The Win-Win Solution to "China Shock 2.0"

The best way to address the concerns of China's trade partners is to let the Chinese people live better.

I will be in Dalian on June 23-25 for the World Economic Forum’s Annual Meeting of the New Champions. I will be giving a short presentation on “A World Out of Balance” on June 23 at 10:00 local time, which I believe can be viewed online at this link. If you are around, please come by and say hi!

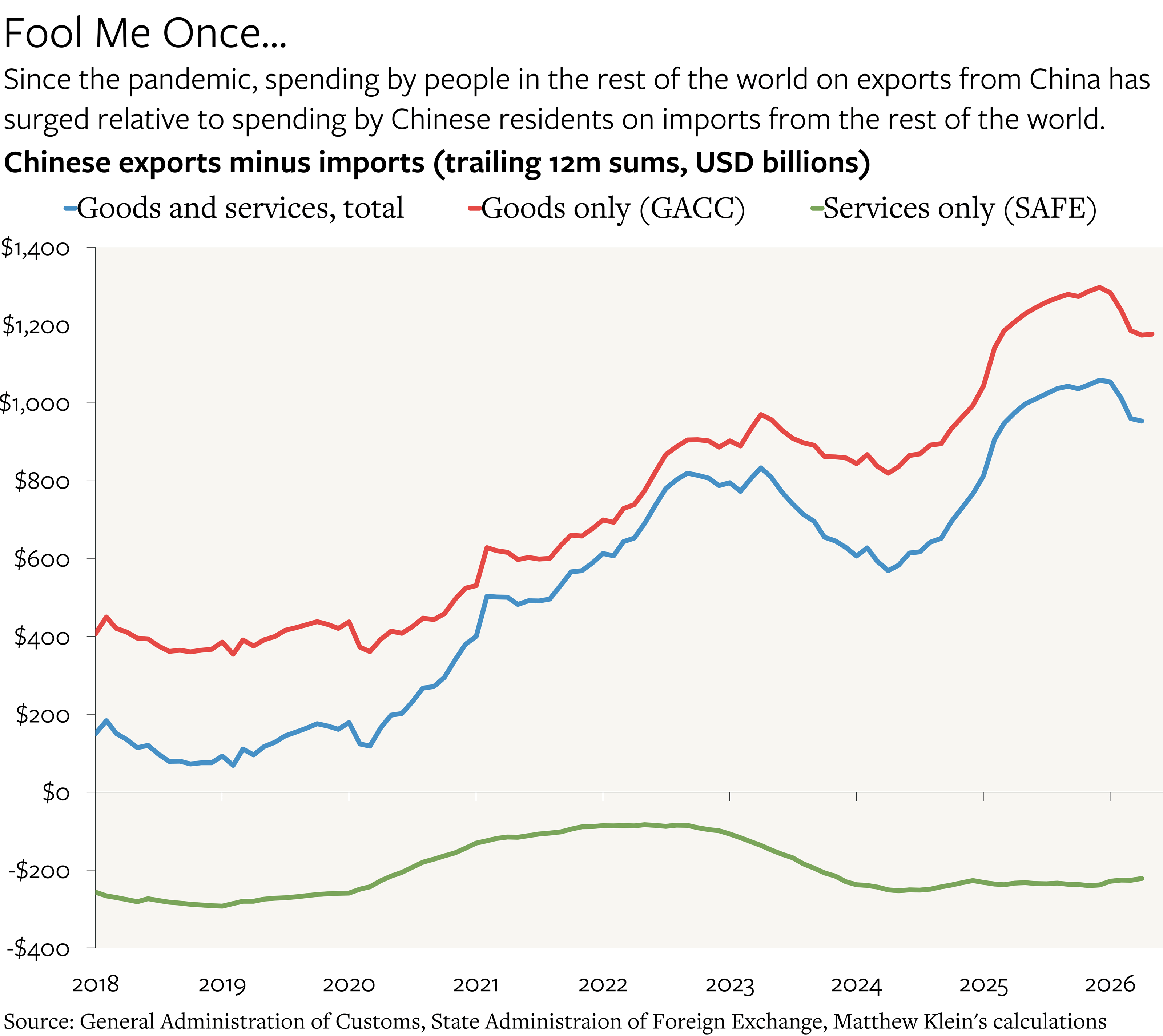

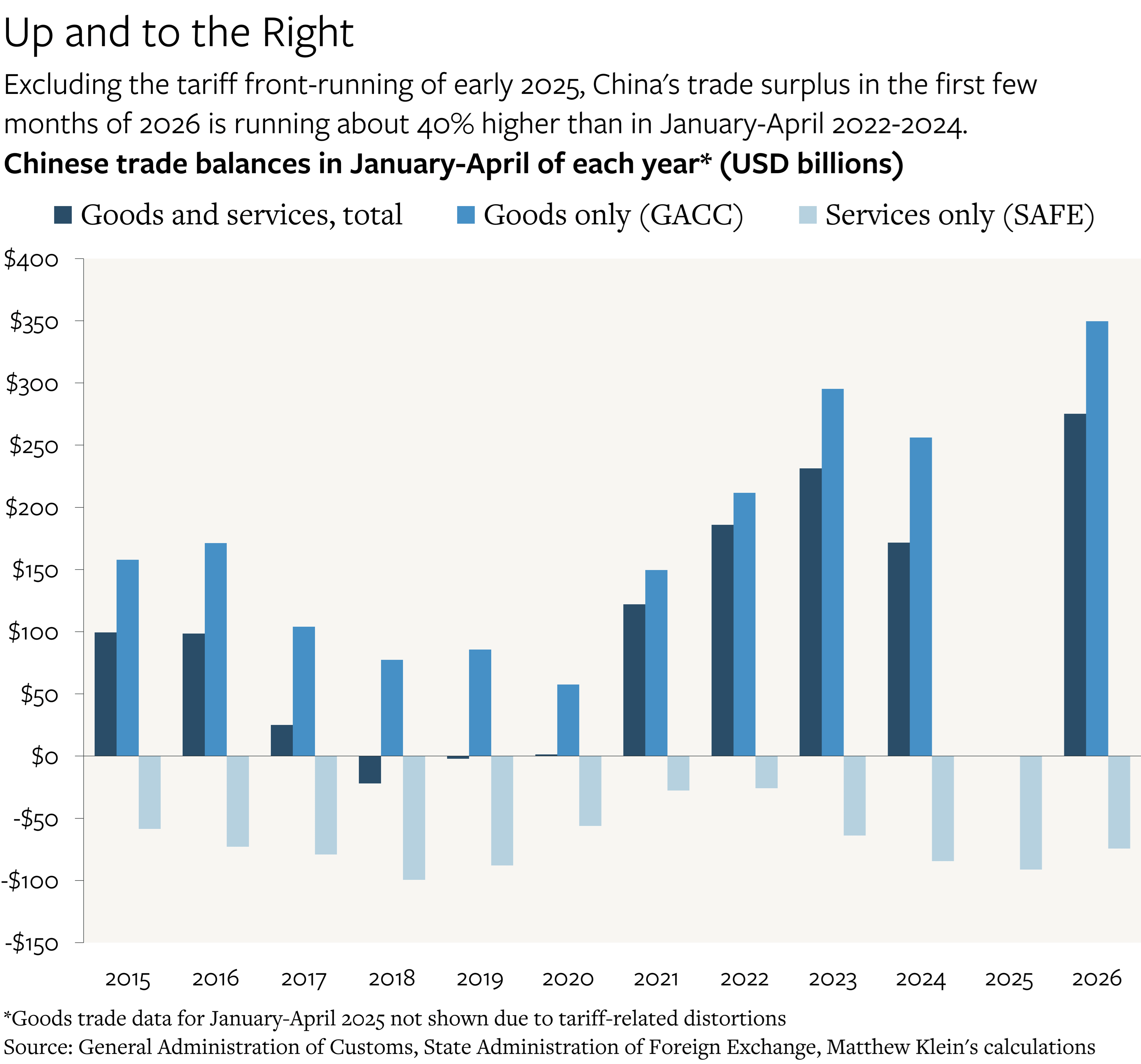

In 2025, the last full year for which we have data, Chinese residents sold about $4.5 trillion in goods and services to people in the rest of the world, but spent just $3.4 trillion on goods and services produced outside of China. In 2017-2019, the gap was only $140 billion/year on average.1 So far in 2026, China’s trade surplus in goods and services is 40% larger than the 2022-2024 average for January-April.2

This is an increasingly serious problem for people outside China. Surging Chinese exports crowd out sales by non-Chinese producers both in their home markets and in third countries, while weak Chinese import demand means that there is little ability to make up the lost revenues by selling output made abroad in China itself.

