"Look Through" the Hormuz Shock if You Want. U.S. Inflation is Still Running Hot.

A wide range of underlying measures indicates that prices are rising too fast to be consistent with the Fed's alleged 2% yearly target. Plus: explaining the CPI-PCE gap.

I was only away in Yosemite for a week, but somehow that was long enough for the situation in the Gulf to go from “the U.S. is threatening to commit war crimes unless the Iranians open the Strait of Hormuz” to “the U.S. and Iran have a ceasefire to open the Strait” to “the U.S. has imposed its own blockade on the Strait of Hormuz”.

With export options either limited or non-existent, and with storage facilities filling up, the U.S. Energy Information Administration (EIA) estimates that Saudi Arabia, Kuwait, Iraq, and the United Arab Emirates (UAE) have slashed their combined production of crude oil by about 7.5 million barrels/day in March and will shut-in 9 million barrels/day in April, on average. The EIA further assumes that production in the affected countries will not return to normal until the end of 2026.

Even this may be too optimistic. Rory Johnston estimates that shut-ins could approach 12 million barrels/day if the Strait remains closed through the end of April. Restoring production that has been shut-in will take time, even if there has been no long-term damage as a result of the conflict. While the world’s oil and products consumers went into the crisis with relatively abundant inventories, the shortfall in production is cumulating rapidly. The EIA estimates an inventory drawdown of about 460 million barrels in 2026Q2, much of which so far has been met by the depletion of strategic reserves, while Rory Johnston’s estimate is that there will be about 1 billion missing barrels by the end of July. If the Strait remains even partly closed after the end of this month, which seems plausible, the cumulative production shortfall would be correspondingly larger.

There will also be a time lag associated with shipping. Even if both (?) blockades ended immediately, it would still take at least 20—and quite possibly 30—days to load, ship, and unload crude oil currently held in storage from the Gulf to refineries in Singapore or elsewhere in East Asia.

The hit to supply will force (some) users of oil and refined products to cut their consumption. In a market-based system, this rationing occurs via price increases large enough relative to incomes to persuade—or force—people to buy less. After factoring in higher costs of shipping and insurance, the cost paid by (some) refiners for physical oil in the spot market is now over $200/barrel, even if benchmark futures prices for delivery in a month or so cost much less.

The only way that overall inflation could remain unaffected by soaring energy prices (relative to incomes) would be if non-energy prices and incomes fell.1 But a world where most prices are falling is also one where many businesses will struggle to service their debts and pay their workers and suppliers. As troubled businesses cut their spending, everyone else ends up with less income and is forced into an unwelcome combination of defaults and spending cuts, propagating the downward spiral. Policymakers rightly reject this approach, if they have the option, preferring to tolerate some inflation to manage the shifts in relative prices. This is why the pace of price increases in the rich countries is set to accelerate, at least for a bit.

The question for policymakers is what this “one-time thing”, as Federal Reserve boss Jerome Powell has called it, will do to the underlying trend rate of inflation.

