Guest Post: Toby Nangle on Why Asset Managers Should Refuse Bad Clients

The case against working for sovereigns that violate human rights.

This is a guest piece from Toby Nangle. Formerly the Global Head of Asset Allocation at Columbia Threadneedle EMEA, he resigned last year to focus on improving the ethics of the asset management industry. I am grateful that Toby is willing to explain his thinking for readers of The Overshoot. Those looking for additional information and ways to get involved to should go to Toby’s website, Principals with Principles. I lightly edited the text, but the words, ideas, and images are all Toby’s.

Investment management is a great profession to be in. In terms of mental stimulation, it’s off the charts. And it doesn’t pay badly either. At its core, the job consists of working to help make your clients wealthier. Some use this enhanced wealth to send their children to college. Some use it to honor pension promises made to their employees. And some use it to murder journalists, crush internal dissent and conduct genocide on a minority population.

Given that financial wealth exists solely to provide agency to its owner, it is not a stretch to argue that this wealth has an ethical character related to its owner. Asset managers act as principals when they choose which clients to seek to serve and in what capacity. And the decision to work specifically to enhance a client’s financial wealth has an ethical character that is related to the character of that client.

The Chinese state’s actions in Xinjiang are well-documented. Over a million Uyghers have been incarcerated. Sexualised violence, forced sterilisation and routine torture of inmates have become normalised. This has all been laid-out in the United Nations report in August 2022, annual U.S. State Department country reports, U.K. Parliamentary reports, as well as by numerous NGOs and books.

But decades of current account surpluses have left the Chinese state sufficiently asset rich that its official assets—in the form of abundant and substantial mandates from the Chinese Investment Corporation (CIC) and the State Administration of Foreign Exchange (SAFE)—are hungrily sought after by international asset management firms. In managing these Chinese state assets, investment managers become outsourced Chinese treasury officials, working assiduously to boost the financial resources of their master.

The Chinese state is not alone in having both substantial state wealth and an appetite for engaging in crimes against humanity. It is just the largest and most obvious example.

“Because that’s where the money is”

Sovereign wealth funds (SWFs) hold an estimated $10.7 trillion. Of this, around $6.4 trillion is held by states classed as “Not Free” by Freedom House. Only $2.3 trillion is held by states classed as “Free”—$1.2 trillion of which is Norway alone.

Of the ~$13 trillion in foreign exchange reserves estimated by the IMF, around $5 trillion are accounted for by states classed as “Not Free”. Among public pension funds, “Not Free” states are less important, accounting for only $0.4 trillion of the ~$14.7 trillion market. After correcting for some double-counting, “Not Free” states look to control some $9.0 trillion of SWFs, public pension funds and Central Bank reserves.

To put this in context, the total assets under management for the top fifty investment management firms sums to just over $90 trillion. Official assets are big-game trophy clients for asset management firms.

Source: Author’s calculations based on data from Global SWF and Freedom House, 2022. See an interactive version in Tableau here.

The degree to which sovereign wealth funds of “Not Free” states deploy external investment managers tends not be publicly disclosed by either client or manager. Besides BlackRock and SSGA—which report that they managed $316bn and $479bn respectively in mandates for official institutions such as central banks, sovereign wealth funds, and government ministries at year-end 2021—no other top ten firm by assets under management splits out this figure in their annual report. Others make more or less vague reference to the business. For example, JP Morgan Asset Management boasts that it does business with 60% of the world’s largest pension funds, central banks and sovereign wealth funds.

The $1.4 trillion CIC is more forthcoming than many in confirming that it has over 60% of its Global Investment Portfolio farmed out to external managers, but does not go into further detail. The Azerbaijani State Oil Fund (SOFAZ) sits alone among sovereign wealth funds of states rated “Not Free” in providing a detailed breakdown of its external manager allocations by mandate value and asset class. Forty mandates worth a collective $10.7bn are split between thirty-five managers across five asset classes.

The vast majority of assets managed are run by firms with a strong public commitment to ESG. Ninety percent of the externally-managed assets are managed by firms that are signatories of the UN Principles of Responsible Investment. Sixty percent of the assets are managed by firms that are signatories to the UN Global Compact. Twenty percent of the assets are managed by firms who are members of the Investors’ Alliance for Human Rights.

Source: SOFAZ Annual Report 2020. See an interactive version on Flourish here.

