This is What Normalization Looks Like (Mostly)

Long-end interest rates are rising after a prolonged period of being unusually low relative to short-end rates. Even the moves in Japan look less scary when viewed in light of the fundamentals.

I recently joined Anjon Roy’s Paradigm Shock podcast to talk about Trade Wars Are Class Wars and the implications for today. Hope you have a listen!

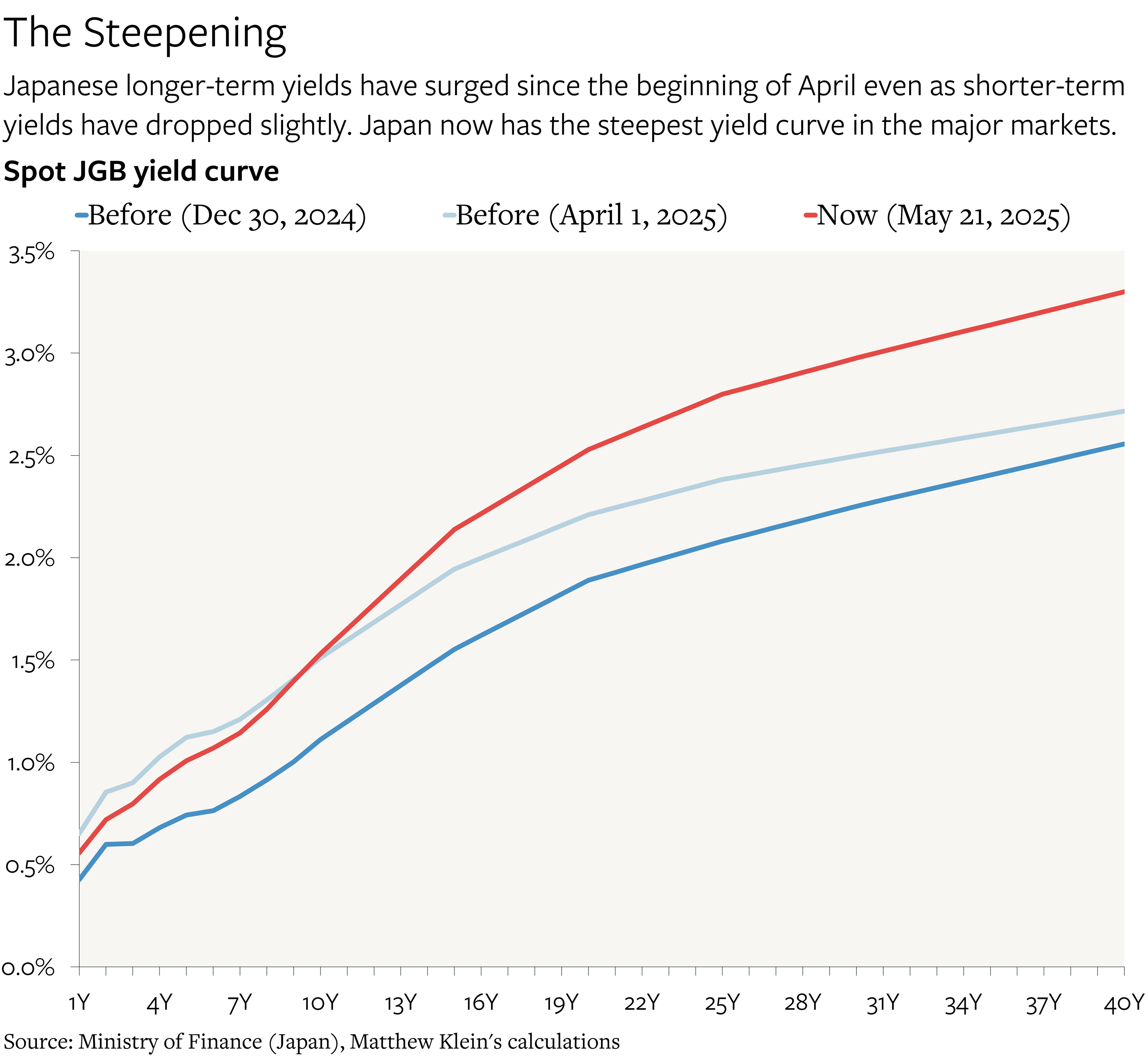

It is getting more expensive for governments to lock in fixed interest rates on longer-term debts. The price action has been particularly extreme in Japanese Government Bonds (JGBs), where ultra-long-term yields been going vertical thanks to surging far-forward interest rates.

Hedged into U.S. dollars, the 30-year JGB is now yielding about 7%, but some off-the-run issues are trading much higher.1 Unsurprisingly, the most recent survey conducted by the Bank of Japan (BOJ) found that “bond market functioning” as of early May had collapsed relative to early February. The only worse drops were in the period leading up to the BOJ’s adjustment of Yield Curve Control at the end of 2022, the depths of the pandemic, and the introduction of yield curve control in 2016.

But while the recent moves have been chaotic, they are not entirely unjustified given the changes in Japanese economic fundamentals over the past few years.