Europeans, who were relatively unbothered the last time this happened, are now seriously concerned—although not yet enough to actually agree to do anything. The French government made “global imbalances” the centerpiece of their agenda for this year’s G7 meeting, commissioned a report on the subject from some of the world’s leading academics, and has pushed for the introduction of Europe-wide tariffs to protect against “unfair” competition.

Perhaps even more significant is the work of Sander Tordoir and Brad Setser, who published a paper on “The Cost of Germany’s Complacency” a month ago.3 According to Handelsblatt, their work has been instrumental in shifting elite opinion within Germany, which has historically been dismissive about both the dangers of global imbalances and the usefulness of government intervention in the markets. At the G7 meeting, Chancellor Merz was explicit about the need to “address” the “competitive disadvantage” caused by the undervaluation of China’s currency on international markets, although he did not mention “China” by name.

Their motivation is straightforward: as Chinese manufacturers have become increasingly sophisticated, the old moats that protected European companies from the direct effects of Chinese underconsumption have been filled in.4

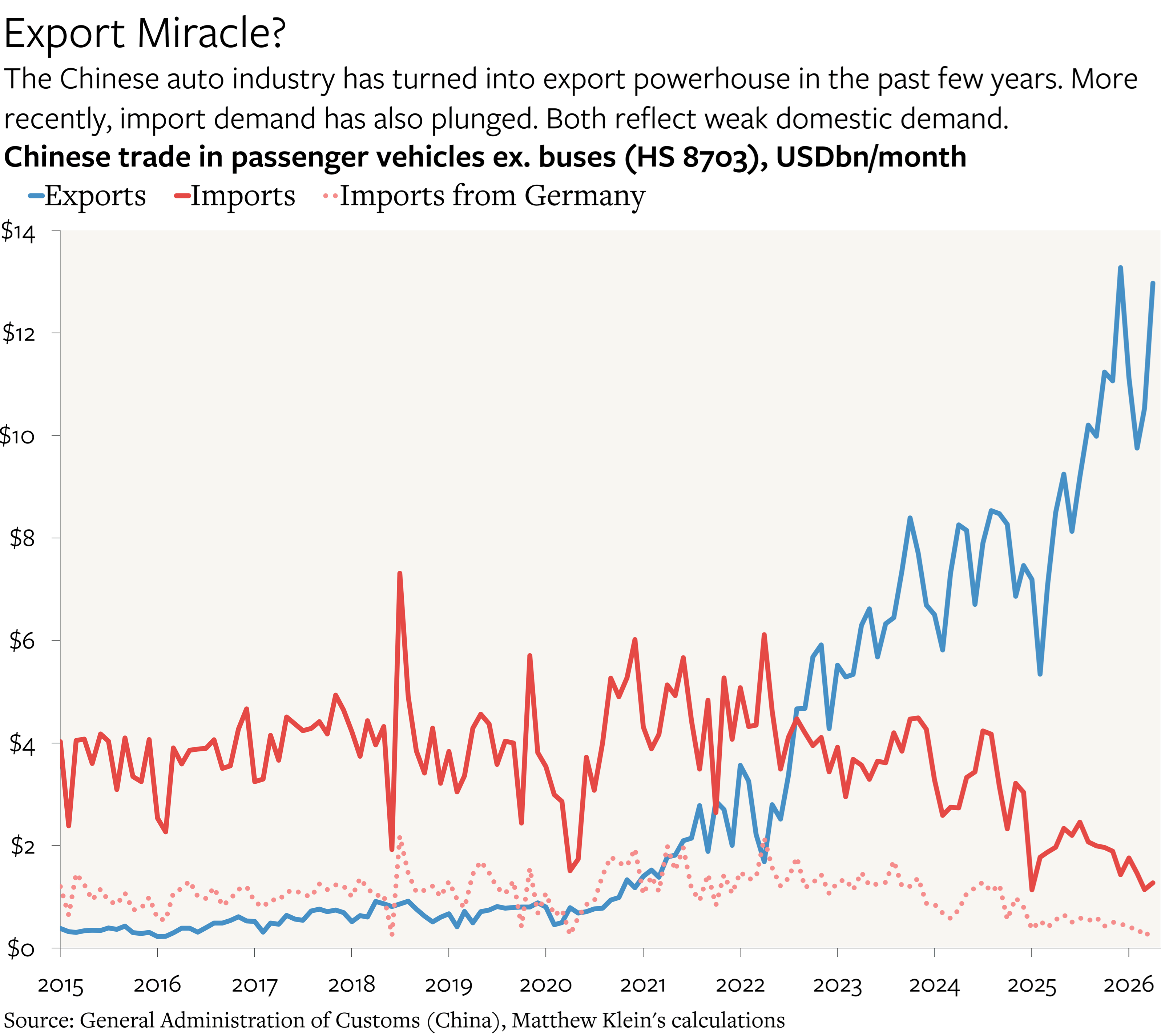

This is perhaps most obvious in the case of motor vehicles (HS8703). Excluding January-July 2020, Chinese residents consistently spent about $50 billion/year on imported cars and light trucks from 2017 through 2023, of which $15 billion/year went directly to Germany. (German-branded cars made and sold in China are counted separately.)

