Contra Krugman on Current Account Controversies

The surpluses of Edwardian Britain were not benign and should not be used to justify similar surpluses in Japan, Germany, and elsewhere.

I have learned much from Paul Krugman over the years, and I am extremely grateful for the support he has provided to The Overshoot since it launched in mid-2021. A particular highlight was when he generously cited my research on Russian imports in his New York Times column. So it is with some trepidation that I am going to disagree with some of his recent writings on trade imbalances, particularly regarding Germany and Japan.1

Krugman is right to compare those two societies to Edwardian Britain, but he does not take the comparison far enough. British surpluses back then reflected deep problems within the British economy as well as a dysfunctional global financial system that dumped those problems on large swathes of the rest of the world. The same is true of the large global imbalances that emerged in the 21st century. The flip side is that persistent U.S. trade and current account deficits are not simply the benign consequences of superior productivity performance.

I do not want this note to be too long2, so I will focus on three narrow points:

Edwardian surpluses reflected an unhealthy distribution of income within and across societies.

Contemporary Japan and Germany, for a variety of distinct historical and institutional reasons, suffer from similar sorts of problems, which are then transmitted to the rest of the world through trade and financial flows.

The U.S., along with a few other rich countries with similar institutions, such as Australia, Canada, and the U.K.3, effectively serves as the premier global supplier of safe assets. Foreign savings preferences therefore have the potential to severely distort the U.S. economy absent deliberate policy intervention to limit excessive private indebtedness, currency overvaluation, and deindustrialization.

Edwardian Inequities

This is how Krugman describes the state of global trade and financial flows before 1914 in his article on Japan:

We want and expect capital to flow from places where it earns a low return to places where it earns a higher return. The classic example is Britain in the decades before World War I. Britain was a mature, already industrialized economy that had already accumulated a lot of capital. It made sense for some of that capital to flow abroad to places that needed it.

To a large extent this involved sending capital to “regions of recent settlement.” What people meant by that, of course, was “recent settlement by white people.” Capital flowed to places where Europeans were moving in, often displacing indigenous people: Canada, Australia, Argentina, southern Brazil and, yes, the United States. But morality aside, the economic logic was clear: These places needed capital for their economic expansion, especially but not only to build railroads.

One might think that the richer, slower-growing society of Britain was producing more goods than it needed domestically, exported the surplus to fast-growing settler societies, and financed the sales of those goods by either lending abroad or taking equity stakes in foreign enterprises. Residents of the “mature” economy would have transferred some of their current purchasing power to the “younger” society in exchange for some investment return in the future.

But that is not what actually happened.

The Bank of England compiled estimates of British trade and balance of payments data going back to the early 1800s. It turns out that Britain ran trade deficits in goods every single year starting in 1823. Even after accounting for British trade surpluses in shipping, insurance, banking, and other services, the overall trade balance was negative in the century before WWI. In other words, the “mature” British economy was not providing more real resources to the rest of the world than it was taking in. The transfer of purchasing power went in the “wrong” direction.

What was actually happening was that a relatively small subset of wealthy Brits accumulated financial claims on the rest of the world and then kept reinvesting the dividends and interest payments abroad. By 1913, the value of British residents’ foreign assets minus their (small) obligations to foreigners was worth about 160% of British gross domestic product. Purchasing power was not transferred, but destroyed as income accrued to rich people who did not spend much of it on goods and services at all.

This was appealing—for some. In the movie Mary Poppins, there is a delightful scene that explains how things could work if you started with enough capital. Notice that most of the investment opportunities are either abroad or related to foreign trade, and that the alternative is for Michael to buy food to feed the birds:

But it was not good for most people either in Britain or elsewhere.

In the U.K., British manufacturing suffered from a lack of demand and from lower-priced competition from abroad, creating precarity for workers as well as security risks. Deindustrialization in the face of emerging capacity in the U.S. and, more worryingly, in Germany, was a threat that was exacerbated by the British elite’s focus on training men for military service in the empire instead of industry and commerce.4

Meanwhile, many of the developing countries supposedly benefiting from British financial outflows were in fact running large trade surpluses to generate cash to cover (some of) the interest expense they needed to send to London. The U.S. did well, all things considered, but it was consistently running trade surpluses with the rest of the world starting in the 1870s, and even switched to a large overall current account surplus by 1897. British investors may have been buying U.S. assets and lending to Americans, but the net effect was not obviously helpful to most people in the U.S. or Britain.

