The Squeeze on Russia Is Loosening

The Squeeze on Russia Is Loosening

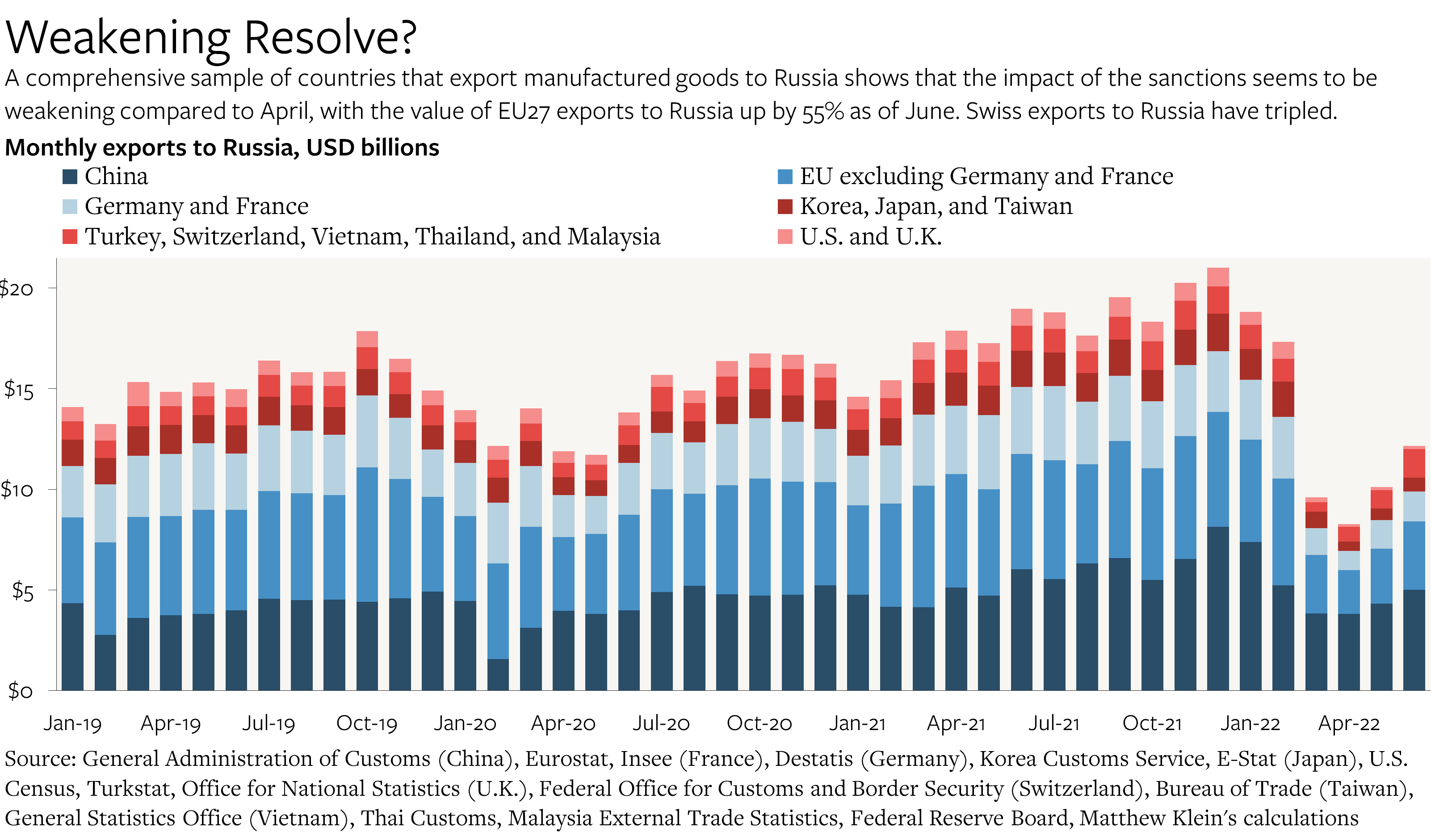

The latest numbers from the major manufacturing powers suggest that exports to Russia are rising.

