The Fed is Misreading the Inflation Risks

Inflation was getting worse *before the war* across a broad range of categories. Yet Fed officials are still blaming "one-time things".

It is understandable why Federal Reserve officials decided not to let the war with Iran affect their monetary policy decision on Wednesday. The range of outcomes is so vast that it makes sense to wait until there are hard data on the responses of consumers and businesses.

What is not understandable is Fed officials’ faith that—leaving the war aside—inflation will return quickly to their 2% yearly goal as the economy accelerates and interest rates continue to fall.

This is a failure of analysis. According to Jerome Powell’s latest press conference, Fed officials believe that their policy has been “restrictive” (it has not), that inflation would already be at or close to 2% if not for tariffs (it would not), and that “the labor market is clearly not a source of inflationary pressures” (it is). The latest data, which run through February, make it clear that the inflation situation was continuing to get worse before the current conflict.

From that perspective, Fed officials should have been following the Reserve Bank of Australia, which has pivoted to raising rates, even without the war with Iran. Including a reasonable distribution of the possible consequences of the war into the calculations reinforces the case for rate increases.

Goods and Bads

Perhaps the most striking thing about Powell’s Wednesday press conference was the repeated—and wrong—insistence that excessive inflation was mostly about rising goods prices, which in turn were mostly about tariffs:

Inflation has eased significantly from its highs in mid-2022 but remains somewhat elevated relative to our 2 percent longer-run goal…These elevated readings largely reflect inflation in the goods sector, which has been boosted by the effects of tariffs.

