The U.S. Economy Is Booming. Or Stagnating? The Mystery of the Missing Interest.

The latest estimates of domestic income and domestic product are alarmingly inconsistent. The gap is mostly attributable to the bizarre (alleged) decline in net interest paid by businesses.

The U.S. economy has grown at a yearly average rate of 2.2% over the past two years—and by 3% in the past 12 months. Or, it has grown at a yearly rate of just 0.7% since 2021Q3, having shrunk by 0.8% since 2022Q3.

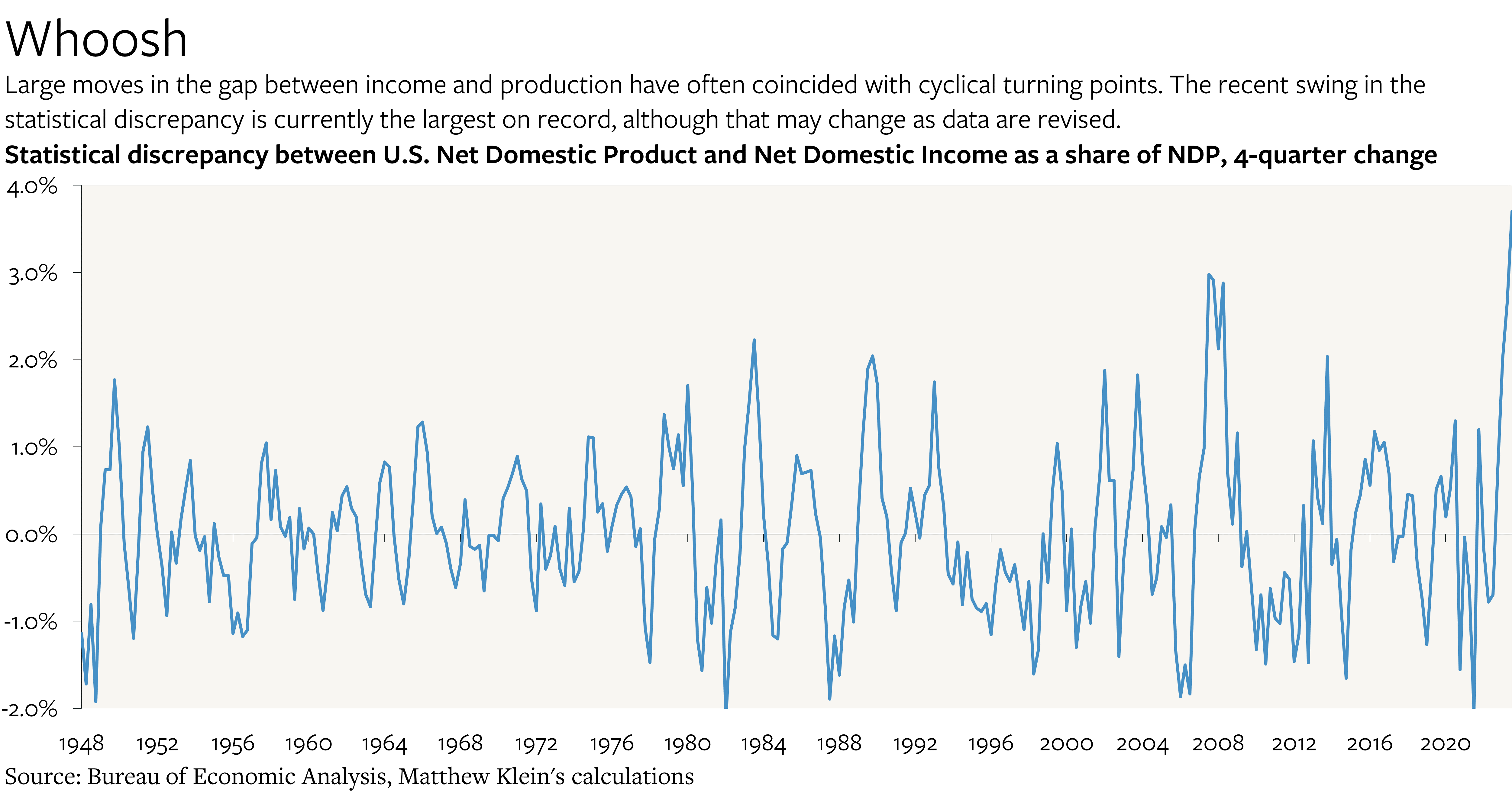

That is a big difference. Put another way, the “statistical discrepancy” between expenditure-based estimates of the value of goods and services produced in the U.S. (GDP/NDP) and estimates of the income generated in the U.S. (GDI/NDI) has swung by a whopping $843 billion (annualized) between 2022Q3 and 2023Q3. Production net of depreciation (NDP) is currently estimated to be 3% larger than net income (NDI). Last summer, NDP was thought to be 1% smaller than NDI. Subsequent revisions should change the picture, but as of now, this is the largest 4-quarter move on record.

While there are several plausible explanations, it seems likely that something strange is going on with the way the Bureau of Economic Analysis (BEA) estimates the amount of interest paid and received by businesses.

But first, some context.

The Statistical Discrepancy in 2021-2022

Regular readers know that this is not a new problem. Estimates of NDI exceeded NDP by as much as 5% last year. That confused me a great deal, and inspired a fair amount of digging. The BEA eventually cleared things up with its September 2022 benchmark revisions, although the September 2023 comprehensive revisions added some new wrinkles:

U.S “Excess” Household Savings and the Balance of Payments (January 25, 2022)

Are the U.S. GDP data missing a capital spending boom? (February 16, 2022)

U.S. Economic Data Aren’t Adding Up (May 27, 2022)

Solving One Puzzle in U.S. GDP Data (Maybe), Finding More (August 31, 2022)

The Covid Recovery Looks Different Now (September 30, 2022)

Less Tax Evasion, a Profit Boom, and a Persistent Interest Puzzle: Highlights of the 2023 Comprehensive NIPA Revisions (Part 1) (September 29, 2023)

At the time, I thought this puzzle could potentially be explained by the misclassification of certain forms of investment spending as intermediate consumption. Companies buying parts to build their own servers in-house, for example, might expense their purchases instead of treating them as capital spending, and that accounting treatment might then flow through to the BEA’s estimates of spending on “material inputs”, which are netted out from estimates of domestic production.

My thinking was based on the BEA’s convention of attributing the statistical discrepancy to “domestic private business”, as well as the BEA’s own research showing that corporate profits, proprietors’ income (small business and self-employment income), and capex are the components of GDP/GDI most prone to revision.

As of now, the official explanation is a bit different (see my notes from September 2022 and September 2023 for more details). First, wage income in 2021-2022—which should be among the more straightforward components to track—was revised down. Second, consumer spending, particularly on pandemic-affected services, was revised up. Third, services exports were revised up. And finally, both the dividend payout ratio and profit estimates were revised up a lot. But none of those changes explains the gap that has emerged recently.

Decomposing the Income Shortfall

The cumulative changes in nominal NDP and NDI from the end of 2019 through the beginning of 2023 were almost identical. The recent discrepancy is a function of the fact that NDP has continued to rise this year, while NDI has barely grown.

There is no theoretical reason to prefer NDP over NDI as the “right” measure of what is happening in the economy, or NDI over NDP. But the sources of the recent gap seem to be concentrated in components of NDI that are more prone to measurement errors and revisions.