Exports to Russia from the major manufacturing economies have been rising rapidly since April. If the allies do not act swiftly to tighten the enforcement of sanctions and export controls, the Russian military may be able to replenish its losses of equipment and advanced ammunition—and prolong the war.

Sanctions and the Military Balance

Since at least 2014, the rich democracies have been struggling with the challenge of how to help the Ukrainians defend themselves from Russian aggression without taking any risk.1 The statecraft of the past six months has focused on how to deliver maximum damage to the Russian military without violating this basic constraint.

Until February, the solution was to have elite U.S. and other NATO soldiers train the Ukrainian military and equip them with the best anti-tank weapons, all while trying to warn the Russians that their economy would be harmed if they got too aggressive. Deterrence failed, but so did the Russian blitzkrieg. Providing motivated defenders with (some of) the resources they needed to protect their homes has turned out to be extremely effective.

Once the invasion began, the allies intensified their contributions to the war effort by ramping up their military aid to Ukraine (both materiel and intelligence) and by depriving the Russians of access to critical expertise, parts, and components for weapons and dual-use technologies. As I noted back in April, the Russians were highly vulnerable to a coordinated campaign of denial because they lacked the sophistication and the industrial base to satisfy their domestic needs. This gave the allies the opportunity to use economic sanctions as a form of strategic bombing:

The sanctions should be understood as a weapon deployed on the economic battlefield alongside the Javelines, NLAWs, Stingers, and Neptunes that have proven so helpful to Ukraine’s defense thus far. Those weapons are neutralizing Russia’s existing inventories of tanks, aircraft, and ships, while the sanctions are crippling Russia’s ability to replace those losses by constraining what Russians are able to import…While it would be inappropriate for NATO aircraft to bomb Russian tank factories, shipyards, and missile assembly plants today, it would also be unnecessary. The democracies can replicate the effect of well-targeted bombing runs with the right set of sanctions precisely because the Russian military depends on imported equipment from the very same set of countries it has angered with its brutal attack on Ukraine.

The effectiveness of the sanctions should therefore be viewed from the context of military attrition. The Russians may have started from a position of superior firepower, but the allies’ use of sanctions, intelligence support, and weapons donations has been shifting the balance of forces increasingly in favor of the Ukrainians.

Unfortunately, the latest trade data are a warning that tighter export controls and more stringent sanctions may be necessary to ensure the continued success of this strategy. Boosting both the quantity and quality (i.e., more long-range weapons) of military aid being delivered to Ukraine should be a top priority for the allies in any case, but it will be especially important if the allies believe that they cannot tighten the sanctions regime.2

Tracking Russian Imports

The Russian government has stopped publishing monthly data on imports, but it is possible to reconstruct the data by looking at customs numbers from the main manufacturing countries. For the past several months I have been tracking a sample of 39 countries that collectively accounted for 72% of Russia’s pre-war imports of goods—and essentially all of Russia’s imports of high-tech goods.3

In April 2022, the monthly dollar value of exports to Russia from this sample of countries was 57% lower, on average, than in September 2021-February 2022. Notably, businesses operating in neutral or ostensibly pro-Russian countries—such as China, India, and Vietnam—slashed their exports to Russia at least as much as businesses in countries that formally participated in the sanctions.4

Since then, however, exports to Russia have been rising steadily. As of June, the latest month for which we have comprehensive data, the dollar value of exports to Russia across the broad sample was 47% higher than the trough in April, with the majority of that increase attributable to the EU27, Switzerland, Korea, and Japan—all of which are ostensibly participating in the sanctions.