In fact, it was the British social critic John A. Hobson who wrote one of the most trenchant analyses of what was wrong with the system as it stood, in his 1902 book on imperialism:

To a larger extent every year Great Britain is becoming a nation living upon tribute from abroad, and the classes who enjoy this tribute have an ever-increasing incentive to employ the public policy, the public purse, and the public force to extend the field of their private investments, and to safeguard and improve their existing investments.

The problem was that the distribution of income within Britain and the other major industrial powers was so malign that it squeezed domestic demand and created the pressure to find export markets:

If a tendency to distribute income or consuming power according to needs were operative, it is evident that consumption would rise with every rise of producing power, for human needs are illimitable, and there could be no excess of saving. But it is quite otherwise in a state of economic society where distribution has no fixed relation to needs, but is determined by other conditions which assign to some people a consuming power vastly in excess of needs or possible uses, while others are destitute of consuming power enough to satisfy even the full demands of physical efficiency…It is not industrial progress that demands the opening up of new markets and areas of investment, but mal-distribution of consuming power which prevents the absorption of commodities and capital within the country.

Interestingly, the one set of places that ran trade deficits in goods with Britain were the ones that were part of its direct and indirect (i.e. mainland China) colonial empire.

Japan (and Germany) Today

Krugman is right to draw an analogy between pre-WWI Britain and Japan. But the conclusions he draws are harder to justify.