But as one CEO of a large asset management firm put it to me: 1) the decision to turn away business based on any ethical concern is “above my pay-grade”; 2) there are many shades of grey, and this makes any ethical decision far from straightforward.

They were right on both counts. Senior managers are just that. They work for their shareholders, and significant business decisions are “above their pay grade”. They need a business case that their boards can interrogate and back. And ethical norms are contested, culturally-rooted, and evolving. This makes any distinction between “good” and “bad” states contentious, to say the least, as well as smelling distinctly neo-colonial.

Even so, asset managers have many reasons to avoid working for authoritarian regimes that are widely understood to be committing severe human rights violations of irremediable character. The industry has already committed to fulfill a social purpose beyond next-quarter profit-maximization, in part because executives have realized that it increases commercial resilience, a healthy corporate culture, and brand values attached to responsible capitalism. Many clients care about investing responsibly, and have asked their investment managers to commit to practices that are consistent with their values. Human rights may not yet get the same level of attention as environmental concerns or other issues, but managing sovereign wealth from repressive countries does present material business risks.

The rights-based case for change

The UN Global Compact is the world’s largest corporate sustainability initiative in which signatory firms pledge to operate in ways that, at a minimum, meet fundamental responsibilities in the areas of human rights, labour, environment and anti-corruption. The first of the UN Global Compact’s Ten Principles is that “businesses should support and respect the protection of internationally proclaimed human rights”, with Principle 2 adding that businesses must “make sure that they are not complicit in human rights abuses”.

This has implications for asset managers. In a joint note, the Global Compact and the Office of the High Commissioner for Human Rights (OHCHR) point signatories to the UN Guiding Principles on Business and Human Rights (UNGPs) when looking to put their Global Compact commitments into practice. Under UNGPs, firms managing portfolios for states engaged in serious human rights violations are “directly connected” to these violations under UNGPs.1

UNGPs are not currently enforceable in any court of law, despite efforts to incorporate them into the European Commission’s Supply Chain Directive and the ongoing inter-governmental efforts to turn UNGPs into a binding international treaty. Instead, they simply serve as the bedrock on which analyses of businesses human rights responsibilities are built. As the canonical text for business and human rights, they are integral to the OECD Guidelines for Multinational Enterprises, UN Global Compact, as well as private understandings of human rights across the ESG world.