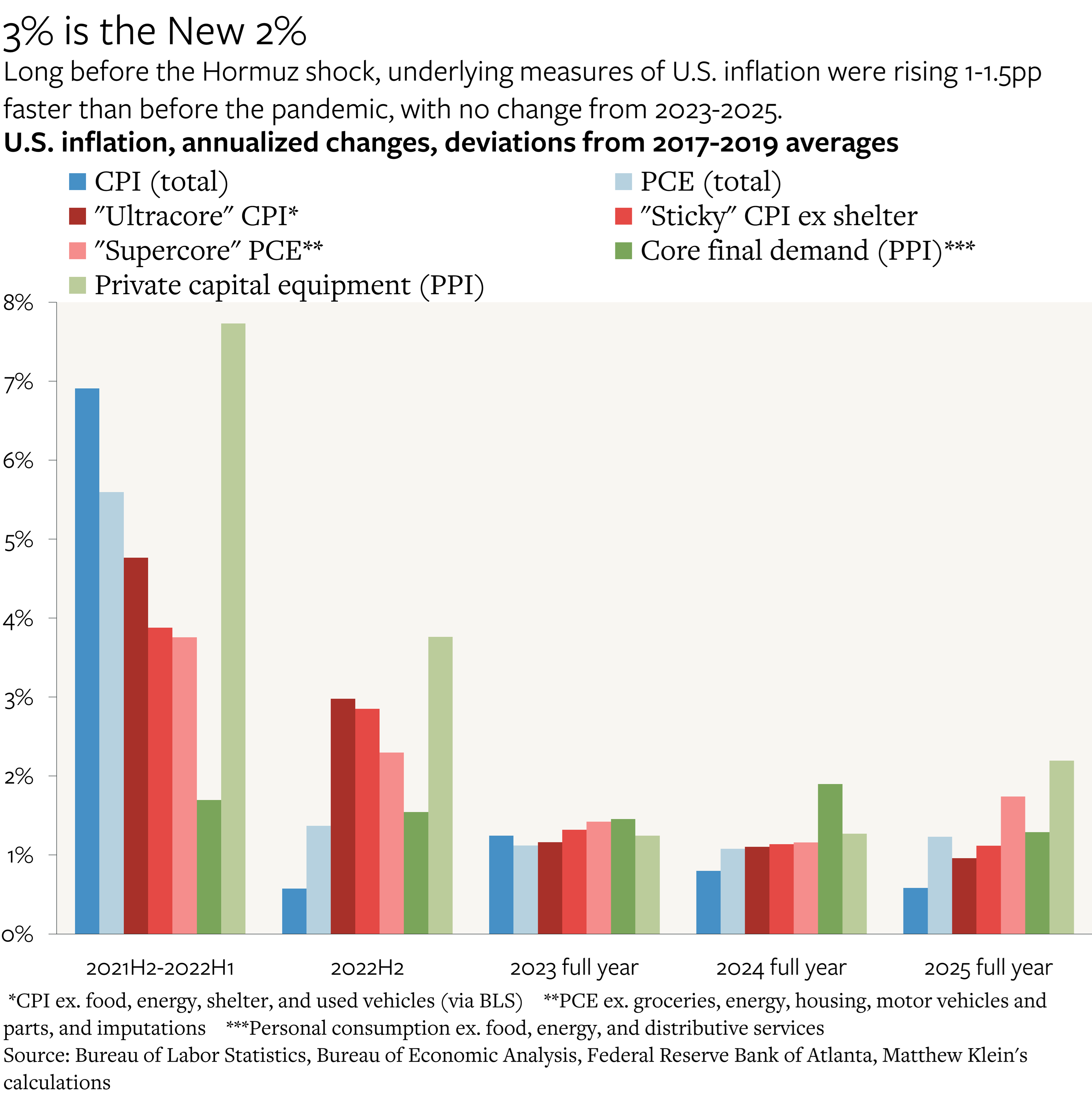

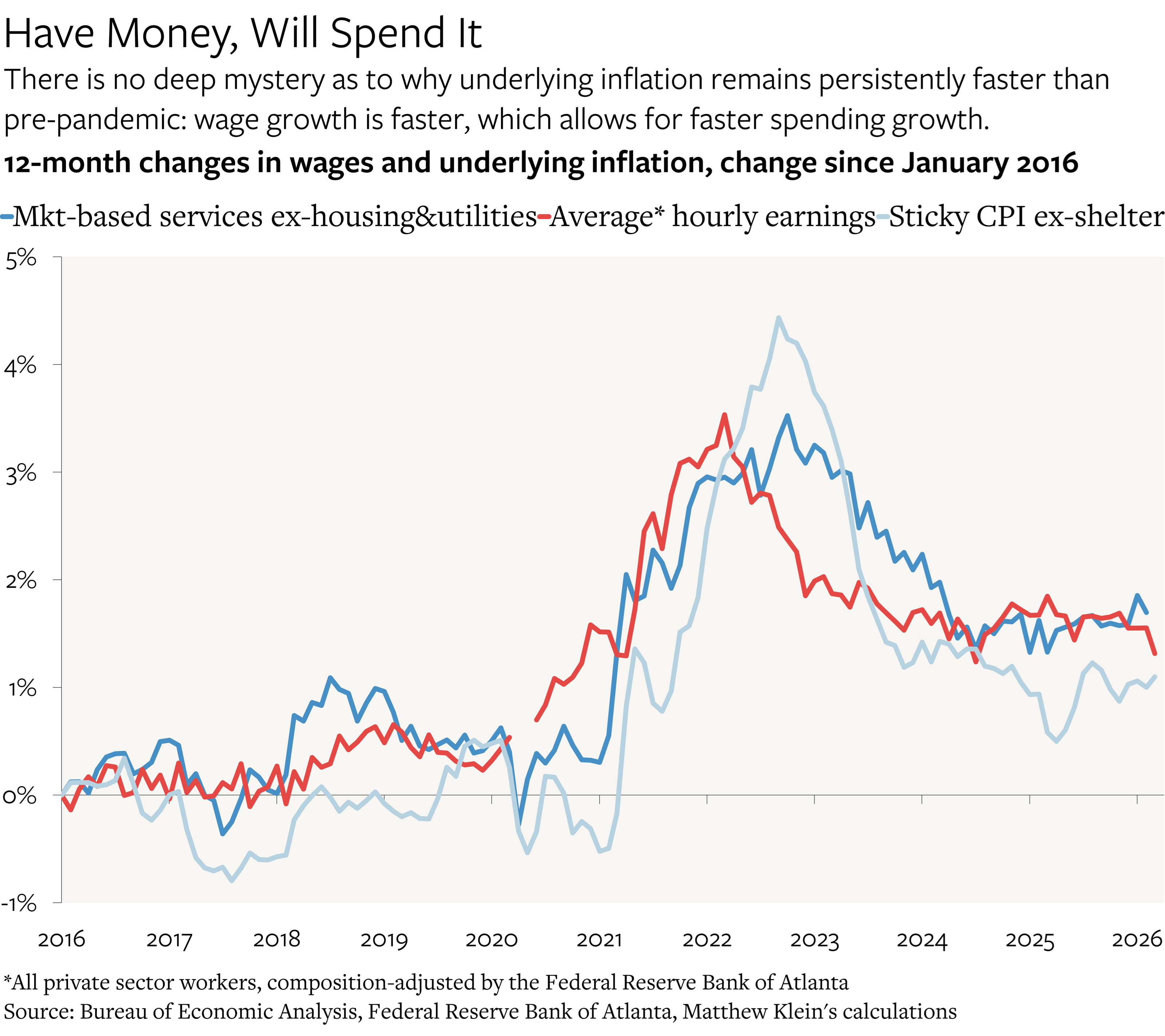

The problem is that Fed officials have spent the past several years believing that inflation would fully revert to normal on its own, and kept lowering interest rates on the basis of this mistaken belief. Yet the Personal Consumption Expenditures (PCE) price index, which is what the Fed officially targets, has been rising remarkably steadily at ~3% annualized ever since the middle of 2022. A wide range of measures that attempt to strip out volatile and idiosyncratic components have shown little change since at least 2023. However you choose to define it, underlying inflation, like wage growth, remains about 1-1.5pp too fast to be consistent with the central bank’s alleged 2% yearly target.

Given all this, the most benign outcome would be for underlying inflation to remain about 1-1.5pp faster than before the pandemic, with officials either tacitly or openly admitting that the target has been revised from 2% to 3%. The pre-pandemic growth rate of nominal income was probably too slow, so there would be nothing inherently wrong with a modest change—at least, as long as officials hold the line against any further acceleration.

There are other, worse, possibilities.

For one thing, Fed officials are still dealing with an administration intent on suborning it to force interest costs lower. Powell is still under threat from a bogus criminal investigation. There is also the risk, as some astute policymakers have warned, that businesses and consumers may reasonably come to suspect that a sustained series of successive policy “shocks” is actually the new normal. Once is happenstance, twice is coincidence, three times is enemy action, etc.

After all, the direct price passthrough from tariffs to overall price indices should have been relatively modest, but there was already some evidence before the war that businesses were using tariffs as an excuse to raise prices even further, with the knowledge that their customers had plenty of purchasing power available to cover the higher costs. It is entirely possible that something similar could happen in response to this “shock”, especially given how many different commodities, from fertilizer to helium, are affected.

By all means, policymakers should “look through” what is happening with energy. But that requires recognizing the persistent pace of price increases in the rest of the economy—and the real possibility that this underlying trend could accelerate further.

The rest of this note is a more detailed breakdown of the latest inflation numbers for March, including a thorough analysis of why a gap has opened up between the Consumer Price Index (CPI) and the PCE.

