The Case for Higher U.S. Rates

Hormuz may be opening up, but the combination of robust growth and stable-to-accelerating underlying inflation suggests that the previous bias to lowering rates was a mistake.

Among other reasons, Kevin Warsh was nominated to run the Federal Reserve because of his insistence that software innovations will lower prices so much that the central bank will need to preemptively lower interest rates just to keep the economy out of a downturn.

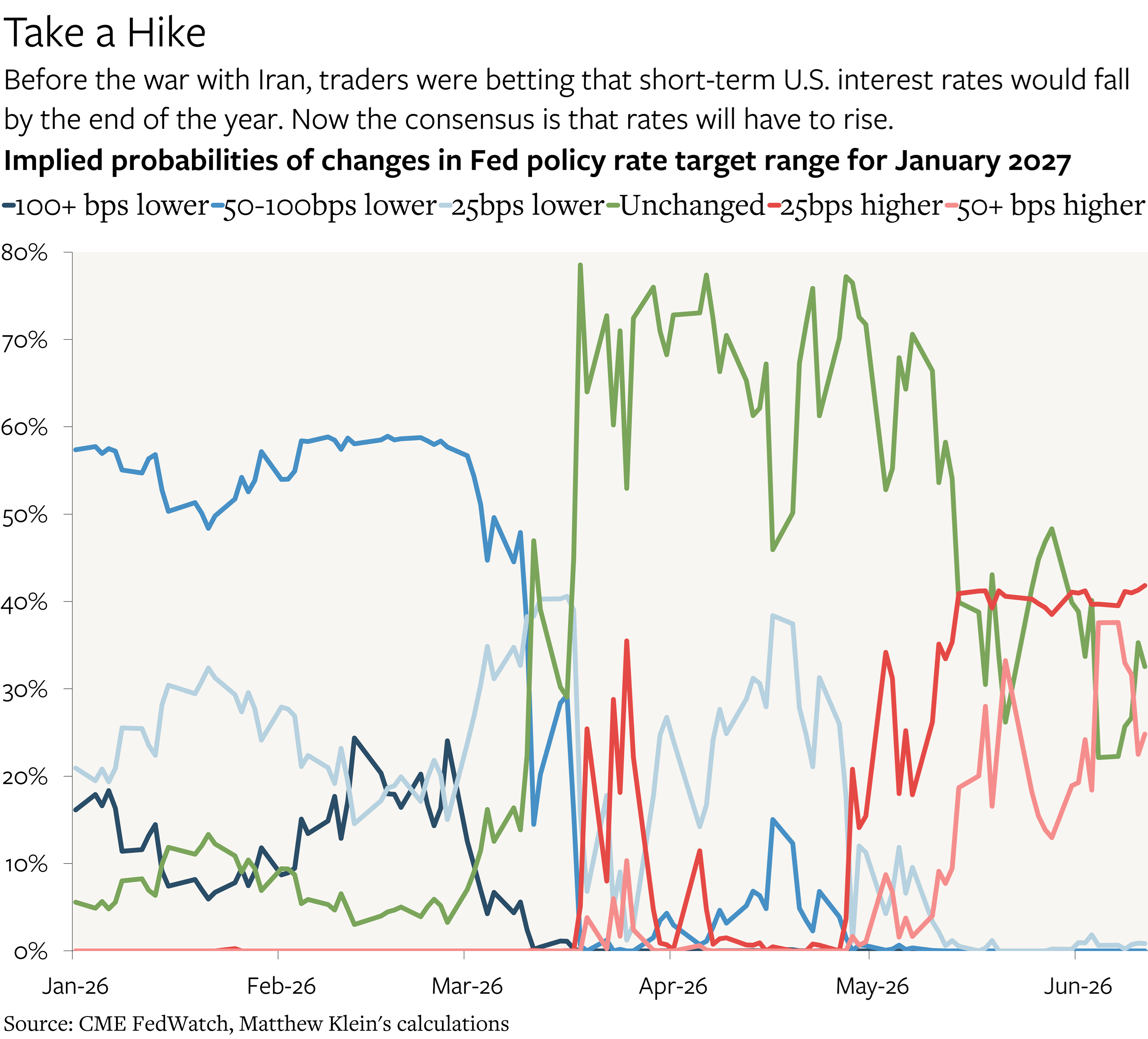

He will soon get to see whether his colleagues on the Fed’s Open Market Committee (FOMC) find those arguments persuasive—or at least persuasive enough to push market pricing back to where it was before the war with Iran.1

The challenge for Warsh, and for his dovish supporters in the administration, is that underlying inflation continues to be persistently faster than the Fed’s official target, and may even be accelerating (slightly). Temporary disruptions associated with the closure of the Strait of Hormuz are not the main problem, which explains why rates pricing has barely budged since the announcement of a ceasefire and, more recently, a deal to reopen the Strait.

Instead, as I have been arguing for some time, most recently back in mid-February, when I suggested that American policymakers could learn from Australia’s experience, the prewar consensus in favor of lowering rates was mistaken. Underlying growth has been much stronger than worrywarts had feared, with the reasonably healthy job market ensuring that wages continue to rise about 1 percentage point faster than in the years immediately preceding the pandemic.

The data over the past four months seem to have convinced traders to come towards my point of view.

The obvious reason is that the job market, consumer spending, and inflation all seem to have accelerated. More important is that this acceleration coincided with a massive spike in commodity prices.

The standard theory is that higher prices for energy and other inputs depress consumption, as well as hiring by non-commodity businesses. The impact might be partly offset by additional investment in commodity extraction, but the net effect tends to be negative outside of a few small economies where commodity production dominates the economy, such as Norway. While I was more optimistic than some about the potential growth impact on the U.S., the fact is that U.S. oil drillers did not respond by increasing output, drilling, or hiring. (They did increase exports by running down commercial inventories, however.)

The implication is that growth would likely have been even stronger if not for the conflict with Iran, which in turn means that the easing of constraints on shipping through Hormuz should create an additional boost to growth, and quite possibly to underlying inflation. In those circumstances, rate cuts would not be appropriate—but rate increases would be.