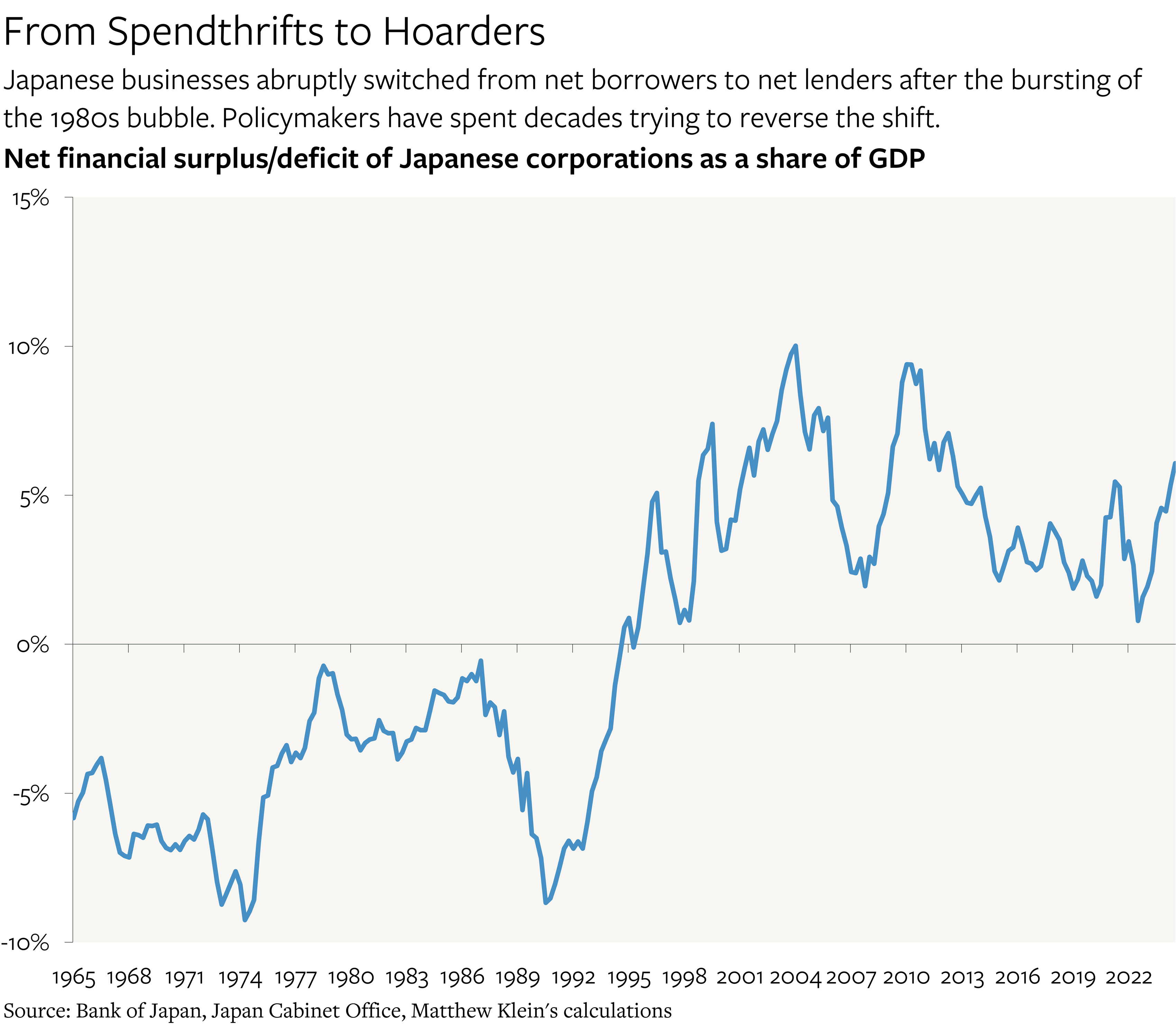

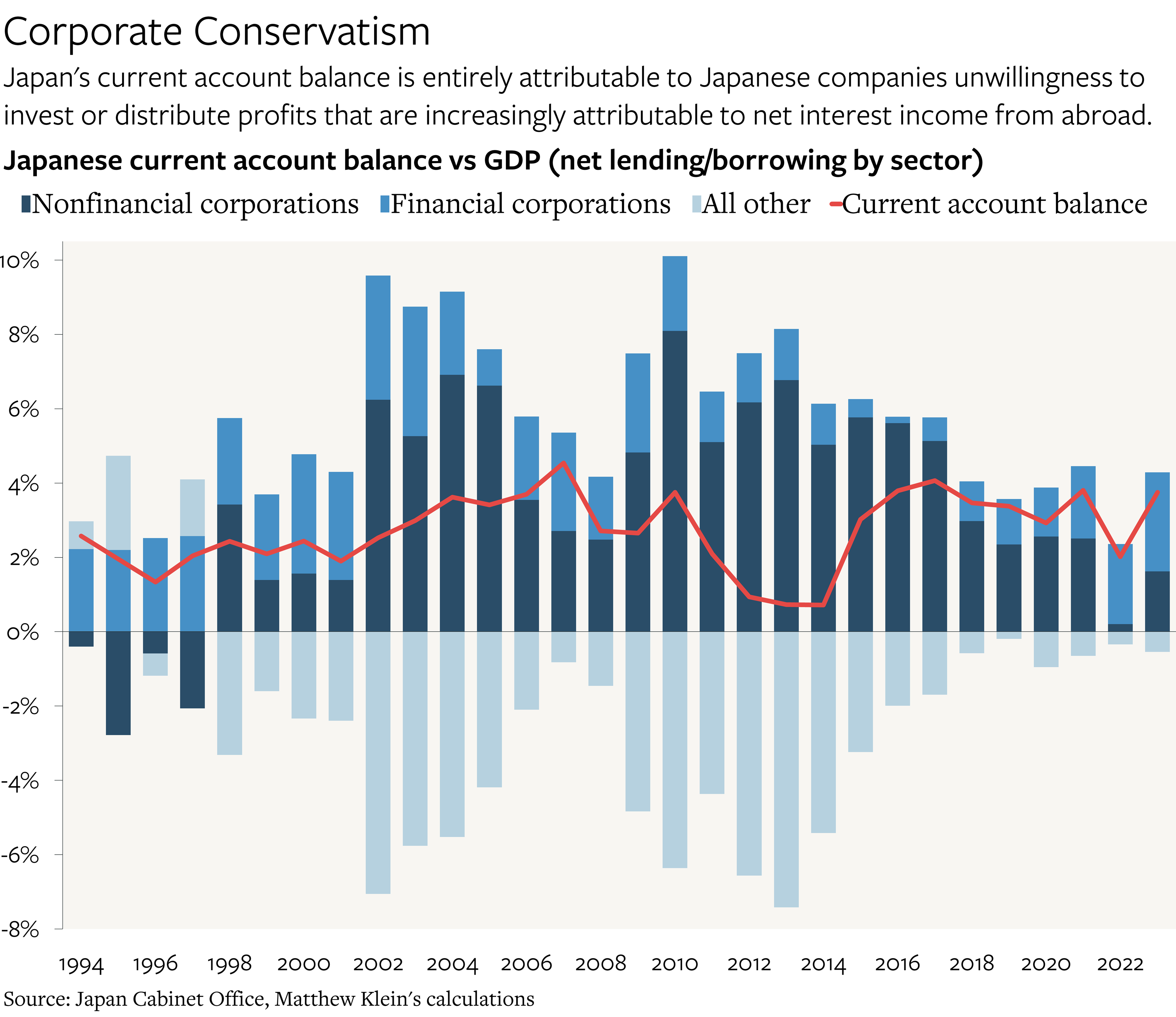

Like Britain, Japan has a large and persistent current account surplus dominated by net investment income. In 2024, the investment income surplus was almost 40% larger than the overall current account surplus, compensating for both the trade deficit in goods and services as well as foreign aid and other transfers.

The takeaway is that Japanese residents, in the aggregate, are not really transferring purchasing power to the rest of the world, despite running a current account surplus. Instead, purchasing power is simply being destroyed.