After decades of trying to generate nominal income growth, Japanese policymakers seem to have finally succeeded in the years following the pandemic. In 2016-2019, the value of the income generated in Japan rose by only 0.2% a year in yen terms, on average. But NGDP grew by 4.4% a year, on average, from 2022Q4 (after energy prices had peaked) through 2025Q1. Over the past four quarters, NGDP rose by 5%. Japanese consumer prices have gone from not rising at all in the years before the pandemic to rising about 3.5% as of April 2025. Exclude the unprecedented surge in rice prices2, which have doubled over the past 12 months, and underlying inflation measures seem to be settling around 1.5-2% year, compared to ~0% before the pandemic.

This also seems to be flowing through to wages, with the latest negotiated pay increases between employers and the Japanese Trade Union Confederation (Rengo) clocking in at 5.4%, with about 4 percentage points of that attributable to higher base salaries. That is the second year in a row that negotiated pay increases have topped 5%, which is the most since 1991. Negotiated pay increases were around 2% a year in the decades before the pandemic, with base salaries flat. While overall Japanese wage growth has historically been weaker than what Rengo has secured for its members, the acceleration in negotiated pay increases over the past few years seems to have flowed through to faster aggregate wage gains, as can be seen in this chart from a recent speech by BOJ board member Noguchi Asahi.

BOJ officials have been burned before, but they have become increasingly optimistic that they are getting close to achieving their longstanding goals. That is why, since March 2024, they lifted their cap on the 10-year JGB yield, began reducing their net asset purchases, and, most recently, started raising short-term interest rates. Should the BOJ succeed, it would make no sense for ultra-long bonds to yield less than 1.5%.

In March 2025, BOJ officials were aware of potential problems. From the minutes:

They agreed that, in principle, long-term interest rates were to be formed freely in the markets in response to factors such as market views of economic activity and prices. On this basis, a few members noted that, in an exceptional situation where long-term interest rates rose in a manner that differed from normal market developments, from the perspective of encouraging the stable formation of interest rates in the markets, the Bank would nimbly conduct operations. These members then commented that, although the markets did not appear to be in such a situation at this point, it was necessary to carefully monitor market developments.

On May 13, the BOJ included the following cryptic statement in their summary of the meeting ended May 1:

Investors need to be cautious about investing in super-long-term JGBs when market expectations regarding the interest rates on these bonds are particularly high and the markets are nervous. While it is natural for central banks to take appropriate account of market views, if a central bank is continually over-flexible in response to these views, this flexibility itself could make the bank's responses less predictable, thereby increasing uncertainties in the markets. The Bank should avoid, as much as possible, actions that lead to such uncertainties.

The challenge for bondholders—and for policymakers—is managing the transition between the old world of slower growth and lower yields and the new world of faster growth and correspondingly higher yields. Someone who had bought a new 40-year JGB in April 2024, when the yield was 2%, is now sitting on an unrealized loss of more than 30%.3

As it happens, the rest of the rich world has some recent experience with this. The exit from the pandemic led to a reset in growth rates that has been disorienting for people who were convinced that the lost decade of the 2010s was “normal”. While interest rates are still adjusting, occasionally in ways that look a little chaotic, the bigger picture (so far, anyway) is that yields are getting closer to what one would expect given historical relationships with fundamentals and historical term spreads. There is no need, yet, to come up with scare stories about excessive bond supply due to “fiscal profligacy” to understand what is happening.4 Especially since fiscal profligacy is not even happening in the U.S.

The U.S. Austerity Budget

The U.S. Congress is moving forward with a budget plan that would not lower most Americans’ taxes relative to current rates5, but that would meaningfully cut spending on health benefits for the poor (Medicaid), food aid for the poor (SNAP), and subsidies for green energy. The proposed budget is also set to sharply increase the punitive tax imposed on America’s premier research universities in 2017. Combined with the tariffs, which are taxes imposed on Americans, the net effect should be contractionary relative to the current fiscal stance, although the timing of specific provisions may obscure the aggregate impact.

Confusingly, much of the coverage about the proposed budget focuses on how much the federal deficit will rise over the next ten years compared to “current law” and what that will do to the stock of federal debt outstanding. Most estimates of the total “cost” of the proposed legislation start from the absurd baseline that individual and business taxes would have been allowed to rise sharply in 2026 as the 2017 Tax Cuts and Jobs Act (TCJA) expired. That was never particularly likely, especially once the party that explicitly campaigned on extending the TCJA tax regime won Congressional majorities and the presidency.

The main surprise, to the extent that there was one, was the severity of the spending cuts, although some of them may be moderated by the Senate. In fact, according to the nonpartisan Committee for a Responsible Federal Budget (CRFB), the current budget plan adds far less to the debt stock relative to the “current law” baseline over the next ten years than they had expected based on pre-election campaign promises. The CRFB’s “central” projection as of the end of October 2024 was that the Harris agenda would generate additional borrowing of $4 trillion in 2026-2035 relative to “current law” and that the Trump agenda would generate $7.8 trillion in extra debt. Their current estimate of the bill just passed is that it would add only $3.1 trillion in incremental debt. Add in reasonable estimates of the revenue impact of tariffs and it is possible that the new budget could lead to almost no incremental increase in federal debt issuance compared to the “current law” baseline!

There are plenty of reasons to oppose this policy mix, but concerns about the deficit impact (relative to doing nothing) are not particularly compelling. Nevertheless, U.S. bond yields have gone up in a way that is causing some analysts to panic. That suggests there are other forces at work.