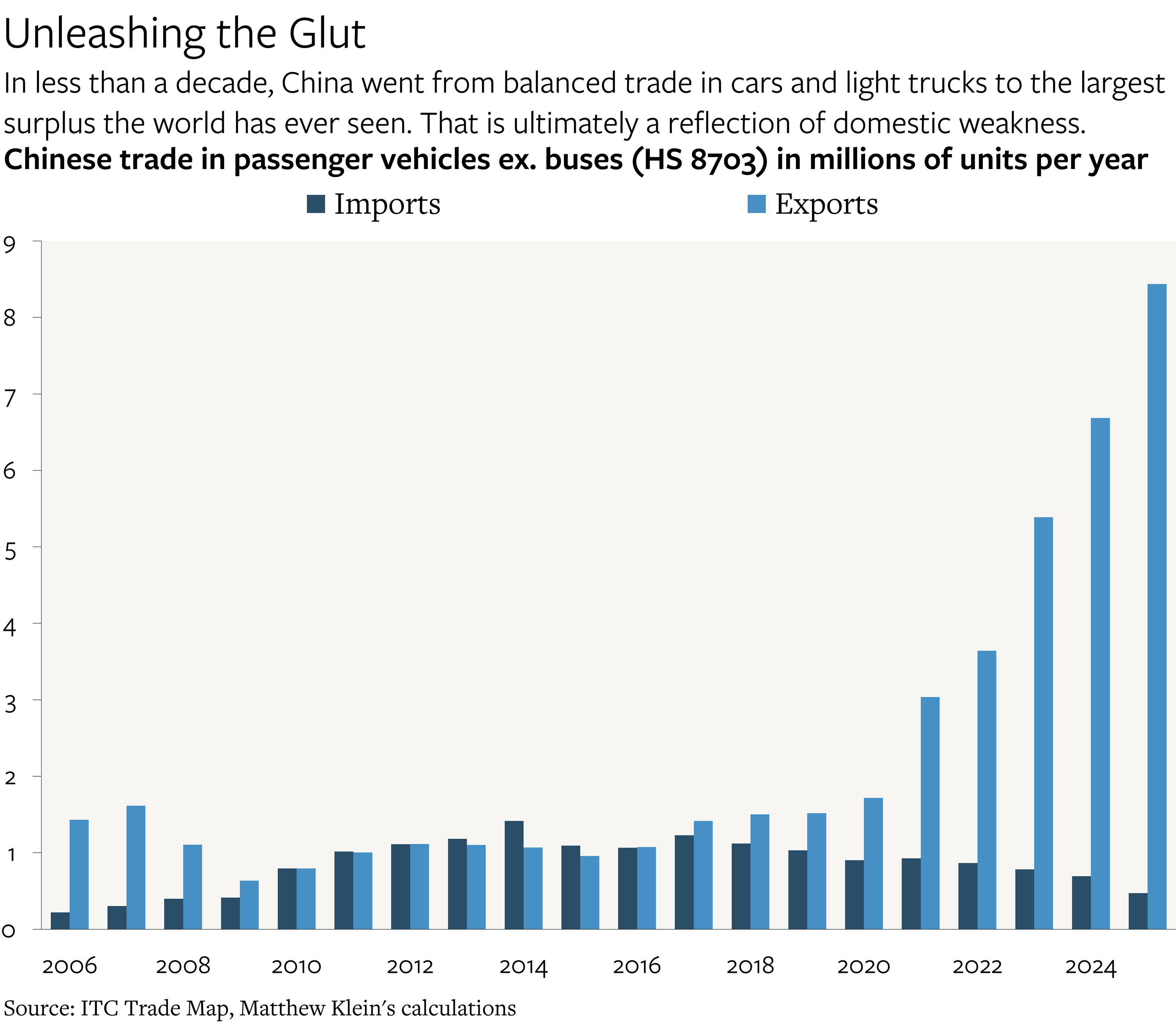

In the first four months of 2026, Chinese import spending on passenger vehicles has collapsed to a run rate of less than $20 billion/year for all countries, of which just $4 billion/year went directly to Germany. Meanwhile, the U.S. dollar value of Chinese exports of finished vehicles has ballooned from $8 billion/year immediately before the pandemic to $90 billion by 2024, to more than $130 billion/year (!) since last summer. In unit terms, China went from both importing and exporting about 1-2 million cars each year in 2011-2019, on average, to exporting more than 8 million vehicles in 2025 while importing fewer than 500,000.

Many analysts therefore attribute the recent re-emergence of China’s overall surplus to Chinese “competitiveness” in motor vehicles and other advanced industries, which, depending on the analyst’s point of view, is either a consequence of Chinese efficiency and innovation, or the product of unfair trade practices and subsidies.

There are elements of truth in these stories, but all of them suffer from the analytic error of “microbrain”: excessive focus on industry-specific phenomena without sufficient attention to the macroeconomic forces that actually drive persistent imbalances.

If Chinese cars, for example, have suddenly become so much better and cheaper than European equivalents that they are raising their market share in Europe, in China, and in many third countries, then Chinese car producers ought to be experiencing soaring revenues that get passed on to workers, investors, and suppliers. That additional income should then flow through to the rest of the Chinese economy as those entities spend their windfall, and some of that spending should eventually flow to the rest of the world via imports because the Chinese economy is not yet completely autarkic. The composition of employment and production in China and in Europe might change over time in response to these relative shifts in productivity, but the overall balance between production and consumption in each economy should not be affected.