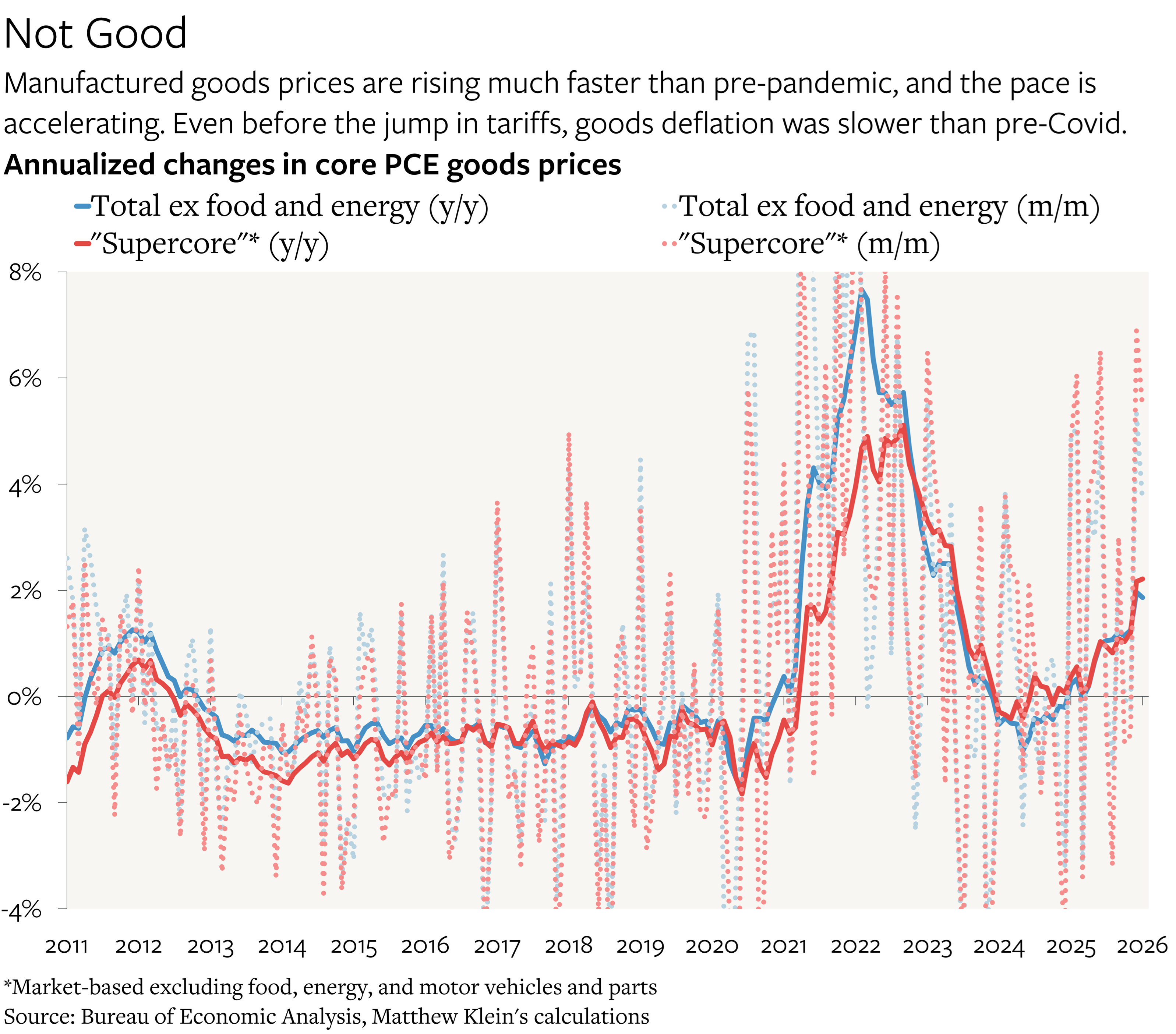

To be fair, goods inflation was getting worse before the Iran conflict, and in some significant categories was worse than in the 2021H2-2022H1 price spike. In the years immediately preceding the pandemic, consumer goods prices regularly fell about 0.5%-1% each year. In 2024, those prices were flat. As of the eve of the war with Iran, consumer goods prices were rising by about 2% a year—and the pace was accelerating.

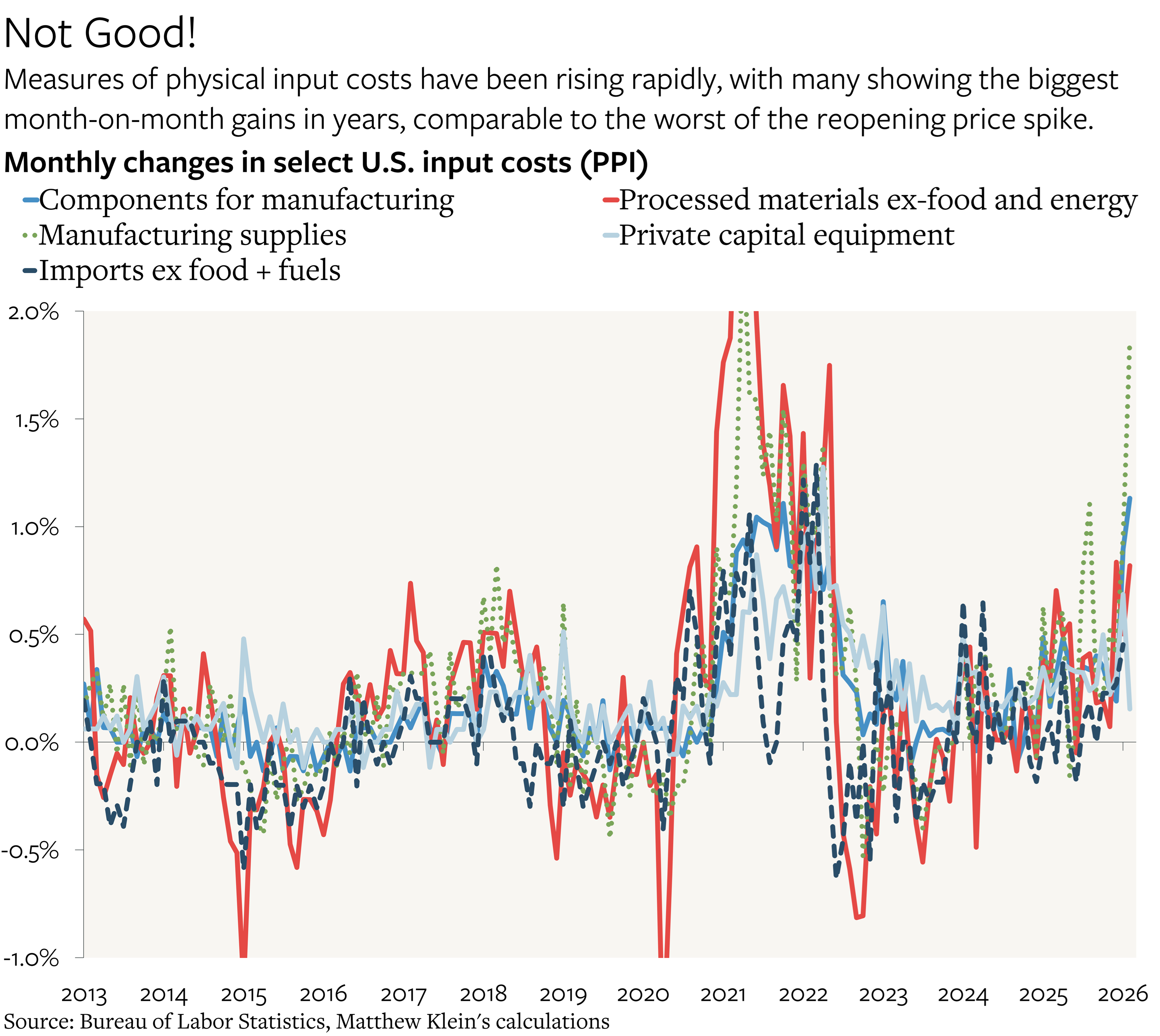

The picture looks worse when focusing on goods purchased by businesses, either as inputs or capital equipment.