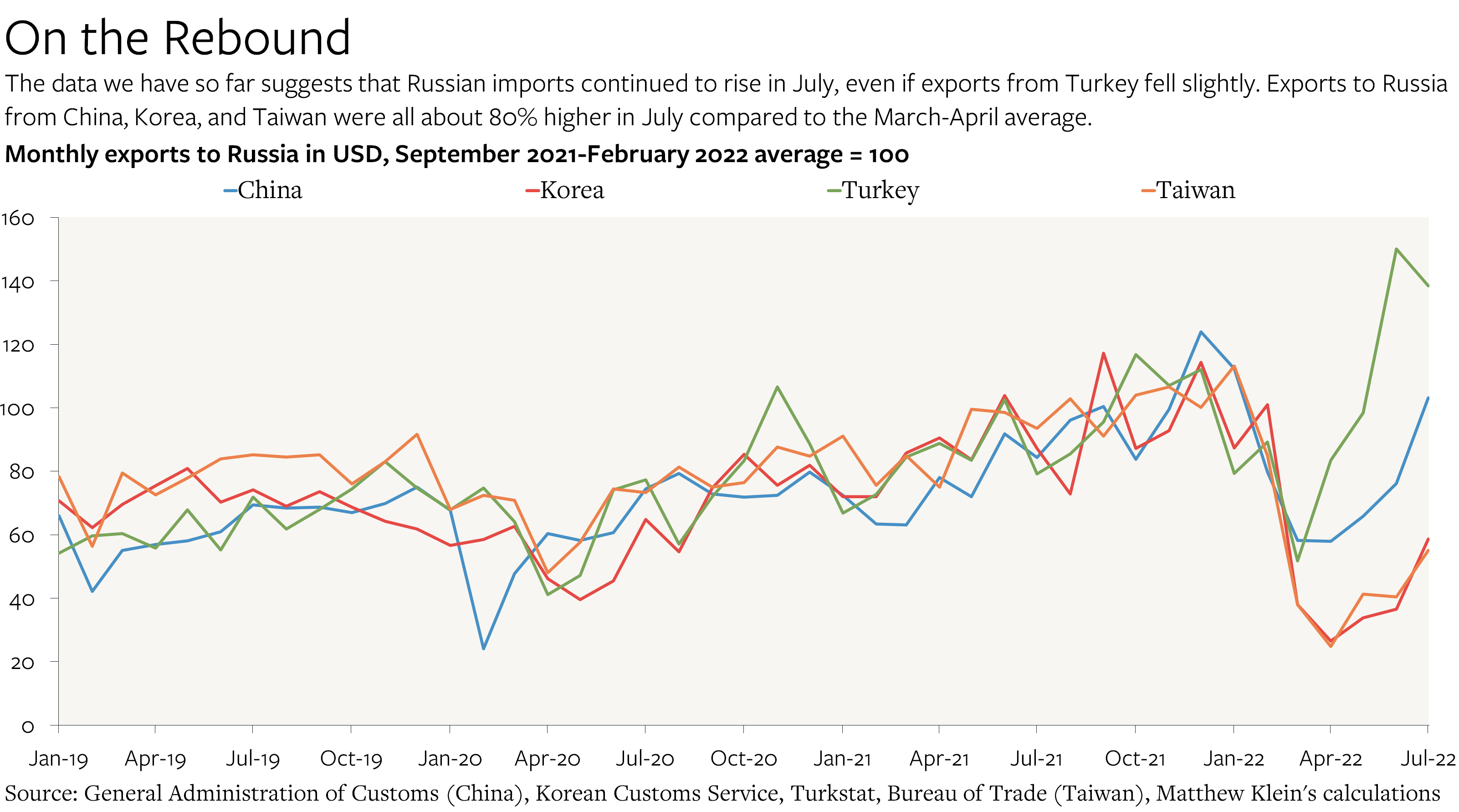

Preliminary data from July suggest that the Russians’ situation has continued to improve.

Last week, China’s General Administration of Customs (GACC) revealed that the U.S. dollar value of the country’s exports to Russia in July had soared by 35% compared to June. For the first time since the invasion began, Chinese exports to Russia were worth more than the September 2021-February 2022 monthly average. Taiwan’s customs services reports that exports to Russia in July were 36% higher than in June, while Korean data show exports to Russia up a whopping 61%. For all three countries, the value of exports in July was about 80% higher in July than the March-April average. The exception so far is Turkey, where exports in July fell slightly compared to June, although Turkish exports to Russia remain about 40% higher than the pre-invasion average.

