The U.S. Job Market is (Still) Inflationary

Wage growth is now accelerating slightly, supporting the quickening of "supercore" service price increases. Plus: more on the health care wage slowdown mystery.

I was fortunate to attend two fascinating conferences in the Bay Area last week, which I look forward to writing about soon.

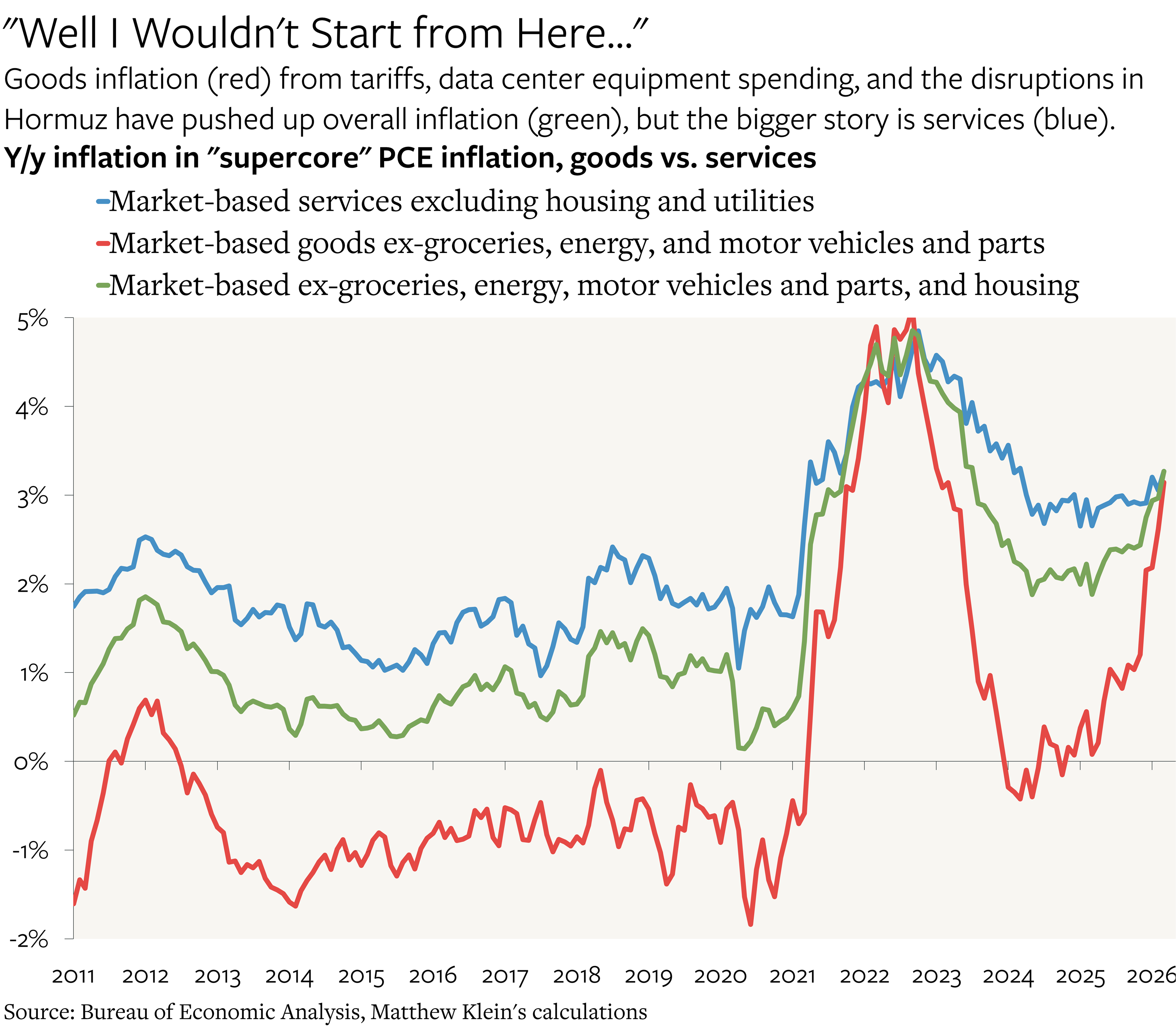

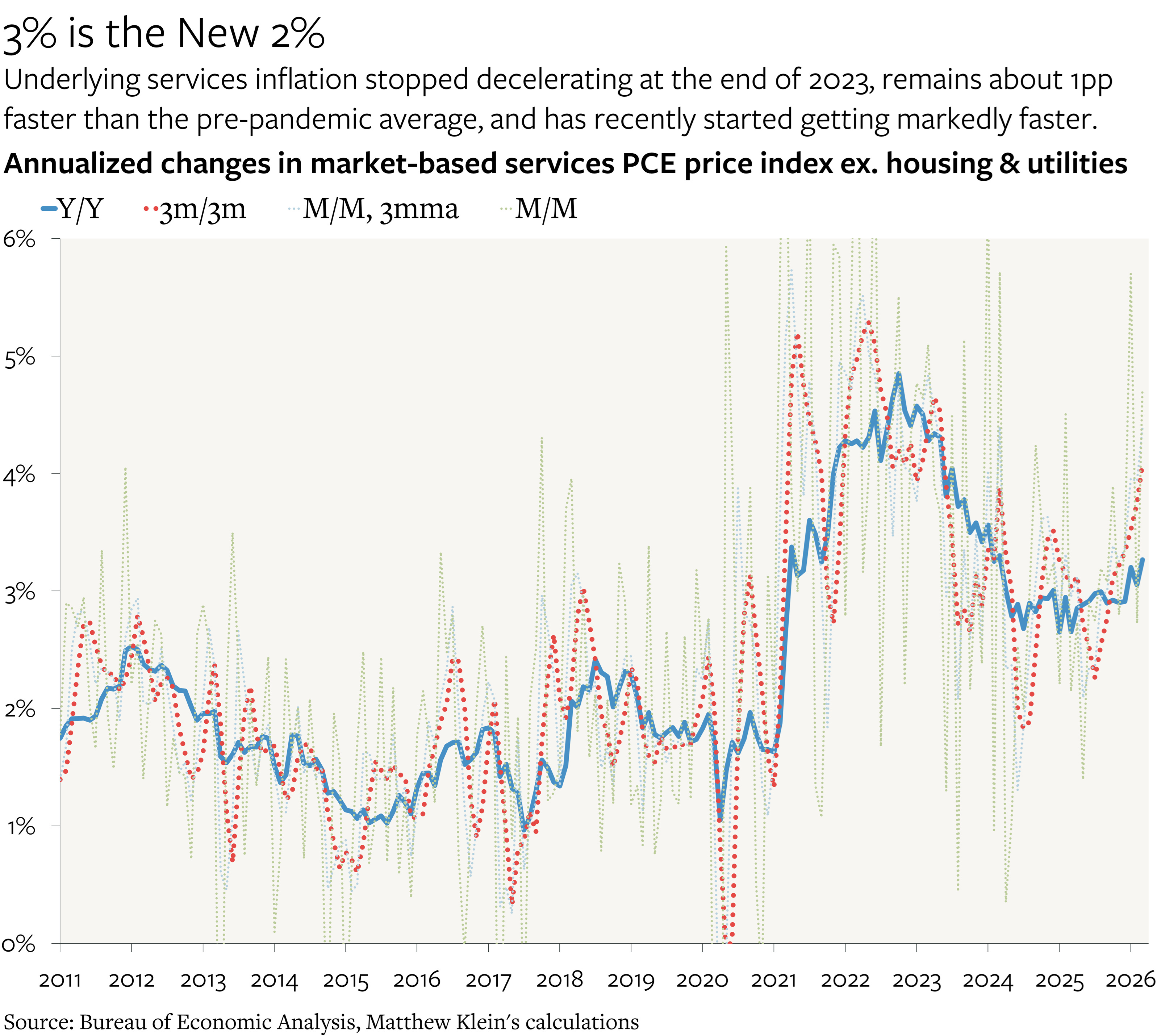

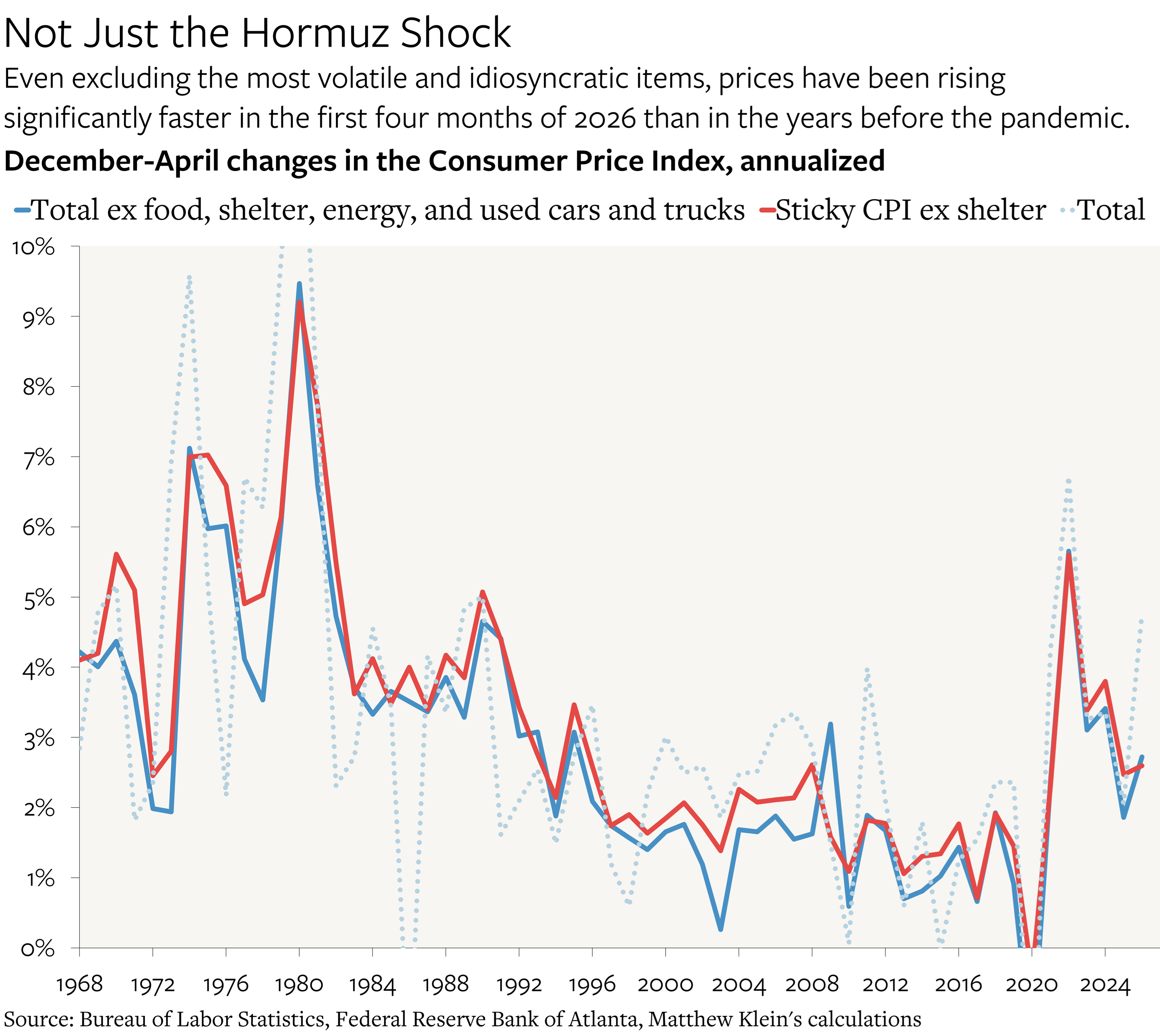

Tariffs, cloud companies’ insatiable demand for (imported) data center equipment, and the disruption to the flow of goods through the Strait of Hormuz rightly get a lot of attention. But the most important thing to understand about U.S. inflation is that the prices of locally-produced services continue to rise about 1-1.5 percentage points faster than in the years immediately preceding the pandemic—and the pace has been accelerating over the past year. Even without the unwelcome “one-time things” pushing up prices, underlying inflation would still be just as far off from the Federal Reserve’s goals as it was three years ago.

The most straightforward explanation is that U.S. consumers’ (nominal) purchasing power continues to rise quickly enough to cover both rising real demand as well as any price increases that businesses try to pass along. Despite Federal Reserve officials’ repeated insistence that they are committed to bringing inflation back to just 2% a year, there seems to have been a regime shift in the growth rates of (nominal) incomes and prices compared to the period before the pandemic. In particular, most measures of the average worker’s pay are still rising markedly faster than in the period immediately preceding the pandemic.1 While that does not have to correspond to faster inflation, it usually does.2