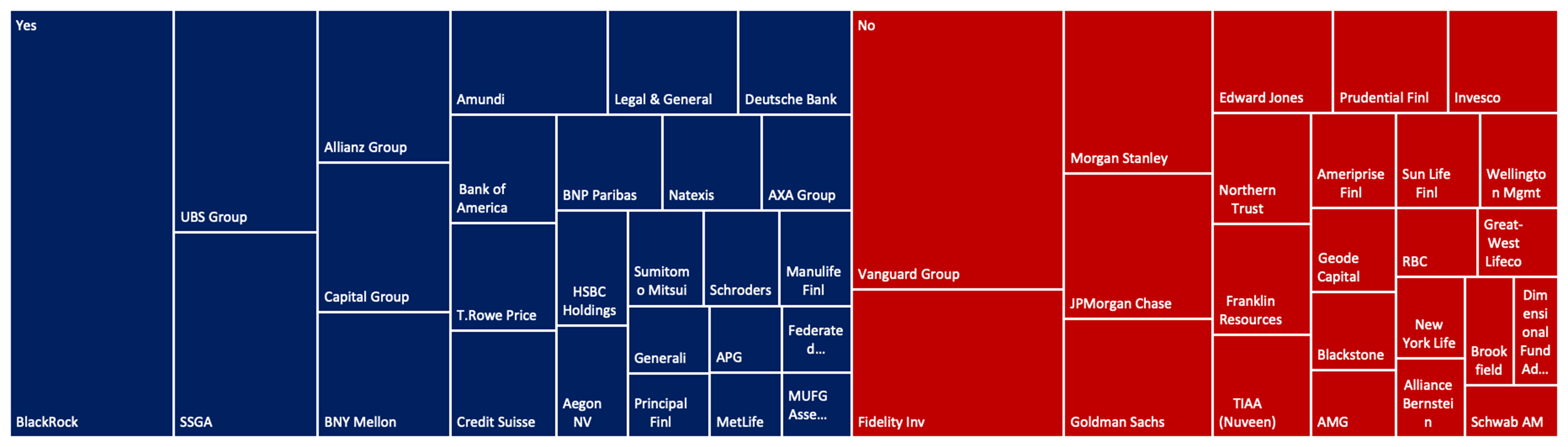

Just over half of the top fifty firms by assets under management, as well as by number, are signatories to the UN Global Compact. In joining the Compact firms commit to apply the UNGPs to their own business practices. Any of these firms accruing “direct linkage” to serious human rights violations by selling their services to clients engaged in serious human rights violations runs elevated reputational risk. Being put on a breach list or being ejected from the UN Global Compact for accruing direct linkage to crimes against humanity is not, after all, a great look.

Largest 50 Asset Managers by Assets under Management and UN Global Compact Signatory Status (Blue = signatory; red = non-signatory)

Source: ADV Ratings, United Nations, 2022

Navigating shades of grey

If there is a reputational risk in managing money for problem states, how can these states be identified? How can we solve the “shades of grey” problem?

There are many human rights, and rights entrepreneurs work to further expand the human rights perimeter. It is a hard, perhaps impossible, task for any government in the world to avoid engaging in actions that might transgress human rights. But not all human rights are the same.

Careful readers will have noticed that I keep using the phrase “serious human rights violations”. This has a specific legal meaning. Essentially, it refers to a collection of non-derogable rights over which the International Criminal Court has jurisdiction with reference to the signatories (or territories of signatories) of the Statute of Rome:

Genocide

Crimes against humanity (murder, torture, rape, enforced sterilisation etc)

War crimes (eg, grave breaches of the Geneva Convention)

Crimes of aggression.

Signatory states to the Statute of Rome forgo impunity regarding serious human rights violations, and such breaches can be investigated and prosecuted in the Hague. While an investment manager cannot be not absolved from their responsibility to conduct due diligence on any client, they should take comfort that signatory state clients have made themselves subject to such external scrutiny and forfeited impunity.

But many states have chosen not to sign or ratify the Statute of Rome. Some will have domestic institutions that provide robust checks and balances against an overbearing executive seeking to engage in crimes against humanity, genocide, etc. Reputable and independent third-party data exists that can help us identify the strengths of these institutions, and the level of domestic impunity held by these states.

International IDEA – an intergovernmental organisation composed of member states from every continent and stage of economic development – run a project called the Global State of Democracy Indices. As the name suggests, its focus is on democracy, but perhaps surprisingly, not solely on representative government. Instead, it brings together data on five broad categories of internal checks and balances against impunity: representative government, fundamental rights (eg, access to justice, civil liberties), checks on government (eg, judicial independence), impartial administration (eg, predictability of enforcement), and participatory engagement.

Source: International IDEA, with visualisation by the author. See an interactive version on Flourish here.

I consider states that are flagged as both Authoritarian (a representative government score below 0.4) and also score in the bottom decile against their peers in at least one other category of checks to have very high levels of impunity and as such demand a higher level of human rights client due diligence.

Putting these measures of external and internal impunity together we arrive at a Venn intersection, shown in the diagram below.

The Venn intersection delivers a focus list of 20 states. Around half of them are on financial sanctions lists from the US and the UK due to their serious human rights failings; the other half mostly have financial wealth. The Venn does not obviate the many shades of grey that exist. Nor does it preclude the notion that a state with extremely high levels of impunity will not let this power corrupt them. But it does seem a reasonable basis to approach the shades of grey problem.

States highlighted are not necessarily all engaged in serious human rights abuses, but they do demand higher levels of due diligence. I’ve called this a Common Minimum Standard to firms I’ve so far met. And I am asking firms to either leverage their business relationships to affect change, explain why they are working to increase these states’ financial resources, or cease the relationships.

Staff, society and client trust

The case that fund managers downing tools would make a difference to the victims of states engaging in serious human rights violations is extremely flimsy (at best!). A change in business practices would at most cause some states to become marginally less wealthy. And serving authoritarian regimes brings billions of dollars of revenues to western firms each year, supporting employment and contributing to the vibrancy of financial centres in Boston, New York, London, Paris, Frankfurt and Tokyo.

So why bother? In short, because it’s the right thing to do.

Doing the right thing also increases firms’ commercial resilience.

