How Türkiye Pulled It Off (-ish)

Policy tightening helped reduce inflation, stabilize the currency, and improve the country's fragile financial position. But Turks are still worse off than before thanks to rule-of-law concerns.

Türkiye is a country of 90 million people who enjoy, on average, living standards comparable to Poland or Portugal thanks to the integration of their diversified economy into European production networks.

It is also a country with a history of political instability that has spent the past two decades transforming from a democracy that was trying to enter the European Union, into a “competitive authoritarian” regime that maintained democratic forms, into something worse. This has coincided with repeated episodes of financial instability that have been managed, to varying degrees, by the technocrats at the Central Bank of the Republic of Türkiye (CBRT).

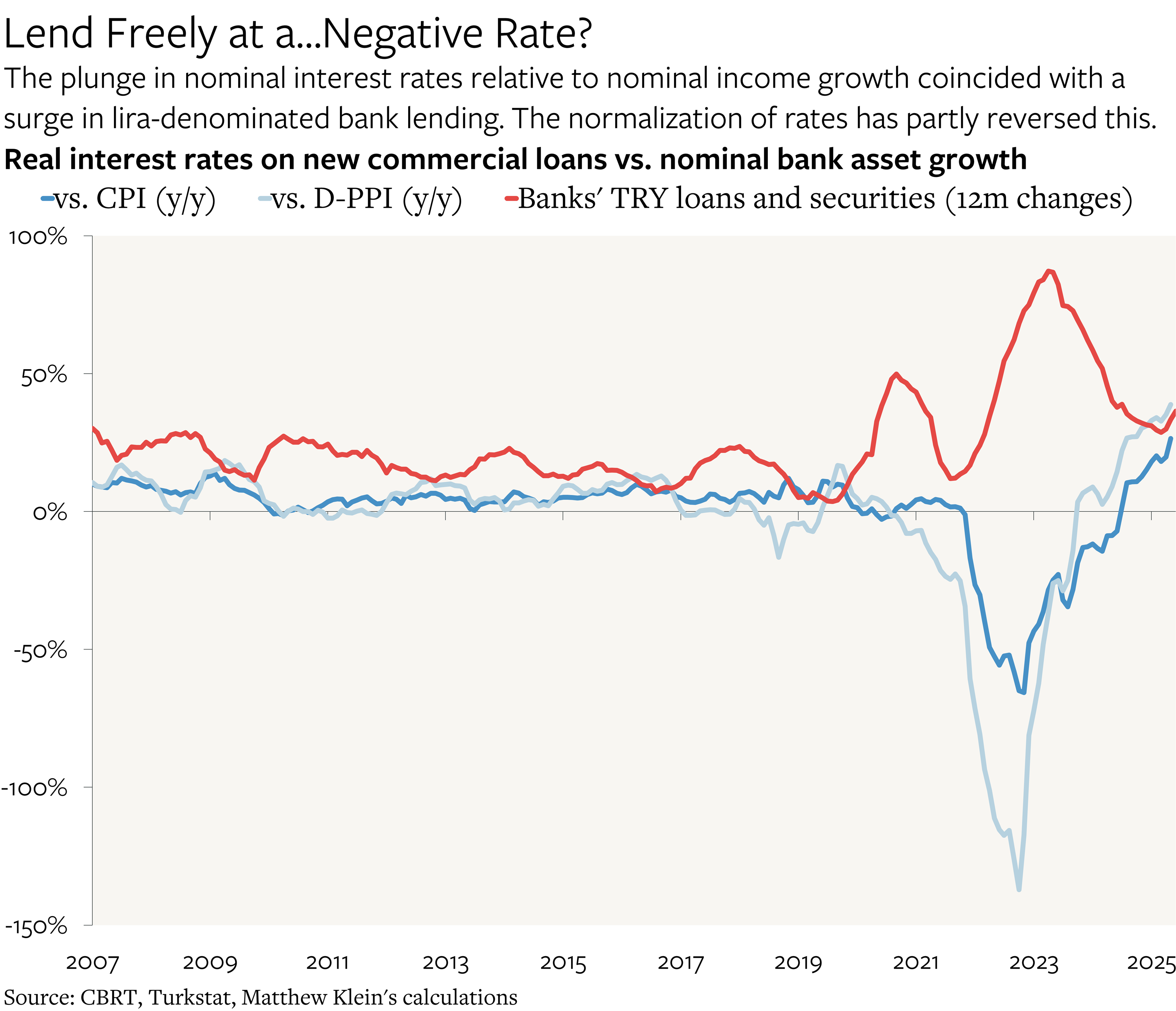

As I had pointed out in the beginning of 2024, the prior commitment to low domestic interest rates meant that the Turkish economy had become increasingly unbalanced, with consumer and business spending increasingly financed by a mix of money printing and foreign currency that was ultimately borrowed by the central bank. (I encourage readers to re-read that note if anything in this note is unclear.) By the beginning of this year, however, it had looked as if the CBRT, together in cooperation with officials in the finance ministry, had made substantial progress unwinding the damage wrought by the policy experiments of prior years.

