The Europeans Should Give Russia's Reserves to Ukraine Now

An accounting gimmick that is appropriate for the seriousness and stupidity of the times.

Democratic Europe can become a formidable military power capable of subduing the Russians and securing peace on the continent. Unfortunately, that will take time, but there is plenty that the Europeans (and Japanese) can do right now to increase their support of Ukraine in the face of American perfidy. In particular, they can immediately give the Ukrainians hundreds of billions of dollars of purchasing power by transferring ownership of Russia’s frozen foreign exchange reserves, much of which are trapped inside a handful of European jurisdictions.

What Foreign Reserves Are

Finance is a technology to transfer purchasing power through space and time. I can choose to buy fewer goods and services today in exchange for the ability to buy more tomorrow as long as there are others who are willing to buy more now in exchange for creating financial liabilities that will constrain how much they can buy in the future.

Governments regularly borrow, both to finance investments and to cover temporary revenue shortfalls/spending spikes associated with business cycle downturns, pandemics, wars, or other emergencies. Governments also save. Some governments accumulate strategic stockpiles of everything from maple syrup to crude oil.1 The current U.S. administration is apparently thinking of using taxpayer resources to bid up the prices of various cryptos. And many states, particularly those that have experienced balance of payments crises, hold foreign currency reserves to help cover spending on imports and debt service in case of emergency.

All reserves are a form of insurance, and the premium payments take the form of higher taxes and lower public spending than otherwise would have been the case. Accumulating reserves of critical goods can make sense for societies that want to limit price volatility, or are worried about supply vulnerabilities. Societies reliant on commodity exports may want to hoard hard currency when prices are high to lock in some of the benefits and hedge against future downturns.

But those hard currency reserve assets have to be issued by someone. The flip side of FX reserve accumulation is that a few governments are borrowing more than would otherwise be the case, or at least borrowing more cheaply, at the cost of a relatively overpriced currency and slower growth. Net asset purchases somewhere must be matched by net liability creation somewhere else, and the places where reserve managers want to lend are not necessarily the societies that actually need the money.

In the aggregate, people in the reserve-buying societies are living below their means in exchange for the promise of a floor on future living standards, while people in the reserve-issuing societies are spending more than they produce (often by producing less than they could) and racking up ever-increasing debts, which could—but probably will not2—be exchanged for claims on future production. This is a worse outcome for almost everyone involved compared to a world where countries did not need to self-insure.

Besides which, building a financial war chest to prepare for emergencies does not even work much of the time, because the best hedges are real investments in spare productive capacity and stockpiles of critical goods. This was as true for the Russians—who ended up leaving much of their reserve hoard under the control of the democracies—as it was for the Germans who were unreasonably pleased with their low levels of public debt even as they let their infrastructure and defense capabilities deteriorate.

Russia’s Foreign Reserves

Russians endured an extremely painful balance of payments crisis in 1998. Determined never to repeat the experience, the Central Bank of Russia (CBR) spent almost $500 billion accumulating foreign reserves when oil prices soared in 2003-2008. Some of that stockpile was subsequently spent down to support Russian purchasing power and debt service obligations in response to the global financial crisis, and again in 2014-2016 after Russia was hit by the combination of mild sanctions and severe declines in energy prices. But reserves were rebuilt in 2017-2021 and were worth $630 billion on the eve of the Russian invasion of Ukraine just over three years ago.

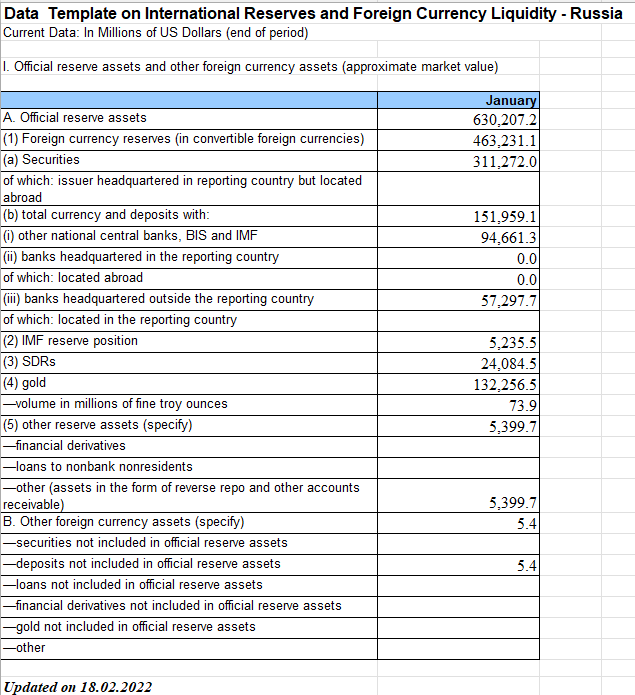

Back then, the CBR held $463 billion in convertible foreign currency assets. Of that, $311 billion was held in securities and $152 billion in foreign currency deposits, of which $95 billion was with foreign central banks and institutions such as the Bank for International Settlements (BIS), and another $57 billion in other banks outside Russia. Beyond convertible FX assets, the CBR also held $29 billion with the International Monetary Fund and 73.9 million troy ounces of gold, which was then valued at $132 billion. The CBR has since taken down the spreadsheet that provided this detailed breakdown, but I had saved it at the time. This is what things looked like then:

