and add them all up to get GDP. While the Bureau of Economic Analysis (BEA) does calculate and publish these numbers, it does so with a lag. The short cut is the “expenditure approach”, which is based on the following identity:

Domestic Spending = Domestic Production - Exported Domestic Production + Imported Foreign Production

Or, more conventionally:

GDP = Consumption + Fixed investment + Changes in inventories + Exports - Imports

Spending is used as a proxy for what is actually produced, but that only works if exports are added in and imports are subtracted out to avoid double-counting. For the world as a whole, there is no difference between spending and production because all exports and imports add up to zero, but for individual places in particular points in time, this is not true.

GDPNow’s interpretation of the recent data is that domestic production is plunging as a wave of imports displaces American producers even as domestic demand decelerates. That is simply not happening. The Atlanta Fed model is being led astray by an error in its choice of data source.

All that Glitters…

In particular, much of the January 2025 pop in imports is attributable to goods that the BEA explicitly excludes from GDP. Remember that the point of GDP is to track production. Just as it is important to subtract imports to avoid double-counting, there is one category of imports that should not be counted: goods that are used as financial assets, which in practice means gold.

From chapter 8 of the handbook:

All domestic production of gold, regardless of its final use, is included in GDP. However, the NIPAs do not treat transactions in valuables, such as gold, as investments in fixed assets, and so investments in gold (other than gold held in industrial inventories) are not reflected in gross domestic purchases (PCE, gross private domestic investment, and government consumption expenditures and gross investment). For example, if households purchase gold as a form of investment, including that purchase in PCE would distort the analysis of consumption and saving…Only a small share of the international transactions in nonmonetary gold recorded in the ITAs is for business or industrial use; most transactions are for investment or other purposes. Consequently, the NIPA estimates for exports and imports of nonmonetary gold are not based on the ITA estimates.

This turns out to be very important.