The Types of Exports Matter

Not all exports are equally helpful to the Russian war effort. Access to fresh vegetables and luxury handbags do not make a difference on the battlefield even if they affect Muscovites’ quality of life (and could therefore have an indirect impact on popular support for the regime). For our purposes, what matters are Russia’s imports of electronics, machinery, and other high-tech components.

The good news is that the increase in Russian imports in May and June was largely attributable to goods that don’t have direct military value.5 As of June, the value of Russian imports of goods with dual-use potential, including machinery, electrical equipment, and vehicles, was about 52% lower than the pre-invasion average, while imports of all other manufacted goods were down by only 18%.

The bad news is that the value of dual use exports was nevertheless rising, mainly thanks to an uptick in exports of industrial machinery and electronics from the EU27. Total exports of dual-use goods to Russia from my broad sample were worth $4.6 billion in June, up from $3.4 billion in April. Most of the increase can be attributed to the Europeans, where exports rose by 80%. Turkish exports of dual-use goods remain below the pre-invasion average.

Worse, the initial data for July suggest that allied pressure may be easing further. Korean exports of dual-use goods to Russia last month were up by 140% compared to the April-May average thanks to a surge in deliveries of aerospace goods, mechanical machinery, and motor vehicles and parts.

The big question is China. GACC hasn’t yet published the detailed numbers on Chinese exports by type of product, only by destination. As of June, Chinese exports to Russia had been rising thanks to higher shipments of non-military goods. Was that what happened in July, or did businesses there follow the path of their Korean counterparts?

I will keep you updated as the data are released. My next note will cover recent developments in Russia’s domestic economy and what we can learn from their balance of payments.

Western Europeans had been unwilling to jeopardize their substantial commercial relationships with Russia after the Russian attack on Ukraine in 2014. (The notable exception was Francois Hollande’s decision to cancel the delivery of French-made warships to the Russian Navy.) Russia was a sizable export market for industrial and luxury goods and an essential supplier of energy, metals, and other commodities. Wealthy Russians were also lucrative customers of financial and legal services, as well as major investors in residential property. German Chancellor Angela Merkel’s stubborn determination to shut down the country’s nuclear power stations and simultaneously increase German imports of Russian natural gas via the (uncompleted) Nord Stream 2 pipeline was especially craven, but far from unique. The Trump Administration, pressured by Congress, went so far as to impose sanctions on the project in 2017 and again in 2019 after the Obama team’s gentler admonitions failed to persuade the Europeans to reconsider.

Ukraine’s civilian economy also needs support from the allies. The immediate task is to provide enough hard currency to pay for imports and service pre-war obligations. After that comes reconstruction.

While I have not been tracking Indian exports to Russia on a monthly basis, it’s worth noting that the dollar value of Indian exports to Russia in 2022Q2 was 38% lower than in 2021Q2. India is not a meaningful supplier of the goods that Russia needs, nor is it a significant exporter to Russia. In fact, the Indian military has historically been a major importer of Russian-made weapons, which helps explain why the Indian government has ostentatiously refused to join the other democracies in support of Ukraine. Still, the visible impact of the sanctions on the export data is revealing.

I described my methodology in more detail in my previous note on the subject. Medicinal goods could potentially be considered dual-use insofar as they may limit the battlefield losses of Russian soldiers, but I have not classified those goods that way in this analysis. Surging exports of pharmaceuticals helps explain the recent boom in Swiss exports to Russia.

As always your analysis are the best. These data are quite worrying; particularly the imports from South Korea, Germany, Sweden and Italy are among the ones that can indicate building up the structure of Russia war machine (precision machineries and electronics).

I wonder if Ukraine would lodge a complaint....but of course who to? Would seem a few well aimed missives to shareholders may be in order.