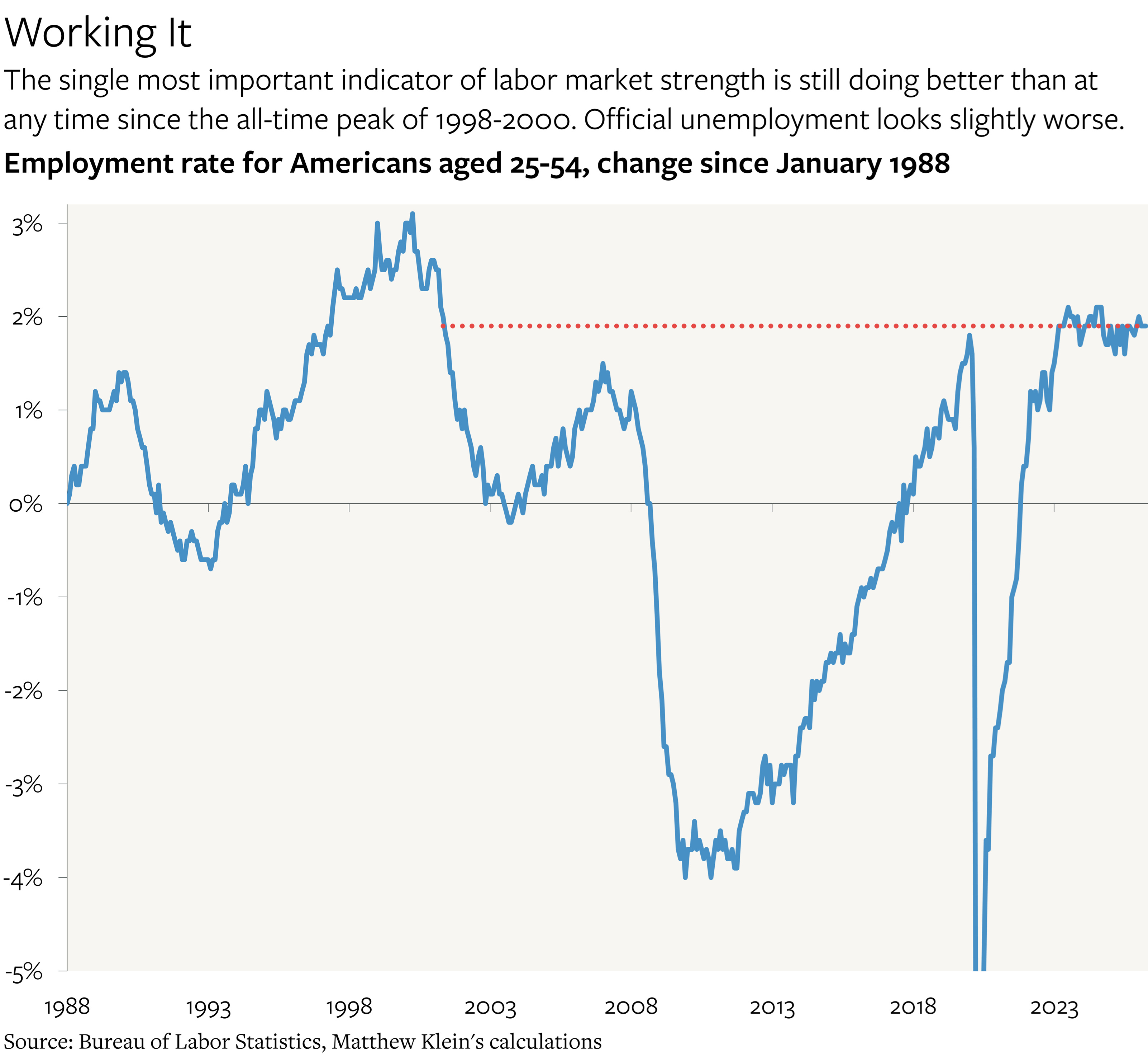

This post-pandemic nominal growth regime has been sustained, in part, by the continued strength of the U.S. job market, which Fed officials have (justifiably) been unwilling to force into a downturn.

Just as the dramatic headlines about goods-related inflation have obscured the more important story about services prices, the wild swings in net payroll growth over the past two years, which have largely been attributable to changes in immigration policy rather than changes in cyclical conditions, have obscured the more important stability in the proportion of Americans aged 25-54 with a job.

This is not a bad thing: the slow nominal growth and low interest rates of the 2010s were both symptoms and causes of an unhealthy economy. I see no reason to prefer yearly inflation of 1.5-2% vs. 3% if the only way to get the slightly slower inflation rate is via persistent underemployment and precarious household finances. But regardless of what I or anyone else prefers, this is where the U.S. economy is right now.3 That should have implications for interest rates, among other things.

The rest of this note goes into more detail on the latest data for wages (including the bizarre health care numbers I flagged last month) and prices.