Trust is hard won and easily lost. Firms that ask their clients to hand over their wealth require trust to survive. They require trust from clients, employees, and society at large.

An investment management firm’s main assets are its corporate culture and human capital. A firm dedicating itself to expand the fiscal capacity of states committing serious human rights abuse will be unable to articulate the higher purpose it needs to inform a healthy culture with authenticity—to attract, retain and engage the best staff. Over 40% of Gen Z and Millennials in senior positions have rejected a job or an assignment based on personal ethics, according to Deloitte.

Asset management firms cannot afford to shrink their prospective talent pool to only those willing to hold their nose. If they think they can, regulators cannot afford to let them. As the FT’s Robert Armstrong put it, “if you work for monsters, fewer people will want to work for you; the ones who will work for you are more likely to be creeps”. This is a bad outcome for firms, as well as for clients and society more generally.

When speaking with regulators in the U.K., the phrase that comes up again and again is “the social license to operate”. The Global Financial Crisis cast a long shadow over the financial sector, and recent problems for U.S. regional and European banks have raised anxiety levels once more about how little trust has been rebuilt over the last fifteen years. The regulatory agenda is fixated on culture, tone from the top and on following through on commitments made. Investment management firms risk their social license when they dance with the devil.

And clients should, and I believe will, care for at least three reasons. Firstly, the notion of entrusting one’s wealth to any organisation whose business practices are so at odds with their widely- and expensively-advertised claims to “responsible capitalism” is a red flag. Secondly, clients often engage in ESG investment strategies because their stakeholders care about ESG. It seems unlikely that, having committed their wealth to such a strategy, they might be indifferent to direct linkages that their manager has to serious human rights violations.

Thirdly, there is a direct issue of financial materiality for clients. Employing a firm whose business is exposed to elevated risks of financial sanctions run a risk; this is elevated further when coinvesting in a strategy with sanction-exposed clients. This is no hypothetical. Following Russia’s invasion of Ukraine, U.K. pension funds found themselves unpicking the problems caused by their managers’ lack of client human rights due diligence. Some are in the process of rewriting their RFPs to extract information from managers about their direct linkages to serious human rights violations.

A way forward

The way forward is uncomplicated.

Firms can commit to a comply or explain regime: ceasing to manage mandates for official clients in states failing to clear the Common Minimum Standard outlined above, or explaining why listed state clients were being served. In so doing firms would be able to signal their alignment with a values-based purpose, garnering higher engagement from existing and prospective employees, clients and other stakeholders.

Asset management is a great industry to work in. And it has got some outstanding people. I found no opportunity to change practices from within, and the moral injury attached to sustained complicity led me to leave. Since writing about the reasons for quitting last year what was a big job at a large firm in the FT, I’ve been inundated by messages of support from people in the industry. Some outstanding and well-known investors have related to me their own experiences, ranging from profound discomfort with their firms’ client roster, to their quiet (or in some cases noisy!) success in sabotaging their firms’ efforts to win or retain certain sovereign clients.

With the rise of passive investing, active fund management as an industry has been sustained mostly by rising asset prices and waves of consolidation. Net client flows out of active have been a one-way street for a decade or more, and fee rates have compressed. In this context, C-suiters have been more than courteous in meeting me, when the bottom-line of my ask would see them voluntarily turn away one of the few new sources of client business. In the famous words of Upton Sinclair, “it is difficult to get a man to understand something, when his salary depends on his not understanding it.”

I believe that the positive longer-term reward is there for firms brave enough to embark on the path less travelled. But the main focus of discussion is sizing the immediate risks of carrying on as normal. DWS saw billions wiped from its stock price, its offices raided and its management resign over alleged greenwashing. If rightswashing were perceived to carry comparable risks, minds would be focussed.

I still feel great affection for my interlocutors. Until very recently I stood in their shoes and saw the world through their eyes. Having upended their businesses over the last few years to make ESG central to their firms, having progressed programmes of cultural change, and having championed DEI initiatives, they thought that they were the good guys. They still have an opportunity to prove that they are.

UNGP13 specifies that firms have a responsibility to “seek to prevent or mitigate adverse human rights impacts that are directly linked to their operations, products or services by their business relationships, even if they have not contributed to those impacts.” Clients are business partners. The product/service is the creation of enhanced financial power. These points are neither complicated nor contested.

| A guest post by

|