Prices of “components for manufacturing” rose by 0.9% in January and by 1.1% in February on a seasonally-adjusted basis. The February increase was larger than in every month of the post-pandemic inflation except for January 2022. Capital equipment prices are rising about 5% annualized, up from about 3% in 2023-2024 and about 1% in the years before the pandemic. Prices of “supplies to manufacturing industries” have been accelerating rapidly, with the one-month increase in February the largest since April 2021.

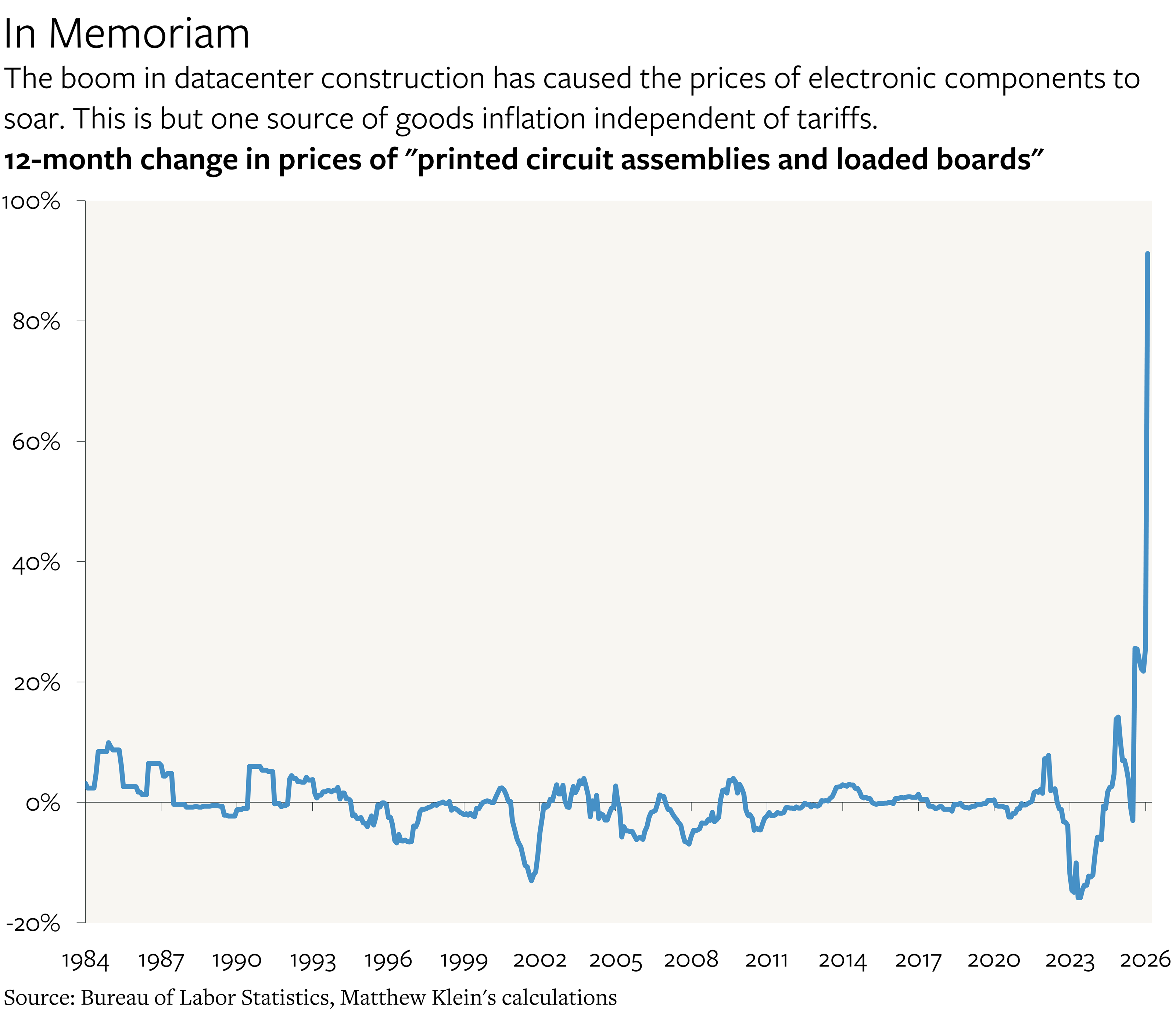

Tariffs are not the only explanation for this. One of the biggest categories within “supplies to manufacturing industries” is “printed circuit assemblies, loaded boards, modules and consumer external modems”, which have mostly been excluded from tariffs because of their importance to the datacenter buildout. Those prices rose by 48% (!!) between January and February. Even if that were a typo, prices rose by 26% between January 2025 and January 2026, which is unprecedented in the history of the data going back to the early 1980s.

While all of this is both significant and unwelcome, it pales in importance to what has been happening with services prices.

The Underlying Inflation Elephant in the Room

Many of the forces affecting the prices of goods are relatively insensitve to changes in U.S. domestic monetary and financial conditions. The same cannot be said for services, which represent the bulk of economic activity, and which, by themselves, should be making Fed officials worry that their 2% inflation target is of reach.