Yet this is not what is happening.

Improved “competitiveness” simply cannot explain the rise in China’s economy-wide trade surplus with the rest of the world. Instead, the source of China’s post-pandemic surplus is the same as the source of its previous world-destabilizing surplus in the 2000s: systematic transfers of spending power from ordinary Chinese to businesses, local governments, and foreign consumers.

These transfers depress consumer spending and imports relative to production, investment, and exports. That creates a bias towards trade surpluses—unless businesses and governments spend enough on capital goods, factories, and infrastructure to make up the difference. In the 1990s, they did, but since then, they mostly have not.5

The Chinese government’s response to the pandemic prioritized subsidies to producers and exporters while leaving workers and consumers out in the lurch. The policy choice was a natural consequence of the post-1989 political economy and exacerbated China’s pre-existing imbalances, as some of us warned at the time. The impact was later magnified by the deliberate popping of China’s property bubble, which continues to crush investment spending.

The good news, from this perspective, is that the best way to address (many of) the concerns of China’s trade partners is to raise the living standards of most Chinese people. There is space for genuine “win-win cooperation”, to use a popular phrase, and it does not even require China “winning twice”. The bad news is that this benign positive-sum outcome depends on changes within China that the government may be unwilling—or unable—to make. If Chinese policies do not change, then the rest of the world will have no choice but to take measures to insulate their own societies from the resulting toxic spillovers.