Rising U.S. Goods Prices Are More About Strong Demand than Constrained Supply

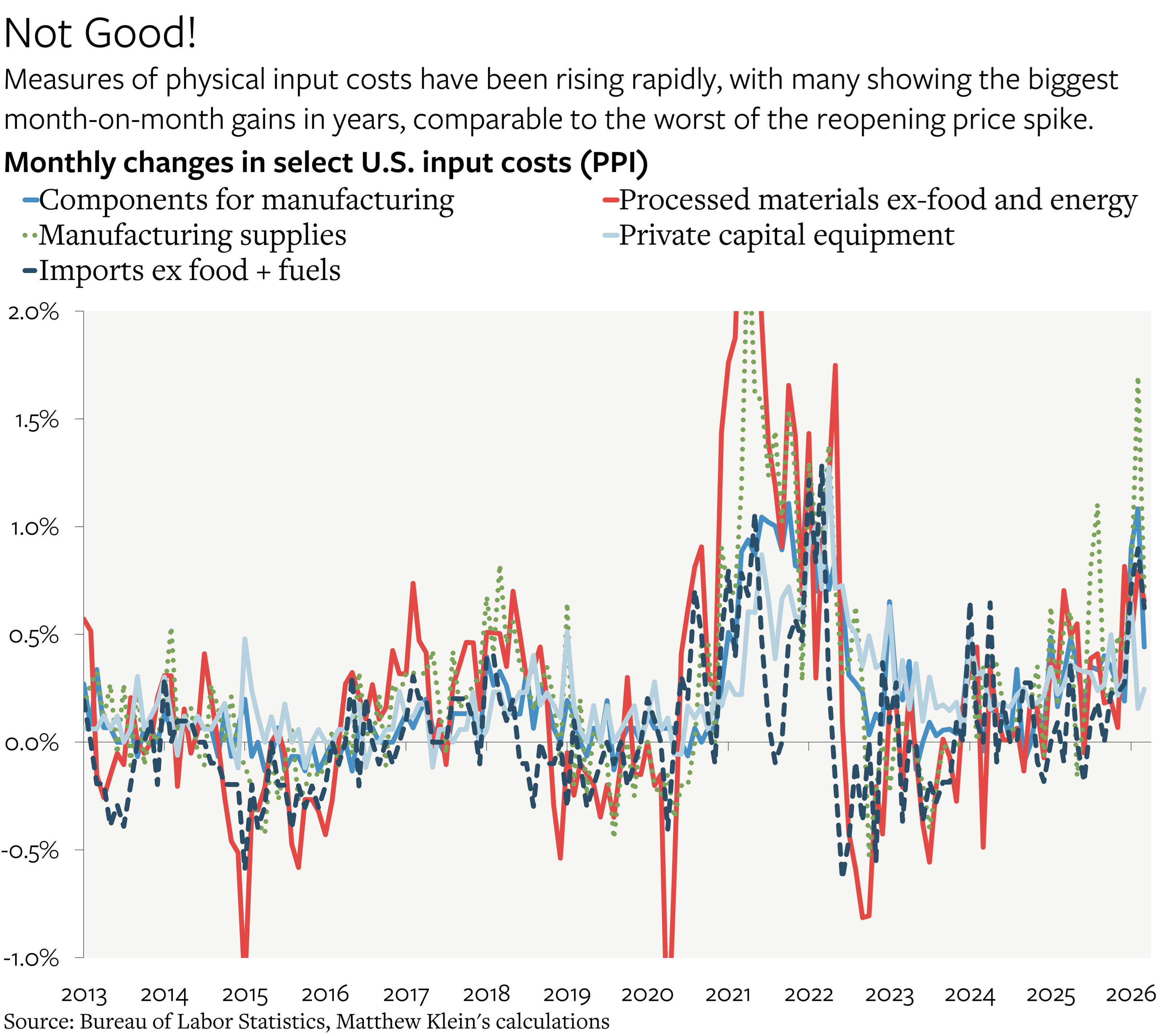

Prices for physical goods were rising faster than at any point outside of the post-pandemic reopening before the Iran War. While some of that can reasonably be attributed to tariffs, tariffs are not the only, or even the main explanation.

There are at least three ways to see this.