The CBR also published more details on its holdings in its annual report for the end of 2021. (The amounts do not line up exactly because the dates are not identical.) By type, debt securities issued and guaranteed by sovereigns and international organizations accounted for about 42% of total reserves, while deposits at foreign banks, foreign central banks, and the BIS accounted for 30%. Gold held in the CBR’s vaults covered most of the rest.

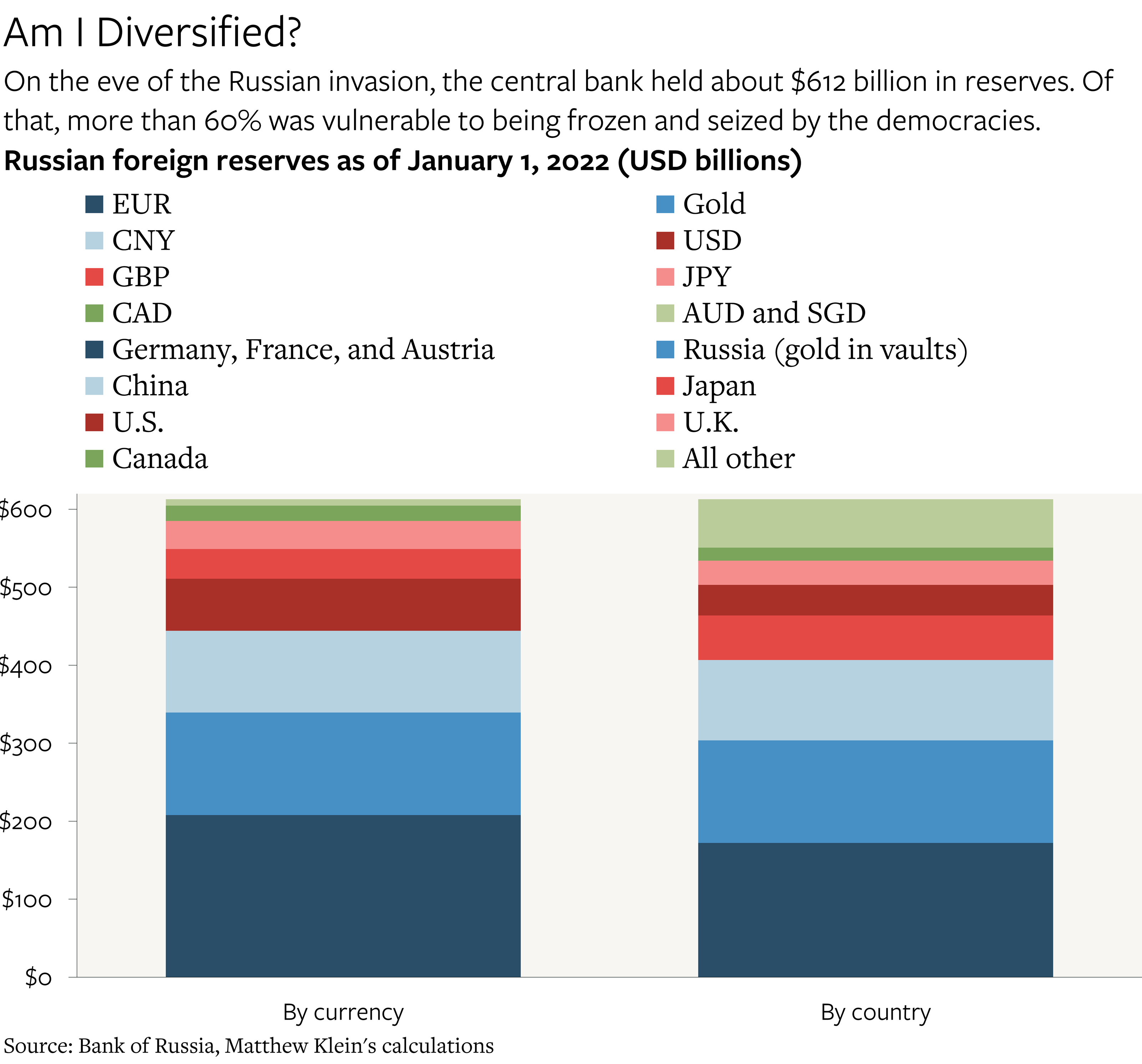

By market value, about a third of Russia’s reserves were held in euro, 17% in Chinese yuan, 11% in USD, 6% each in GBP and JPY, 3% in CAD, 1% in AUD, and the remaining 21.5% was in gold held in vaults in Russia. The currency exposures did not perfectly match the country exposures, with about half of the USD-denominated holdings issued by non-U.S. borrowers, about a third of the Japan exposure was in currency other than JPY, and some of the GBP exposure was in non-U.K. assets.

Some of those mismatches likely reflected holdings of Special Drawing Rights (SDRs) in addition to custody relationships and purchases of offshore debts (i.e. Japanese corporate debts denominated in USD). Regardless, a little more than 60% of Russia’s foreign reserve portfolio was theoretically vulnerable to being frozen. That was much lower than before the first Russian attack on Ukraine in 2014, but still relatively high for a country planning on becoming an international pariah.3

The CBR has since become much less transparent, only indicating that there are $386 billion in convertible FX assets, $28 billion in claims on the IMF/SDRs, and 74.9 million troy ounces of gold, currently valued at around $207 billion. A big chunk of the “convertible” assets are not really convertible, however, because the CBR’s accounts were blocked by the allies almost immediately, as I (and Mario Draghi) had recommended over Janet Yellen’s objections. As the CBR put it in their 2022 annual report (emphasis mine):

Modern banking systems and systems for record-keeping of rights to securities are designed so that authorities and financial institutions of each country, normally, can identify the ultimate owner of assets denominated in the currency of this country and, if they decide to do so, can block these assets or the assets of the financial institution where the ultimate owner has the account…At the end of February 2022, a number of foreign countries forbade their residents to conduct any transactions with the Bank of Russia and its assets. The sanctions limited the opportunities to use and manage a part (about 50%) of Russia’s international reserves, but the Bank of Russia remains the owner of the blocked assets. The Bank of Russia is preparing legal claims to challenge this blocking of its assets.

And in their most recent annual report, the CBR reiterated why they were in that position despite having done so much to move into gold and yuan pre-2022:

The opportunities to further diversify the reserve assets with currencies and financial instruments of countries not put on the list of unfriendly states are limited due to the risks that these currencies and economies might involve. The exchange rates of these currencies are highly volatile, the markets are characterised by low liquidity, and a number of such countries have capital controls, which is why such currencies and instruments cannot be used to form reserves.

There are no publicly-available data on where exactly Russia’s blocked reserves are right now, although my friend and former colleague Martin Sandbu has done heroic work on this over the years. We can reasonably guess that some portion of the European Central Bank’s (ECB) “liabilities to non-euro area residents denominated in euro” and some portion of “other deposits” held at the Bank of Japan consist of CBR assets. Perhaps most significantly, we know that €183 billion worth of coupon and principal payments from bonds held by the CBR at Euroclear, the Brussels-based custodian, have ended up at Euroclear Bank, which means that Russia’s total holdings at Euroclear are somewhat more than that.4

Why Now is the Time to Confiscate the Reserves

While I was among the first to publicly call for seizing Russia’s foreign reserves, it is not something I have written much about in the years since. I had two reasons:

Limiting Russia’s access to its reserves was not hurting its ability to wage war given the other measures that were already in place. The point of reserves is to be able to spend more on imports (and debt service) than would be expected given export earnings, but the Russians have consistently been spending far less on imports than one would expect. In 2024, Russia generated a current account surplus worth $54 billion. That is presumably because sanctions and export controls have been constraining what is available to buy. Blocking access to Russia’s reserves was reasonable as part of a belt-and-suspenders approach to financial warfare, but seizing the reserves did not seem like an urgent priority compared to tightening the export controls and giving more actual firepower to the Ukrainians.

The allies did not need to seize the reserves to provide support to Ukraine. The allies have enormous financial resources at their collective disposal. At current exchange rates, the most expansive estimate of total Russian spending on the war since the beginning of 2022 is about $500 billion. That is just 0.8% of the value of goods and services produced in the rich democracies in 2024 alone. Tiny Norway has a sovereign wealth fund worth more than $1.8 trillion dollars. Even if the allies wanted to outspend the Russians and cover the entire bill for Ukrainian reconstruction, which the World Bank currently estimates is $525 billion, the total cost would still be trivial.