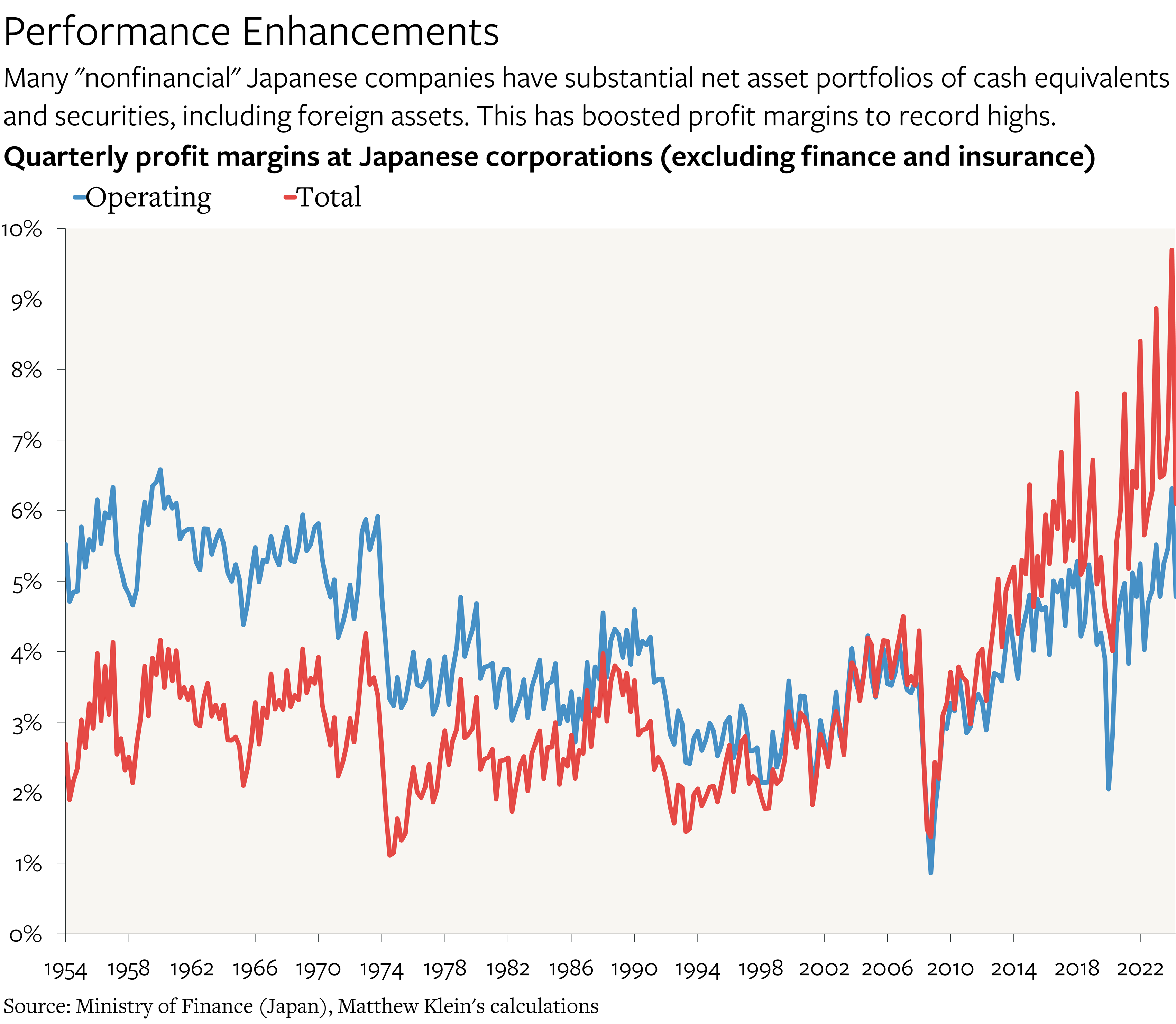

“Japanese residents” is technically correct, but far too broad. The actual explanation is that Japanese companies have steadfastly refused to increase either investment, workers’ wages, or shareholder payouts relative to their profitability—an incredibly long-lasting legacy of the post-1980s bust. Instead, they paid down their debts and then committed to accumulating more and more assets. This is particularly striking given how much of corporate Japan’s net income is now attributable to net interest payments from the rest of the world.

Japanese policymakers have long been aware of these issues. A little over a decade ago I had the chance to meet with senior officials from the Ministry of Finance and other parts of the government, and they explained to me that a major goal of Abenomics was to reverse this trend. Even the 2% inflation target was justified on the grounds that it would tax corporates’ retained earnings cash pile and encourage them to either spend more on capex or increase shareholder payouts.

From this perspective, Abe’s approach failed, even if the currency depreciation helped boost profit margins. I was hopeful that Kishida Fumio might be able to make more progress, because he seemed to understand the relationship between corporate conservatism, consumer spending, and the income distribution. Unfortunately, he does not seem to have pulled it off either. So while it is wrong to claim that Japan is “taking advantage” of the U.S., it is fair to say that the current situation is worse for most Japanese people than it otherwise should be—and that the negative consequences also redound to the rest of the world, including the U.S.

By contrast, Krugman says that “Japan is exactly the kind of country that should be running current account surpluses” because “like late Victorian/Edwardian Britain, it’s a mature economy with limited opportunities for domestic investment, above all because of demography”. Leave aside the fact that Japan’s household savings rate has been stuck around 0% for 25 years, because of aging. There are plenty of unmet investment needs in Japan, from defense to clean energy. Besides, Japanese stocks have done well for a country that supposedly has no good opportunities, either tracking or beating the all-world ex-U.S. index.

A similar error afflicts Krugman’s (much shorter) analysis of Germany:

Germany has somewhat high savings, but mostly it’s lacking in investment opportunities. Their technology has been relatively stagnant. Their demographic situation is not good, very low fertility. And while they’ve had some immigration, it’s not enough to prevent them from having a real problem of labor force growth, which means limited opportunities for investment. And so German money flows abroad.

Germany does not have great demographics, but he is wrong to say that there are insufficient investment opportunities. For one thing, the long and disgraceful track record of German foreign investment is so bad that the hurdle rate for investing domestically is actually quite low.

But as Krugman has noted elsewhere, public investment in Germany has been strangled for decades by mistaken fears of budget deficits and government debt. Germany now has some of the worst infrastructure in Europe, whether it is roads, trains, airports, internet, or energy. On top of which there is now a pressing need to rearm. I had been hopeful that the 2021 election would create the space to break this destructive consensus, and while that turned out to be wrong, I am nevertheless optimistic that the likely winners of the upcoming election will be able to make some headway.

