The Case for Cutting Rates (or Not) is the Same As It Was Last Year

The most recent data are likely overstating the extent of disinflation, especially given what seems to be happening with goods supply and demand.

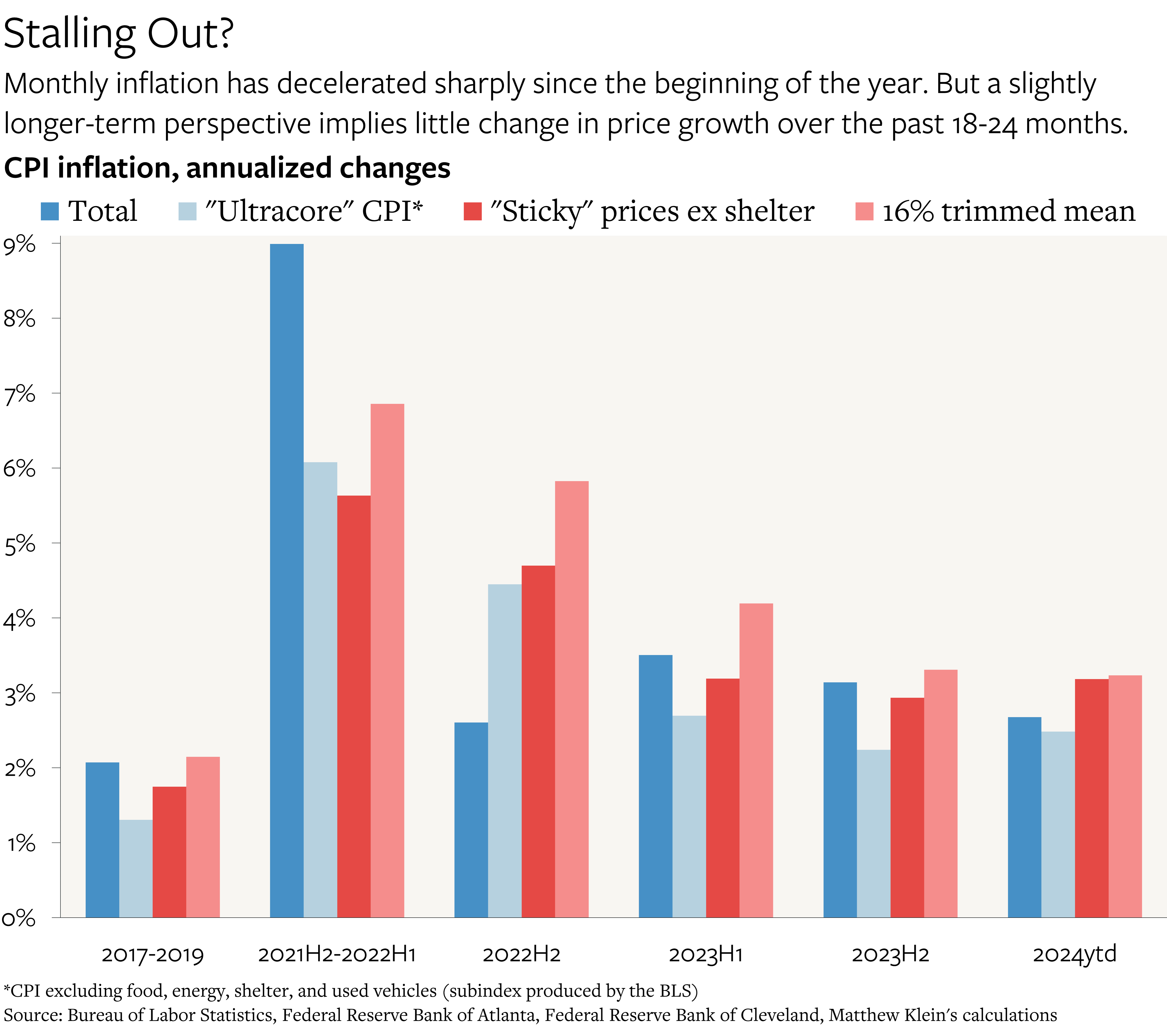

There has been essentially no inflation in the past three months: the U.S. Consumer Price Index (CPI) is up just 0.1% from April-July. The recent sharp slowdown in inflation is also clear in narrower cuts of the data that attempt to strip out volatile or idiosyncratic components.

The question for policymakers is whether this is noise, or indicative of underlying trends. If inflation were actually running close to—or slower than—the Federal Reserve’s 2% goal1, and if the economy were weakening, which the (apparent) slowdown in the job market suggests2, then it would likely be appropriate for monetary conditions to loosen. As of this writing, traders are about evenly split between bets that the Fed will lower short-term interest rates by 0.75 percentage points or by 1+ percentage points by the end of this year.

While easing policy now might be the correct course, the case for doing so is not much stronger now than it was at the end of last year. There were some signs of economic weakness back then, for those inclined to look,3 just as there are some notable signs of strength now. And the underlying inflationary trend so far this year is essentially the same as it was in 2023H1 and 2023H2, if the price bumps in January-April, which overstated the inflationary situation at the time but nevertheless led to sustained increases in the level of the CPI, are not ignored.

Moreover, there are reasons to think that the falling prices of consumer goods, which had been a helpful impulse holding back the overall rate of inflation, may soon start either falling more slowly, flattening out, or even begin to rise slightly.

Inflation Has Not Slowed As Much As It Seems (And That’s Okay)

Prices rarely rise smoothly, and even with seasonal adjustments, there can be plenty of month-to-month volatility that obscures trends. So far, there is no evidence to suggest that the unusually slow pace of price increases since April is anything more than a correction for the unusually rapid price increases in the first few months of the year.

The 12-month change in the CPI from June 2022 to June 2023 was 3.1%, while the 12-month change from July 2023 to July 2024 was 2.9%. That modest slowdown is entirely attributable to the substantial deceleration in rental inflation based on signed leases—which are checked only once every six months. Measures based on listed rents for available units had long implied that this measure of inflation would eventually slow, and it has.

Higher-frequency cuts of the CPI that strip out housing and other volatile or idiosyncratic components4 tell a similar story: underlying CPI inflation is still running around 2.5%-3% a year, just as it has been since the end of 2022. Consistent with the wage data through July, inflation is rising about 1-1.5 percentage points faster at a yearly rate than before the pandemic, although many policymakers think that prices back then were rising too slowly.

If inflation is now slow enough to justify policy recalibration, then policy recalibration would also have been justified by the end of last year. And if prices were rising too fast then, they are still rising too fast now.

I do not know what would be gained by squeezing the last percentage point or so of inflation out of the economy, especially if that came at the cost of impoverishing consumers and reducing business investment.

Short-term interest rates did not need to fall last year to maintain current conditions. Policymakers, however, may worry that inflation will slow substantially in the near future—and that the economy could roll into a downturn—unless policy is recalibrated. While that could happen, it is worth noting that there are several countervailing forces pointing in the other direction.

Goods Supply/Demand and the Disappearing Deflationary Impulse

The prices of durable consumer goods have been falling at the fastest rate in more than two decades. The prices of nondurable goods—mostly groceries, gasoline, clothes, and medicines—have been rising more slowly than at any time outside of oil price crashes. After the unusual and unwelcome spikes in prices attributable to the pandemic and Russia’s war on Ukraine, the recent large declines have been helpful for suppressing the overall inflation rate. But there are reasons to think that the pace price decreases could slow, stop, or even reverse.