Put another way, my issue was that some people were confusing the financial with the real. The actual cost of aiding Ukraine, to the extent that there is any cost when viewed against the costs of not supporting Ukraine, is that some amount of goods stored in, produced in, or imported into the democracies would go to Ukraine rather than the domestic market.5 That cost would stay the same regardless of how the aid is financed.

From this perspective, seizing the $300+ billion in Russian reserves to defray the aid bill would be an unnecessary accounting gimmick. On paper, seizing the reserves would hurt Russia and help Ukraine, but the battlefield effect would depend on how it would affect the Russians’ and Ukrainians’ ability to get what they needed to wage war. Until recently, for the reasons noted above, it seemed that the real effect would be close to zero. Given the supposed legal issues associated with seizing the reserves outright as opposed to indefinitely blocking them6, it did not seem like an argument worth having.

But things have changed materially in the past few days.

The U.S. has cut off military aid to Ukraine and might plausibly weaken the sanctions on Russia to the point that the reserves might become useful again. Given the current state of things, it is even possible that the current U.S. administration would pressure the allies to drop their own sanctions, including the blockages of the CBR’s accounts in Euroclear, Japan, and elsewhere.

The allies have limited options in the face of this perfidiousness, but they do have one big option: seizing Russia’s reserves now and giving them to the Ukrainians, who can use the money to buy military gear and other needed goods on the open market.7 It is an accounting gimmick, but an accounting gimmick is an appropriate response to the seriousness and stupidity of the times.

As of this writing, the Europeans are moving in this direction, although the proposal currently being mooted is that the reserves would only be seized if the Russians violated a ceasefire that has not even been agreed. That is too timid, and the timidity seems to be motivated by misplaced fears that other reserve managers would stop holding euros.8 With the turn in the U.S., Ukraine may not have much time to wait. The Europeans have a chance to immediately alter the diplomatic situation and the military balance without even spending any of their own money.

Seizing Russia’s reserves is far from sufficient—no less than Martin Wolf has suggested that European and U.K. defense spending might need to be sustained at 5% of GDP for years to develop sufficient capabilities after decades of neglect—but it would be a valuable start.

One is a viscous dark-colored energy-dense liquid with a powerful smell, with Canada one of the world’s largest producers, and the other…

Reserves are only supposed to be used in emergencies, and, ideally their existence also helps prevent emergencies by bolstering confidence. From this perspective, there is little danger that reserve holders will ever choose to “redeem” or “cash in” their foreign assets.

To be fair to the CBR’s foreign reserve management team, it is unlikely that anyone there was privy to Putin’s plans, although they did cut their USD exposure from 21.2% of reserves (including gold) to 10.9% in the course of 2021. The really big shift had occurred earlier, after the seizure of Crimea in 2014. Before that, the CBR held 45% of its FX reserves (excluding gold) in USD and 31% of its non-gold country exposure was to the U.S. as of January 1, 2014. France, Germany, and the U.K. also had much higher weights back then. The biggest surprise for the Russians in 2022 was probably that Korea, Japan, Singapore, and Taiwan all joined in all of the sanctions.

The €183 billion has been “re-invested to minimise risk and capital requirements” by Euroclear, mostly in EUR, but the portfolio nevertheless generates billions of euros a year, much of which is now being transferred to Ukraine. The currency mix of Euroclear Bank’s “Cash balances related to Russian sanctions” is radically different—and lower-yielding—than the currency mix of its “‘Business as usual’ cash balances”. Brad Setser and Michael Weilandt have persuasively argued that the cash could be invested differently to generate higher returns without taking additional credit risk.

This is not even a cost to the extent that higher defense spending on R&D can boost private-sector innovation and to the extent that running down inventories of older military hardware creates a stimulus for manufacturers to make more new gear.

The Russians protest that their state assets are protected by international law, but international law also prevents them from invading their neighbors and committing war crimes.

For an even bigger accounting gimmick, the allies could create a limited-recourse loan to Ukraine that would be collateralized solely by Ukraine’s reparations claims against Russia. If Russia fails to pay reparations (likely), then the lenders would have the right to seize as many Russian state assets as they can to cover their “losses”, including the foreign reserves. As far as I can tell, this idea was first conceived by Martin Sandbu at the end of 2023, and was since written up in greater detail a few months later by Hugo Dixon, Lee C. Buchheit, and Daleep Singh.

Even if that did happen, which seems unlikely given the lack of viable alternatives, it is far from obvious that this would be bad for Europeans. Besides which, the far bigger impediment to the international use of the euro for reserves and offshore borrowing is the persistence of sovereign risk and subscale market size. Apparently it is easier to cower before the empty threats of the Saudis than to create a common bond market backed by the central bank.

Excellent coverage....appreciate the work that went into this.

This is what I've been wanting to see.