The U.S. Current Account Deficit Is Not About Superior Returns

The last point is that the U.S. does not attract net foreign investment for “good” reasons. Krugman wrote that it made sense that Japan would run a current account surplus and that the U.S. would run a deficit because of differences in demographics. Separately, he gave a presentation where he argued that the U.S. ought to run a deficit because of its superior productivity:

We had a period of rapid productivity growth, and it really starts in 1995 and kind of fades out around 2005…We had a surge in productivity that really wasn’t matched in the rest of the advanced world…That’s exactly when the United States began running big trade deficits. And the reason is that because the US economy was doing well, it was attracting a lot of inflows of foreign investment. And the balance of payments balances. The trade balance plus net inflows of foreign investment equals zero. So if we’re getting a lot of money coming to America to take advantage of the opportunities, we run a big trade deficit. Hard to see how any of this is objectionable or a problem. This is international macroeconomics working the way it's supposed to: Capital flowing to areas that offer high returns to investment, which for a while there was the United States.

While this makes sense in the abstract, it does not fit with the other things we know about what was happening in the world during this period.

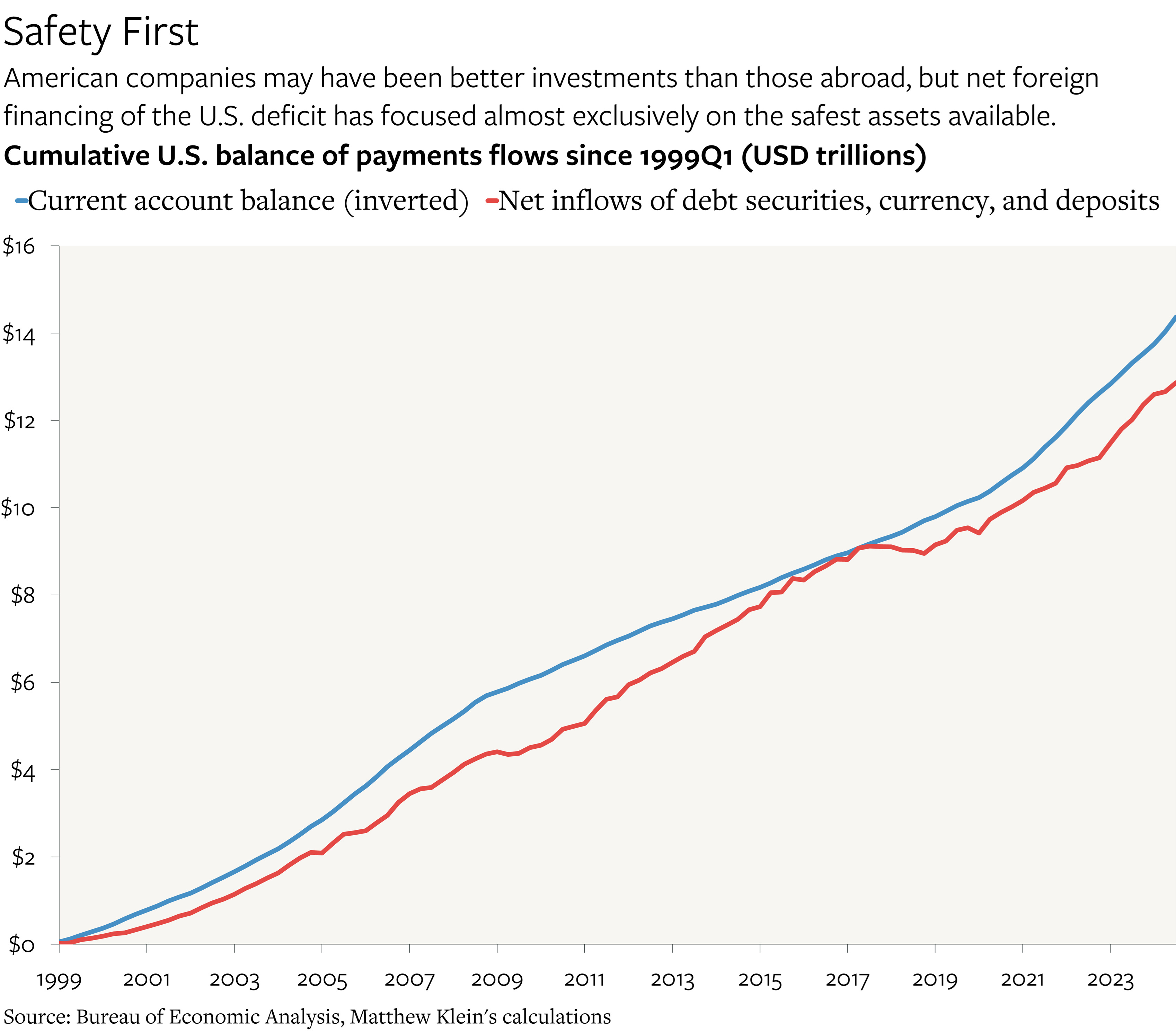

For one thing, the U.S. current account deficit is financed, on net, almost entirely by net foreign purchases of U.S. debt securities—mostly bonds issued or guaranteed by the U.S. Treasury, with the notable exception of toxic mortgage bonds in 2004-7—plus bank deposits and currency.5 In the aggregate, on net, foreigners are not trying to get exposure to high-growth U.S. companies and superior American productivity, but safe claims offering relatively low yields protected by strong legal guarantees.

We also know that severe financial crises afflicted poorer countries in the second half of the 1990s and early 2000s, including but not limited to Argentina, Brazil, Indonesia, Korea, Malaysia, Mexico, Russia, Thailand, and Turkey. Those countries, as well as others that wanted to avoid a similar fate, most notably China, altered their behavior in ways that were individually understandable but globally destructive. In particular, many governments committed to preventing future crises by suppressing domestic demand, generating trade surpluses (mostly with the U.S.), and amassing stockpiles of foreign currency (mostly U.S. dollar) assets. This was not good for them, it was not good for Americans, and it did not reflect the benign consequences of international investors searching the globe for the highest returns.