But just as I was getting ready to write up my analysis of how the return to orthodoxy had (more or less) succeeded in stabilizing the situation, the government decided to arrest the popular mayor of Istanbul—who also happens to be a leader of the opposition to President Erdoğan. That led to a new cycle of capital flight, currency depreciation, and CBRT responses. Now that the acute crisis seems to have ended, and we also have enough data on what actually happened, it is worth looking closely at the dynamics of how it all played out.

A (very brief) history of Erdoğan-omics

President Erdoğan first came into power in elections held shortly after the Turkish financial crisis of the late 1990s/early 2000s, which had culminated with an intervention from the International Monetary Fund in 2001.1 Over the years, his reputation changed from a benign reformer2 to a tyrant. His supposed statement from the 1990s that “democracy is like a streetcar; when I arrive at my stop, I get off” has become increasingly apposite as he repeatedly changed the constitution to arrogate more power to himself and stifled independent media. Even more ominous has been his purging and prosecution of critics, especially in the years following the 2016 coup attempt.

Things had already reached a crisis point by mid-2018. Turks had borrowed hundreds of billions of dollars from abroad, much of it short-term via the banking sector, to finance a domestic construction boom. On top of this, Turkish nonfinancial companies had also borrowed in hard currency in size from domestic banks. This seemed to work well enough as long as the lira did not depreciate too quickly, but it made the economy vulnerable to a retreat in foreign financing that became acute after the coup attempt.

The government’s commitment to low interest rates in the face of accelerating inflation only made things worse. Foreigners started pulling their loans to Turkish banks, with the CBRT trying to make up some of the difference by selling hard currency reserves. By August 2018, the lira had dropped from being worth about 1/3 of one U.S. dollar to being worth about 1/6, while domestic interest rates had jumped from about 16% to 33%.3

One of the likely reasons why the Turkish economy managed to grow in 2020, unlike almost every other country in the world, is because there was so much scope to recover from the prior downturn: real consumer spending had already dropped by 1% from the end of 2017 through 2019Q4, while real gross fixed capital formation was down by 12% over the same period.4 When the pandemic hit, the CBRT cushioned the blow by lowering interest rates, partly offsetting the exchange rate impact by selling about $40 billion in foreign exchange reserves. The currency nevertheless depreciated from 6 lira per USD to 8 lira per USD by the end of 2020.

The post-pandemic inflation hit Türkiye harder than many other societies. From January 2017 through December 2020, the Consumer Price Index (CPI) rose about 14% a year on average, while the Domestic Producer Price Index (D-PPI) rose about 19% a year on average.5 From December 2020 through December 2023, the CPI rose by 54% a year on average, while the D-PPI rose by 72% a year on average. By the end of 2023, it took 30 lira to buy a single U.S. dollar.

Part of the problem was the government’s long-standing insistence on holding lira interest rates low, which in turn was motivated by a mix of heterodox theory and conspiratorial rants about the “interest rate lobby”. While temporary spikes in the prices of select commodities, particularly imported energy commodities, could explain the timing of some of the spikes in broader measures of prices, the main problem was that policy was too loose before the pandemic—and far too loose until the second half of 2023. Tellingly, inflation for groceries tracks inflation for household appliances almost perfectly, suggesting that the exchange rate impact on import prices has been far more important than any external shocks relating to the supply of energy.

Even as inflation was spiking, the weighted average interest rate on new lira-denominated commercial loans stayed around 20%, and it actually fell as low as 14% in early 2023. Unsurprisingly, the volume of banks’ lira-denominated claims on Turkish residents (both loans and securities) rose by 90% between mid-2022 and mid-2023, which happens to be the time when the effective interest rate on new business loans was negative 70%. Turkish nonfinancial businesses rotated away from FX-denominated bank loans into lira-denominated bank loans without changing their aggregate indebtedness.

But while borrowing in lira was obviously attractive during this period, saving in lira was not, which is why Turkish households and businesses moved out of bank deposits denominated in rapidly-depreciating local currency into accounts denominated in dollars, euro, gold, and other hard currencies. At the peak, roughly 70% of bank deposits were either denominated in foreign currency or were “protected” against lira depreciation, compared to 30% as recently as 2011. The rise of lira interest rates has since reversed all of these trends, encouraging savers to rotate back into lira-denominated deposits.