I have written before what I think the U.S. should do to improve the situation, and I know that there were some in the previous administration who were interested in those ideas. I agree with Krugman that the current administration’s approach is not just unhelpful, but downright harmful. That is no reason to justify trade and financial arrangements that sometimes make things worse for many people.

The same basic arguments could also apply to other countries in Europe and East Asia, most notably Korea and the Netherlands, but I am going to focus on those two, as Krugman did.

Those who want a longer version should of course read Trade Wars Are Class Wars.

I am on the fence about whether to include France, which is substantively different from the others, but nevertheless tends to be the only substantial country in the euro area that sometimes acts as if it is a safe asset issuer.

Digging through some coursebooks I still have from college, I found this passage from Lawrence James’s The Rise and Fall of the British Empire (page 207 of my paperback):

Since the 1840s the public schools had undergone a revolution, started by Dr. Thomas Arnold of Rugby, which transformed the habits of mind of the middle and upper classes…Intelligence mattered less than the acquisition of ‘character’, an intellectual actiivty was largely restricted to otiose and repetitive exercises in the languages of two former imperial powers, Greece and Rome. The end product was a Christian gentleman with a stunted imagination…the late-Victorian public schoolboy shunned trade and industry, even if one had been the occupation of his father. Both activities were consequently starved of talent, which has been seen as one of the causes of the paralysis which was spreading through British manufacturing and commerce during this period.

I would prefer to have the chart start earlier than 1999 but the data before then do not distinguish between foreign purchases of U.S. stocks vs. bonds, counting both as “portfolio investment”.

It would be very interesting to see what your thoughts are on the surplus of different oil exporting countries. For example Norway. How much of a surplus is just the sensible way of handling the cyclical nature of oil prices and how much is repression of domestic demand as China and Germany.

Super illuminating thank you.

If I could ask, in the link to the Kiel working paper you provided about Germany's terrible track record of investing abroad, there is a table showing the US seems to have meanwhile an excellent track record at least between 1975 - 2020. What does this actually mean? Are Americans on average much more astute investors / businessmen abroad? Or is there something else going on? (You don't quite address this in the section about how America's current account deficit is not about superior returns). Thank you.